Stakeholders in InputIndustry

1) Farmer/Producer

2) Agri input companies

3) Input dealers

4) Government and Government agencies

5) Co-operative societies.

3.

Agriculture Inputs

Inputs :Seeds, Fertilizers, Pesticides and Farm machinery and

equipment

Source : Nurture Farm

4.

Seeds and PlantingMaterials

• Seed is the basic and most critical input.

• It includes planting and propagating materials (Seeds, Stem,

Cuttings etc.)

• In India, the three-generation system – Breeder, foundation

and certified system is followed.

5.

Type– Seeds

a) NucleusSeeds : Initial seed obtained from plant selected for

breeding purpose. Its termed as parental line and highly pure.

b) Breeder seed : It's developed from Nucleus seeds. This done a

trained plant breeder.

c) Foundation seed : It's produced from Breeder seeds. It’s the

progeny or product of breeder seed.

d) Certified seeds : It’s the progeny of the foundation seeds. Certain

level of genetic identity and purity will be maintained according to

the standards.

6.

Continued

• Re-structuring ofthe seed industry by Government of

India through the National Seed Project Phase-I (1977-

78), Phase-II (1978-79) and Phase-III (1990-1991).

• National Seed policy 2002

Ten Thrust areas include

7.

Seed Policy :Thrust areas

1. Varietal Development and Plant Varieties Protection

2. Seed Production

3. Quality Assurance

4. Seed Distribution and Marketing.

5. Infrastructure facilities

8.

Continued ….

6. TransgenicPlant Varieties.

7. Import of seeds and planting material.

8.Export of seeds

9.Promotion of Domestic Seed

10. Strengthening of monitoring system

9.

Indian Seed Industry-Basic info's

• Two National Level organizations – 1) National seeds corporation (NSC)

2) States Farms corporation of India Ltd(SFCI)

• 15 state seed corporations

• Approximately 300 Seed companies (150 large private companies).

• 19 state seed certification agencies and 63 notified seed testing labs.

• Wheat and Rice account 60% of the seeds produced.

• 50% production by private sector – Hybrids, Vegetables, flowers etc.

• NSC and SFCI merged in 2013.

• SFCI has large acreage of farms and NSC - efficient distribution network.

10.

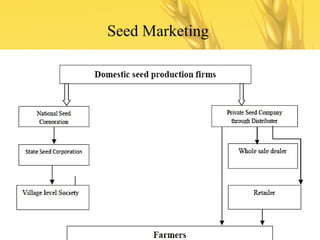

Seed production andsupply system in India

a) Formal b) Informal or can be termed as Institutional and Non

institutional.

b) Institutional (Formal)- Can be Public and Private ( MNCs and

Indian companies).

Institutional includes NSC, SAU(State Agricultural Universities)

State government agencies, Research center's etc.[ Public]

MNCs, TNC(Transnational company) and Indian private sector

companies.

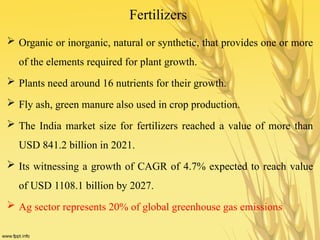

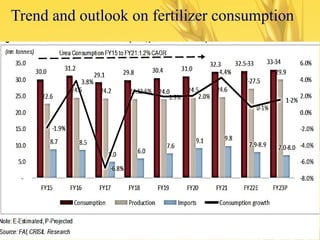

Fertilizers

Organic orinorganic, natural or synthetic, that provides one or more

of the elements required for plant growth.

Plants need around 16 nutrients for their growth.

Fly ash, green manure also used in crop production.

The India market size for fertilizers reached a value of more than

USD 841.2 billion in 2021.

Its witnessing a growth of CAGR of 4.7% expected to reach value

of USD 1108.1 billion by 2027.

Ag sector represents 20% of global greenhouse gas emissions

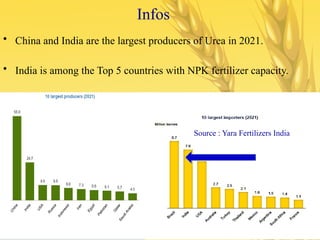

Infos

• China andIndia are the largest producers of Urea in 2021.

• India is among the Top 5 countries with NPK fertilizer capacity.

Source : Yara Fertilizers India

17.

Drivers of consumption

1)Population growth

2) Economic growth and changing food preferences

3) Higher cropping intensity

4) Nutrient use efficiency in farming

5) Waste and loss across the food value chain

Note : Seasonal influence on consumption pattern

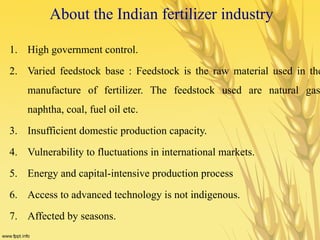

About the Indianfertilizer industry

1. High government control.

2. Varied feedstock base : Feedstock is the raw material used in the

manufacture of fertilizer. The feedstock used are natural gas

naphtha, coal, fuel oil etc.

3. Insufficient domestic production capacity.

4. Vulnerability to fluctuations in international markets.

5. Energy and capital-intensive production process

6. Access to advanced technology is not indigenous.

7. Affected by seasons.

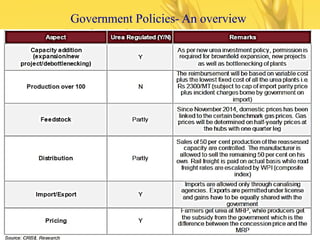

Continued …..

Governmentinitiatives to incentivize players for producing beyond

the cut-off capacity.

Online monitoring system – Fertilizer monitoring system(FMS)-

distribution and movement of fertilizers along with import of finished

fertilizers, fertilizer inputs and production by indigenous units.

Subsidy payment mechanism for urea.

Freight subsidy is provided for the movement of Urea and subsidized

P&K-fertilizers.

Uniform freight policy (2008) to ensure the availability of fertilizers

in all parts of the country. (*Primary and Secondary Movement).

22.

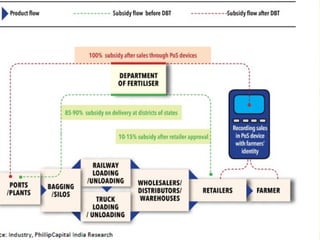

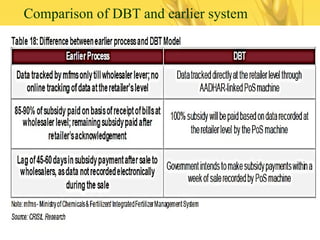

Continued …

DirectBenefit Transfer (DBT,2016) is the process of transferring the subsidy or the

Government’s scheme benefits directly to the beneficiary’s bank account.

PoS software developed for

1. Aadhaar virtual ID option during use to registration, login and sale activity in

DBT Software

2. To captures sale to farmers, mixture manufacturers, planter associations etc.

3. With Multi-lingual facility.

4. It has Provision for Soil Health Card (SHC) recommendation: area-specific, crop

specific recommendations.

Integrated Fertilizer Management System (iFMS) for monitoring the sale of

fertilizers.

Nutrient Based Subsidy Scheme (NBS scheme)

What changed ?(Source : Microsave report)

1) Stronger operational control through Mobile Fertilizer

Management System (MFMS) application.

2) Aadhaar enabled Fertilizer Distribution System(AeFDS)-

Improved availability and strengthened fertilizer distribution

system.

3) Increased accountability of stakeholders including fertilizer

manufacturers, wholesalers, and retailers.

4) Improved tracking of physical movement of fertilizer from

manufacturers to farmers.

26.

5) Transactions authenticatedthrough PoS may not be feasible

during peak “Kharif” season due to high transaction time.

6) Retailers can only handle 120 transactions in a day, which is

insufficient to handle rush of 300-500 farmers per day.

7) MFMS is to monitor the movement of the fertilizer from the

manufacturer to warehouse to wholesalers and from wholesalers

to retailers

27.

Continued

DBT paymentsystem does not cover Imported Urea as the

cost of imported urea is completely borne by Government

of India.

Statutory rate recovered from Fertilizers Marketing

Entities / handling agencies after adjusting Port dues,

customs duty etc.

28.

Industry risks

1) Dependenceon imported fertilizers.

2) Price fluctuations in feedstocks and gas. Ex : LNG as

feed stock.

3) Changes in government policies

4) Demand fluctuations.

29.

Some industry trends

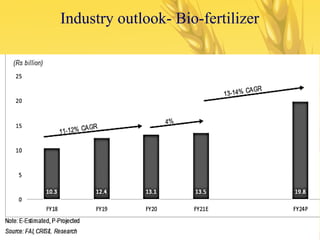

1.Growth of bio-fertilizers.

2. Preference for Liquid biofertilizers- Product form modification

Note : Liquid inoculant formulations containing sprayable particles of

the inoculant mixed with a suitable medium.

3. Water soluble fertilizers

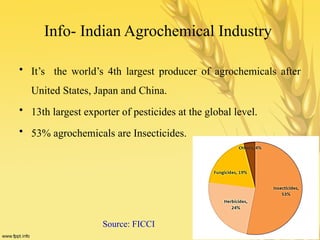

Info- Indian AgrochemicalIndustry

• It’s the world’s 4th largest producer of agrochemicals after

United States, Japan and China.

• 13th largest exporter of pesticides at the global level.

• 53% agrochemicals are Insecticides.

Source: FICCI

Growth drivers

Herbicides

a) Labourcosts and Labour shortage.

b) To enhance growth and production.

Other chemicals

c) Incidence of pests and diseases.

d) To reduce the loss.

34.

Crop loss -India

30-35 % crop loss due to Pests.(Chakrabarty,2017)

Nematodes(microscopic worms) emerged as a major threat to

crop ( Loss estimated : 60 million tonnes).

35.

IPM(Integrated Pest management)

•Integrated Pest Management (IPM) is a sustainable approach to pest

management by combination of biological, mechanical, physical and

chemical methods.

• GOI adopted IPM as part of overall Crop Production Programme

since 1985.

• 36 CIPMCs in 28 States and 2 UT

(Central Integrated Pest Management Centres (CIPMCs).

36.

IPM-Major Objectives

1) Minimizethe crop losses caused by pests and diseases.

2) Encourage farmers to use various ecologically sustainable pest

management approaches

3) Promote use of bio-pesticides & bio-control agents.

4) Conserve the diverse Agro- ecosystem for various natural enemies

for plant pests.

5) Create awareness amongst farmers on (i) Safe and judicious use of

chemical pesticides.

Major Players

International

a) Bayer

b)BASF(Badische Anilin und Soda Fabrik)

c) Dow AgroSciences India Pvt. Ltd

d) Syngenta India Limited

National

e) Tata Rallis

f) Nagarjuna Agro Chemicals Pvt. Ltd.

g) Coromandel International Ltd.

h) United Phosphorus Limited (MNC)

39.

Legal aspects

1) Indianinsecticides Act 1968

2) Insecticides Rules, 1971.

3) The Pesticide Management Bill 2020- approved in Feb

2020( Replaced act of 1968)

40.

The Pesticide ManagementBill 2020- Key points

• To regulate pesticides, including their manufacture,

import, packaging, labelling, pricing, storage,

advertisement, sale, transport, distribution, use and

disposal in order to ensure availability of safe and

effective pesticides.

The Pesticide ManagementBill 2020- Key points

Establishment of Central Pesticides Board

a) To advise the Central Government and the State Governments.

b) Criteria for good manufacturing practices including processes for

pesticide manufacturers

c) Best practices for pest control operators.

d) Procedure for the recall of pesticides

43.

Continued …

e) Criteriafor the disposal of pesticides and packages in an

environmentally sound manner;

f) Standards to be observed by the Central Pesticides

Laboratory and Pesticides Testing Laboratories;

g) Standards for training and working conditions for workers;

h) Standards for the advertisement of pesticides in all forms of

media

44.

Other imp aspects-Bill

1) Registration of pesticides.

2) To secure the distribution and availability of pesticides at fair prices,

it may constitute an authority to exercise such powers and perform

such functions to regulate the price of pesticides in such manner as

may be prescribed by the Government.

3) Pesticide Inspector- To check compliance, get samples for testing

and stop the sale and distribution of any pesticide which is found

unfit(by Executive Magistrate’s approval)

![Seed production and supply system in India

a) Formal b) Informal or can be termed as Institutional and Non

institutional.

b) Institutional (Formal)- Can be Public and Private ( MNCs and

Indian companies).

Institutional includes NSC, SAU(State Agricultural Universities)

State government agencies, Research center's etc.[ Public]

MNCs, TNC(Transnational company) and Indian private sector

companies.](https://image.slidesharecdn.com/agricultureinputmarketingenvironment-260106122903-f369faf9/85/Agriculture-Input-Marketing-Environment-Stakeholders-10-320.jpg)