Download to read offline

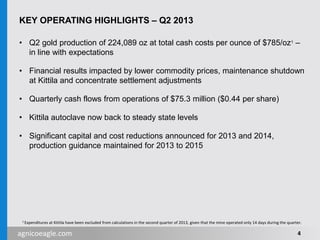

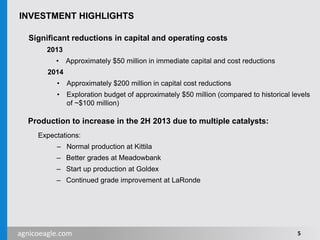

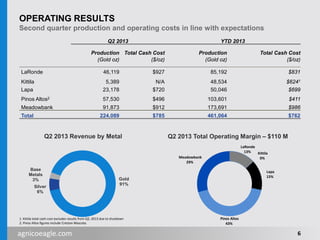

Agnico Eagle reported its second quarter 2013 results in July 2013. Q2 gold production was 224,089 ounces at total cash costs of $785 per ounce, in line with expectations. Financial results were impacted by lower commodity prices, a maintenance shutdown at the Kittila mine, and concentrate settlement adjustments. The company announced significant capital and cost reductions of approximately $50 million in 2013 and $200 million in 2014 while maintaining production guidance for 2013 to 2015.