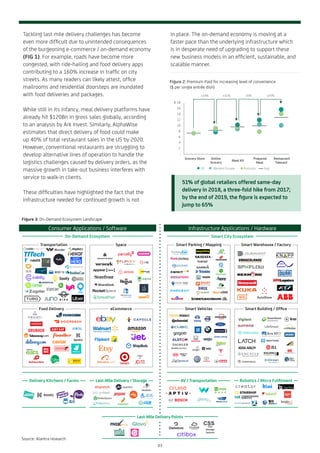

1) The rise of the on-demand economy is fueling innovation in smart cities as companies strive to meet consumer expectations of immediacy and optimize last-mile delivery.

2) However, the infrastructure is struggling to keep up and traditional models are proving too slow to respond. Technology companies are leading investments in startups developing solutions like autonomous vehicles and micro-fulfillment centers.

3) Major deals like Amazon acquiring Whole Foods demonstrate how tech firms are pursuing acquisitions to gain fast access to infrastructure that supports same-day delivery and revolutionizes industries like transportation and mobility.