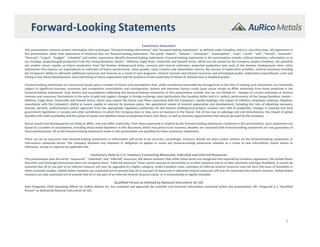

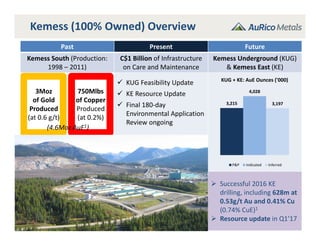

- The corporate update provides an overview of AuRico Metals' royalty portfolio and Kemess gold-copper project.

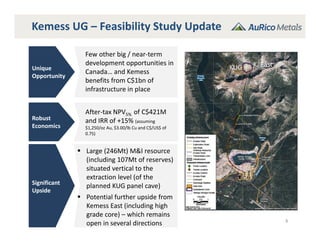

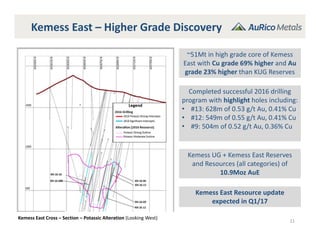

- Recent developments include positive reserve increases at several royalty assets, an updated feasibility study for the Kemess Underground project, and successful drilling at Kemess East that will lead to a resource update.

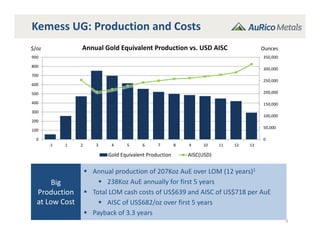

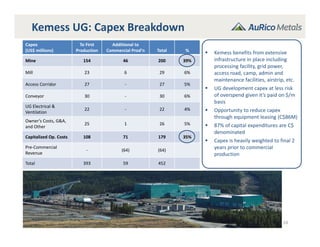

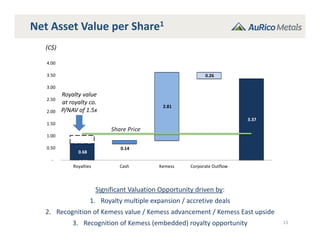

- The feasibility study shows the Kemess Underground project has an after-tax NPV of C$421M and IRR of 15.4%, with annual production of over 200koz gold equivalent and total cash costs of US$639/oz.