Adjusting Entries - introduction finance

•

0 likes•1 view

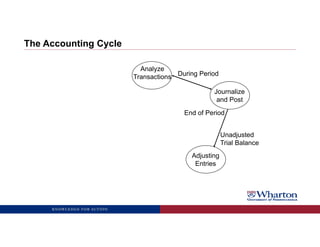

The accounting cycle involves analyzing transactions, journalizing entries, and posting to accounts to track a company's financial activities over a period. At the end of the period, adjusting entries are made for deferred and accrued revenues and expenses to update account balances according to accrual accounting. This ensures revenues and expenses are recorded in the proper period before financial statements are prepared. Adjusting entries may defer existing balances, accrue new balances, or allocate asset costs like depreciation over multiple periods using methods such as straight-line depreciation. T-accounts are used to track debits and credits to accounts during this process.

Report

Share

Report

Share

Download to read offline

Recommended

Finance for Non-Finance People.pptx

This document provides an overview of key finance concepts for non-finance professionals. It discusses statutory financial reporting requirements to report on an organization's financial performance and position. This includes producing an income and expenditure statement and balance sheet. It also covers basic accounting terminology like fixed and current assets, liabilities, funds, and the importance of concepts like liquidity, solvency, and being a going concern. The document discusses costs and costings, including variable, fixed, and overhead costs. It explains cost recovery and budgeting approaches. Finally, it covers cash flow forecasts and their purpose in identifying cash critical points and planning for surpluses or deficits. The overall aim is to help non-finance staff understand relevant finance concepts and reporting

Introduction to Accounting ch03

The document provides information about adjusting entries in accounting. It discusses:

1. The need to make adjusting entries to comply with the accrual basis of accounting and match revenues and expenses to the proper periods.

2. The main types of adjusting entries - prepayments (prepaid expenses and unearned revenues) and accruals (accrued revenues and accrued expenses).

3. Examples of specific adjusting entries for prepaid expenses, unearned revenues, accrued revenues, and accrued expenses.

Accounting cycle

The accounting cycle is a series of steps to record, classify, and summarize a business's financial transactions over an accounting period. It begins with analyzing transactions and recording them in a journal. The journal entries are then posted to ledger accounts, where balances are calculated. An unadjusted trial balance lists the ledger account balances before adjusting entries. Adjusting entries follow accrual accounting principles. The adjusted trial balance incorporates these adjustments. Finally, closing entries transfer temporary account balances to permanent accounts, allowing preparation of financial statements from the post-closing trial balance.

accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of Assets = Liabilities + Owners' Equity. The balance sheet expresses this equation by listing assets, liabilities, and owners' equity. It also defines key elements like assets, liabilities, owners' equity, revenues and expenses. Transactions must follow the accounting equation and be recorded and analyzed to maintain accurate financial records.

Basic Concepts of Financial Accounting

This document provides an overview of basic financial accounting concepts, including the accounting equation, balance sheets, assets, liabilities, owners' equity, revenues, expenses, transactions, historical cost, adjustments, interest, rent, depreciation, and unearned revenue. It explains that the accounting equation must always balance, assets represent resources owned, liabilities are obligations, and owners' equity is the residual claim on assets. Revenues increase owners' equity while expenses decrease it.

ch03.ppt

This document provides an overview of adjusting entries in accounting. It discusses the key concepts of the time period assumption, accrual basis of accounting, and the matching principle. It explains that adjusting entries are needed to properly record revenues earned and expenses incurred in the correct accounting period. The major types of adjusting entries are prepayments (prepaid expenses and unearned revenues) and accruals (accrued revenues and accrued expenses). Examples are provided for how to prepare adjusting entries for each of these types.

Language of business

Basics of Accounting. Terminology, definition of Statements and examples of double entry in terms of commercial Bank.

Financial accounting in Masters of Management Studies by Prof. Subhash Dalvi

It's all about Financial Accounting:

Financial accountancy is governed by both local and international accounting standards. GAAP (which stands for Generally Accepted Accounting Principles) is the standard framework for guidelines for financial accounting used in any given jurisdiction. It includes the standards, conventions and rules that accountants follow in recording and summarising and in the preparation of financial statements. On the other hand, IFRS (International Financial Reporting Standards) is a set of international accounting standards stating how particular types of transactions and other events should be reported in financial statements. IFRS are issued by the International Accounting Standards (IASs).

Recommended

Finance for Non-Finance People.pptx

This document provides an overview of key finance concepts for non-finance professionals. It discusses statutory financial reporting requirements to report on an organization's financial performance and position. This includes producing an income and expenditure statement and balance sheet. It also covers basic accounting terminology like fixed and current assets, liabilities, funds, and the importance of concepts like liquidity, solvency, and being a going concern. The document discusses costs and costings, including variable, fixed, and overhead costs. It explains cost recovery and budgeting approaches. Finally, it covers cash flow forecasts and their purpose in identifying cash critical points and planning for surpluses or deficits. The overall aim is to help non-finance staff understand relevant finance concepts and reporting

Introduction to Accounting ch03

The document provides information about adjusting entries in accounting. It discusses:

1. The need to make adjusting entries to comply with the accrual basis of accounting and match revenues and expenses to the proper periods.

2. The main types of adjusting entries - prepayments (prepaid expenses and unearned revenues) and accruals (accrued revenues and accrued expenses).

3. Examples of specific adjusting entries for prepaid expenses, unearned revenues, accrued revenues, and accrued expenses.

Accounting cycle

The accounting cycle is a series of steps to record, classify, and summarize a business's financial transactions over an accounting period. It begins with analyzing transactions and recording them in a journal. The journal entries are then posted to ledger accounts, where balances are calculated. An unadjusted trial balance lists the ledger account balances before adjusting entries. Adjusting entries follow accrual accounting principles. The adjusted trial balance incorporates these adjustments. Finally, closing entries transfer temporary account balances to permanent accounts, allowing preparation of financial statements from the post-closing trial balance.

accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of Assets = Liabilities + Owners' Equity. The balance sheet expresses this equation by listing assets, liabilities, and owners' equity. It also defines key elements like assets, liabilities, owners' equity, revenues and expenses. Transactions must follow the accounting equation and be recorded and analyzed to maintain accurate financial records.

Basic Concepts of Financial Accounting

This document provides an overview of basic financial accounting concepts, including the accounting equation, balance sheets, assets, liabilities, owners' equity, revenues, expenses, transactions, historical cost, adjustments, interest, rent, depreciation, and unearned revenue. It explains that the accounting equation must always balance, assets represent resources owned, liabilities are obligations, and owners' equity is the residual claim on assets. Revenues increase owners' equity while expenses decrease it.

ch03.ppt

This document provides an overview of adjusting entries in accounting. It discusses the key concepts of the time period assumption, accrual basis of accounting, and the matching principle. It explains that adjusting entries are needed to properly record revenues earned and expenses incurred in the correct accounting period. The major types of adjusting entries are prepayments (prepaid expenses and unearned revenues) and accruals (accrued revenues and accrued expenses). Examples are provided for how to prepare adjusting entries for each of these types.

Language of business

Basics of Accounting. Terminology, definition of Statements and examples of double entry in terms of commercial Bank.

Financial accounting in Masters of Management Studies by Prof. Subhash Dalvi

It's all about Financial Accounting:

Financial accountancy is governed by both local and international accounting standards. GAAP (which stands for Generally Accepted Accounting Principles) is the standard framework for guidelines for financial accounting used in any given jurisdiction. It includes the standards, conventions and rules that accountants follow in recording and summarising and in the preparation of financial statements. On the other hand, IFRS (International Financial Reporting Standards) is a set of international accounting standards stating how particular types of transactions and other events should be reported in financial statements. IFRS are issued by the International Accounting Standards (IASs).

Basic Concepts of Financial Accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of assets equaling liabilities plus owners' equity. Assets are valuable resources owned, while liabilities are obligations, and owners' equity is the residual interest in assets. Revenues increase owners' equity by providing goods/services, while expenses decrease it by consuming resources to generate revenue. Financial statements like the balance sheet present a company's assets, liabilities, and owners' equity at a point in time.

Basic Concepts of Financial Accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of assets equaling liabilities plus owners' equity. Assets are valuable resources owned, while liabilities are obligations, and owners' equity is the residual interest in assets. Revenues increase owners' equity by providing goods/services, while expenses decrease it by consuming resources to generate revenue. Financial statements like the balance sheet present a company's assets, liabilities, and owners' equity at a point in time.

Pre-Read - Understanding Financial Statements and Cash Flows.pdf

This document provides an overview of key financial statements and cash flow concepts. It discusses the objectives of understanding financial statements and cash flows. The four basic financial statements are described as the balance sheet, income statement, statement of changes in equity, and cash flow statement. Key components and calculations for the income statement and balance sheet are defined. The statement of cash flows is explained as measuring cash inflows and outflows from operating, investing, and financing activities. Important terms like net working capital and free cash flows are also covered.

02.PPT

The document discusses key concepts in financial accounting, including the accounting equation (Assets = Liabilities + Owners' Equity), transaction analysis, revenues, expenses, and adjustments. It explains that the accounting equation must always balance, and transactions may affect asset, liability, or owners' equity accounts. Revenues increase owners' equity while expenses decrease it. Interest is computed based on principal, interest rate, and time period.

Accounting and management unit one and basics

The document discusses key concepts in financial accounting including the accounting equation, assets, liabilities, owners' equity, revenues, expenses, and transactions. It explains that the accounting equation is Assets = Liabilities + Owners' Equity and must always balance. Transactions are analyzed to determine their impact on accounts to maintain the balance of the equation. Revenues increase owners' equity while expenses decrease owners' equity.

Job Costing - An Execution Guide for Operations NSCA Best Practices Conference

Job costing is typically thought of as an accounting function. Margins are only getting tighter so every point of margin possible must be achieved in the execution of projects. The project team’s understanding of the financial aspects can make the difference in having unprofitable or profitable projects and service contracts

FA.pptx

The document provides an overview of basic financial accounting concepts including the definition of accounts, accounting principles and processes, types of accounts and ledgers, the accounting cycle, and key accounting terminology. It also discusses the different bases, systems, and branches of accounting as well as the advantages, limitations, and users of accounting information.

Introduction to financial accounting

The document discusses basic concepts of financial accounting including the accounting equation, balance sheets, and key elements like assets, liabilities, owners' equity, revenues, and expenses. It explains that the accounting equation must always balance, with assets equal to liabilities plus owners' equity. Transactions can increase or decrease different elements of the balance sheet to maintain the balance of the equation. Historical costs, revenues, expenses, adjustments, and other accounting concepts are also summarized.

Basics of financial accounting

This document provides an overview of basic financial accounting concepts. It defines key accounting terms like accounts, accounting, the accounting cycle and basis. It describes the different types of accounts, rules of double entry system and branches of accounting. It also explains the accounting process including journal, ledger, trial balance and errors. The accounting concepts, conventions and terminology are introduced along with the different books of accounts used.

Finacial accounting

Real estate is something that you can physically touch and feel – it's a real good and, therefore, for many financiar ,feels more real. Maybe this partially accounts for the high return on the venture, as from 1978-2004, real estate has had an average return of 8.6%. For many time this investment has generated consistent wealth and long term respect for millions of people.

Basic concepts of accounting

The document discusses key concepts in financial accounting, including the accounting equation of Assets = Liabilities + Owners' Equity. It explains that the balance sheet is an expanded expression of this equation. It also defines assets, liabilities, owners' equity, revenues and expenses, and how various transactions affect the accounting equation. Specific topics covered include historical cost, depreciation, interest, rent, sales of inventory, adjustments to accounts, and unearned revenue.

Online Accounting Software Uk

Cloud based <a>Online Accounting Software</a> for day to day needs of accountants and sme's, allows you to manage payroll, bookkeeping for free.

Learn More :- https://www.capium.com

basic of accounts

The document discusses key concepts in financial accounting, including the accounting equation (Assets = Liabilities + Owners' Equity), balance sheets, and the basic elements they contain (assets, liabilities, owners' equity). It also covers revenues and expenses, how they impact owners' equity, and examples like sales of inventory that contain both revenue and expense elements. The document discusses various adjustments that may need to be made to accounting records like depreciation, interest, rent, and unearned revenue.

Balance Sheets

The balance sheet is a financial statement that lists a business's assets, liabilities, and capital at a specific point in time. It provides a snapshot of what the business owns and owes. The balance sheet contains sections for fixed assets, current assets, current liabilities, and capital and reserves. Fixed assets are items owned for several years like buildings and machinery. Current assets can change quickly and include inventory, cash, and amounts owed to the business. Current liabilities are short-term debts owed like accounts payable. The capital and reserves section shows where the money to purchase assets came from, such as shareholder investments and retained profits. The balance sheet must balance with assets equaling liabilities plus capital.

basicaccountingterminology.pdf

This document defines key accounting terminology used in bookkeeping and financial reporting. It explains that bookkeeping is the systematic recording of financial transactions affecting a business. It also defines common accounting concepts like the balance sheet, which lists total assets and liabilities to show net worth, and the income statement, which records revenues and expenses. Finally, it outlines the different bases of accounting, including cash basis, accrual basis, and mixed basis.

Basic accounting terminology

This document defines key accounting terminology used in bookkeeping and financial reporting. It explains that bookkeeping is the systematic recording of financial transactions, and that the journal and ledger are used to record transactions with debits and credits. It also defines accounting concepts like assets, liabilities, revenues, and expenses. Finally, it outlines the cash, accrual, and mixed bases of accounting.

Week 2 slides - Balance Sheet.ppt

This document discusses key concepts in accounting including:

1) Assets and liabilities are classified on the balance sheet as either current (used up within 12 months) or non-current (used up in over 12 months). Current assets include prepaid expenses.

2) Owner's equity is calculated as assets minus liabilities and represents the value remaining for owners, not a pool of cash. It increases with revenues and decreases with expenses.

3) Double-entry bookkeeping follows the principle that for every debit there is an equal and opposite credit, recording monetary events with at least one debit and one credit across two accounts.

Fundamentals Of Accounting

This document provides an overview of fundamentals of accounting. It defines accounting as recording, classifying, summarizing, analyzing, interpreting and communicating financial transactions and events in monetary terms. It discusses the key accounting concepts like systems of accounting, basis of accounting, classification of accounts, accounting equation, books of accounts, financial statements and their uses. The document also provides examples of common business transactions and explains the accounting process and principles involved in recording them.

Book keeping basic concept: - raju mba 4sem

The document discusses the basic concepts of book keeping and accounting. It explains that book keeping involves systematically recording business transactions, while accounting builds on book keeping by analyzing records to prepare financial statements and interpret financial results. The key principles of accounting include the money measurement concept, business entity concept, going concern concept, and matching concept. Financial statements like the manufacturing account, trading account, profit and loss account, and balance sheet are prepared according to accounting principles and concepts.

Reporting and financial_statements_1

This document provides an overview of basic financial statements including the balance sheet, income statement, statement of retained earnings, and statement of cash flows. It explains the purpose and key components of each statement. The balance sheet presents a company's assets, liabilities, and equity on a given date. The income statement shows revenues and expenses over a period of time. The statement of retained earnings tracks changes in retained earnings. The statement of cash flows reports cash inflows and outflows from operating, investing, and financing activities. Notes to the financial statements provide additional important information.

University of North Carolina at Charlotte degree offer diploma Transcript

办理美国UNCC毕业证书制作北卡大学夏洛特分校假文凭定制Q微168899991做UNCC留信网教留服认证海牙认证改UNCC成绩单GPA做UNCC假学位证假文凭高仿毕业证GRE代考如何申请北卡罗莱纳大学夏洛特分校University of North Carolina at Charlotte degree offer diploma Transcript

1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

More Related Content

Similar to Adjusting Entries - introduction finance

Basic Concepts of Financial Accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of assets equaling liabilities plus owners' equity. Assets are valuable resources owned, while liabilities are obligations, and owners' equity is the residual interest in assets. Revenues increase owners' equity by providing goods/services, while expenses decrease it by consuming resources to generate revenue. Financial statements like the balance sheet present a company's assets, liabilities, and owners' equity at a point in time.

Basic Concepts of Financial Accounting

The document provides an overview of basic financial accounting concepts. It explains that accounting is based on the accounting equation of assets equaling liabilities plus owners' equity. Assets are valuable resources owned, while liabilities are obligations, and owners' equity is the residual interest in assets. Revenues increase owners' equity by providing goods/services, while expenses decrease it by consuming resources to generate revenue. Financial statements like the balance sheet present a company's assets, liabilities, and owners' equity at a point in time.

Pre-Read - Understanding Financial Statements and Cash Flows.pdf

This document provides an overview of key financial statements and cash flow concepts. It discusses the objectives of understanding financial statements and cash flows. The four basic financial statements are described as the balance sheet, income statement, statement of changes in equity, and cash flow statement. Key components and calculations for the income statement and balance sheet are defined. The statement of cash flows is explained as measuring cash inflows and outflows from operating, investing, and financing activities. Important terms like net working capital and free cash flows are also covered.

02.PPT

The document discusses key concepts in financial accounting, including the accounting equation (Assets = Liabilities + Owners' Equity), transaction analysis, revenues, expenses, and adjustments. It explains that the accounting equation must always balance, and transactions may affect asset, liability, or owners' equity accounts. Revenues increase owners' equity while expenses decrease it. Interest is computed based on principal, interest rate, and time period.

Accounting and management unit one and basics

The document discusses key concepts in financial accounting including the accounting equation, assets, liabilities, owners' equity, revenues, expenses, and transactions. It explains that the accounting equation is Assets = Liabilities + Owners' Equity and must always balance. Transactions are analyzed to determine their impact on accounts to maintain the balance of the equation. Revenues increase owners' equity while expenses decrease owners' equity.

Job Costing - An Execution Guide for Operations NSCA Best Practices Conference

Job costing is typically thought of as an accounting function. Margins are only getting tighter so every point of margin possible must be achieved in the execution of projects. The project team’s understanding of the financial aspects can make the difference in having unprofitable or profitable projects and service contracts

FA.pptx

The document provides an overview of basic financial accounting concepts including the definition of accounts, accounting principles and processes, types of accounts and ledgers, the accounting cycle, and key accounting terminology. It also discusses the different bases, systems, and branches of accounting as well as the advantages, limitations, and users of accounting information.

Introduction to financial accounting

The document discusses basic concepts of financial accounting including the accounting equation, balance sheets, and key elements like assets, liabilities, owners' equity, revenues, and expenses. It explains that the accounting equation must always balance, with assets equal to liabilities plus owners' equity. Transactions can increase or decrease different elements of the balance sheet to maintain the balance of the equation. Historical costs, revenues, expenses, adjustments, and other accounting concepts are also summarized.

Basics of financial accounting

This document provides an overview of basic financial accounting concepts. It defines key accounting terms like accounts, accounting, the accounting cycle and basis. It describes the different types of accounts, rules of double entry system and branches of accounting. It also explains the accounting process including journal, ledger, trial balance and errors. The accounting concepts, conventions and terminology are introduced along with the different books of accounts used.

Finacial accounting

Real estate is something that you can physically touch and feel – it's a real good and, therefore, for many financiar ,feels more real. Maybe this partially accounts for the high return on the venture, as from 1978-2004, real estate has had an average return of 8.6%. For many time this investment has generated consistent wealth and long term respect for millions of people.

Basic concepts of accounting

The document discusses key concepts in financial accounting, including the accounting equation of Assets = Liabilities + Owners' Equity. It explains that the balance sheet is an expanded expression of this equation. It also defines assets, liabilities, owners' equity, revenues and expenses, and how various transactions affect the accounting equation. Specific topics covered include historical cost, depreciation, interest, rent, sales of inventory, adjustments to accounts, and unearned revenue.

Online Accounting Software Uk

Cloud based <a>Online Accounting Software</a> for day to day needs of accountants and sme's, allows you to manage payroll, bookkeeping for free.

Learn More :- https://www.capium.com

basic of accounts

The document discusses key concepts in financial accounting, including the accounting equation (Assets = Liabilities + Owners' Equity), balance sheets, and the basic elements they contain (assets, liabilities, owners' equity). It also covers revenues and expenses, how they impact owners' equity, and examples like sales of inventory that contain both revenue and expense elements. The document discusses various adjustments that may need to be made to accounting records like depreciation, interest, rent, and unearned revenue.

Balance Sheets

The balance sheet is a financial statement that lists a business's assets, liabilities, and capital at a specific point in time. It provides a snapshot of what the business owns and owes. The balance sheet contains sections for fixed assets, current assets, current liabilities, and capital and reserves. Fixed assets are items owned for several years like buildings and machinery. Current assets can change quickly and include inventory, cash, and amounts owed to the business. Current liabilities are short-term debts owed like accounts payable. The capital and reserves section shows where the money to purchase assets came from, such as shareholder investments and retained profits. The balance sheet must balance with assets equaling liabilities plus capital.

basicaccountingterminology.pdf

This document defines key accounting terminology used in bookkeeping and financial reporting. It explains that bookkeeping is the systematic recording of financial transactions affecting a business. It also defines common accounting concepts like the balance sheet, which lists total assets and liabilities to show net worth, and the income statement, which records revenues and expenses. Finally, it outlines the different bases of accounting, including cash basis, accrual basis, and mixed basis.

Basic accounting terminology

This document defines key accounting terminology used in bookkeeping and financial reporting. It explains that bookkeeping is the systematic recording of financial transactions, and that the journal and ledger are used to record transactions with debits and credits. It also defines accounting concepts like assets, liabilities, revenues, and expenses. Finally, it outlines the cash, accrual, and mixed bases of accounting.

Week 2 slides - Balance Sheet.ppt

This document discusses key concepts in accounting including:

1) Assets and liabilities are classified on the balance sheet as either current (used up within 12 months) or non-current (used up in over 12 months). Current assets include prepaid expenses.

2) Owner's equity is calculated as assets minus liabilities and represents the value remaining for owners, not a pool of cash. It increases with revenues and decreases with expenses.

3) Double-entry bookkeeping follows the principle that for every debit there is an equal and opposite credit, recording monetary events with at least one debit and one credit across two accounts.

Fundamentals Of Accounting

This document provides an overview of fundamentals of accounting. It defines accounting as recording, classifying, summarizing, analyzing, interpreting and communicating financial transactions and events in monetary terms. It discusses the key accounting concepts like systems of accounting, basis of accounting, classification of accounts, accounting equation, books of accounts, financial statements and their uses. The document also provides examples of common business transactions and explains the accounting process and principles involved in recording them.

Book keeping basic concept: - raju mba 4sem

The document discusses the basic concepts of book keeping and accounting. It explains that book keeping involves systematically recording business transactions, while accounting builds on book keeping by analyzing records to prepare financial statements and interpret financial results. The key principles of accounting include the money measurement concept, business entity concept, going concern concept, and matching concept. Financial statements like the manufacturing account, trading account, profit and loss account, and balance sheet are prepared according to accounting principles and concepts.

Reporting and financial_statements_1

This document provides an overview of basic financial statements including the balance sheet, income statement, statement of retained earnings, and statement of cash flows. It explains the purpose and key components of each statement. The balance sheet presents a company's assets, liabilities, and equity on a given date. The income statement shows revenues and expenses over a period of time. The statement of retained earnings tracks changes in retained earnings. The statement of cash flows reports cash inflows and outflows from operating, investing, and financing activities. Notes to the financial statements provide additional important information.

Similar to Adjusting Entries - introduction finance (20)

Pre-Read - Understanding Financial Statements and Cash Flows.pdf

Pre-Read - Understanding Financial Statements and Cash Flows.pdf

Job Costing - An Execution Guide for Operations NSCA Best Practices Conference

Job Costing - An Execution Guide for Operations NSCA Best Practices Conference

Recently uploaded

University of North Carolina at Charlotte degree offer diploma Transcript

办理美国UNCC毕业证书制作北卡大学夏洛特分校假文凭定制Q微168899991做UNCC留信网教留服认证海牙认证改UNCC成绩单GPA做UNCC假学位证假文凭高仿毕业证GRE代考如何申请北卡罗莱纳大学夏洛特分校University of North Carolina at Charlotte degree offer diploma Transcript

1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

The Rise and Fall of Ponzi Schemes in America.pptx

Ponzi schemes, a notorious form of financial fraud, have plagued America’s investment landscape for decades. Named after Charles Ponzi, who orchestrated one of the most infamous schemes in the early 20th century, these fraudulent operations promise high returns with little or no risk, only to collapse and leave investors with significant losses. This article explores the nature of Ponzi schemes, notable cases in American history, their impact on victims, and measures to prevent falling prey to such scams.

Understanding Ponzi Schemes

A Ponzi scheme is an investment scam where returns are paid to earlier investors using the capital from newer investors, rather than from legitimate profit earned. The scheme relies on a constant influx of new investments to continue paying the promised returns. Eventually, when the flow of new money slows down or stops, the scheme collapses, leaving the majority of investors with substantial financial losses.

Historical Context: Charles Ponzi and His Legacy

Charles Ponzi is the namesake of this deceptive practice. In the 1920s, Ponzi promised investors in Boston a 50% return within 45 days or 100% return in 90 days through arbitrage of international reply coupons. Initially, he paid returns as promised, not from profits, but from the investments of new participants. When his scheme unraveled, it resulted in losses exceeding $20 million (equivalent to about $270 million today).

Notable American Ponzi Schemes

1. Bernie Madoff: Perhaps the most notorious Ponzi scheme in recent history, Bernie Madoff’s fraud involved $65 billion. Madoff, a well-respected figure in the financial industry, promised steady, high returns through a secretive investment strategy. His scheme lasted for decades before collapsing in 2008, devastating thousands of investors, including individuals, charities, and institutional clients.

2. Allen Stanford: Through his company, Stanford Financial Group, Allen Stanford orchestrated a $7 billion Ponzi scheme, luring investors with fraudulent certificates of deposit issued by his offshore bank. Stanford promised high returns and lavish lifestyle benefits to his investors, which ultimately led to a 110-year prison sentence for the financier in 2012.

3. Tom Petters: In a scheme that lasted more than a decade, Tom Petters ran a $3.65 billion Ponzi scheme, using his company, Petters Group Worldwide. He claimed to buy and sell consumer electronics, but in reality, he used new investments to pay off old debts and fund his extravagant lifestyle. Petters was convicted in 2009 and sentenced to 50 years in prison.

4. Eric Dalius and Saivian: Eric Dalius, a prominent figure behind Saivian, a cashback program promising high returns, is under scrutiny for allegedly orchestrating a Ponzi scheme. Saivian enticed investors with promises of up to 20% cash back on everyday purchases. However, investigations suggest that the returns were paid using new investments rather than legitimate profits. The collapse of Saivian l

13 Jun 24 ILC Retirement Income Summit - slides.pptx

ILC's Retirement Income Summit was hosted by M&G and supported by Canada Life. The event brought together key policymakers, influencers and experts to help identify policy priorities for the next Government and ensure more of us have access to a decent income in retirement.

Contributors included:

Jo Blanden, Professor in Economics, University of Surrey

Clive Bolton, CEO, Life Insurance M&G Plc

Jim Boyd, CEO, Equity Release Council

Molly Broome, Economist, Resolution Foundation

Nida Broughton, Co-Director of Economic Policy, Behavioural Insights Team

Jonathan Cribb, Associate Director and Head of Retirement, Savings, and Ageing, Institute for Fiscal Studies

Joanna Elson CBE, Chief Executive Officer, Independent Age

Tom Evans, Managing Director of Retirement, Canada Life

Steve Groves, Chair, Key Retirement Group

Tish Hanifan, Founder and Joint Chair of the Society of Later life Advisers

Sue Lewis, ILC Trustee

Siobhan Lough, Senior Consultant, Hymans Robertson

Mick McAteer, Co-Director, The Financial Inclusion Centre

Stuart McDonald MBE, Head of Longevity and Democratic Insights, LCP

Anusha Mittal, Managing Director, Individual Life and Pensions, M&G Life

Shelley Morris, Senior Project Manager, Living Pension, Living Wage Foundation

Sarah O'Grady, Journalist

Will Sherlock, Head of External Relations, M&G Plc

Daniela Silcock, Head of Policy Research, Pensions Policy Institute

David Sinclair, Chief Executive, ILC

Jordi Skilbeck, Senior Policy Advisor, Pensions and Lifetime Savings Association

Rt Hon Sir Stephen Timms, former Chair, Work & Pensions Committee

Nigel Waterson, ILC Trustee

Jackie Wells, Strategy and Policy Consultant, ILC Strategic Advisory Board

真实可查(nwu毕业证书)美国西北大学毕业证学位证书范本原版一模一样

原版定制【微信:bwp0011】《(nwu毕业证书)美国西北大学毕业证学位证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

Mutual Fund Taxation – How Mutual Funds Are Taxed

Divadhvik explains Mutual Fund Taxation clearly: Equity funds held over a year are taxed at 10% for gains over ₹1 lakh, while short-term gains are taxed at 15%. Debt funds held over three years are taxed at 20% post-indexation. Short-term gains are taxed as per your income slab.

The state of welfare Resolution Foundation Event

How has Britain’s safety net changed since 2010 and what comes next?

Discover the Future of Dogecoin with Our Comprehensive Guidance

Learn in-depth about Dogecoin's trajectory and stay informed with 36crypto's essential and up-to-date information about the crypto space.

Our presentation delves into Dogecoin's potential future, exploring whether it's destined to skyrocket to the moon or face a downward spiral. In addition, it highlights invaluable insights. Don't miss out on this opportunity to enhance your crypto understanding!

https://36crypto.com/the-future-of-dogecoin-how-high-can-this-cryptocurrency-reach/

How to Use Payment Vouchers in Odoo 18.

Every business, big or small, deals with outgoing payments. Whether it’s to suppliers for inventory, to employees for salaries, or to vendors for services rendered, keeping track of these expenses is crucial. This is where payment vouchers come in – the unsung heroes of the accounting world.

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

高仿英国伦敦艺术大学毕业证(ual毕业证书)文凭证书原版一模一样

原版一模一样【微信:741003700 】【英国伦敦艺术大学毕业证(ual毕业证书)文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

一比一原版(cwu毕业证书)美国中央华盛顿大学毕业证如何办理

原版一模一样【微信:741003700 】【(cwu毕业证书)美国中央华盛顿大学毕业证成绩单】【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】外观非常简单,由纸质材料制成,上面印有校徽、校名、毕业生姓名、专业等信息。

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】格式相对统一,各专业都有相应的模板。通常包括以下部分:

校徽:象征着学校的荣誉和传承。

校名:学校英文全称

授予学位:本部分将注明获得的具体学位名称。

毕业生姓名:这是最重要的信息之一,标志着该证书是由特定人员获得的。

颁发日期:这是毕业正式生效的时间,也代表着毕业生学业的结束。

其他信息:根据不同的专业和学位,可能会有一些特定的信息或章节。

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】价值很高,需要妥善保管。一般来说,应放置在安全、干燥、防潮的地方,避免长时间暴露在阳光下。如需使用,最好使用复印件而不是原件,以免丢失。

综上所述,办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】是证明身份和学历的高价值文件。外观简单庄重,格式统一,包括重要的个人信息和发布日期。对持有人来说,妥善保管是非常重要的。

International Sustainability Standards Board

Issb standards

New standard for reporting sustainability on lines of tcfd

Governor Olli Rehn: Inflation down and recovery supported by interest rate cu...

Governor Olli Rehn

Bank of Finland

Press conference on the outlook for the Finnish economy

Helsinki, 11 June 2024

Tdasx: Interpreting the 2024 Cryptocurrency Market Funding Trends and Technol...

Tdasx: Interpreting the 2024 Cryptocurrency Market Funding Trends and Technological Developments

Economic Risk Factor Update: June 2024 [SlideShare]

May’s reports showed signs of continued economic growth, said Sam Millette, director, fixed income, in his latest Economic Risk Factor Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

Monthly Market Risk Update: June 2024 [SlideShare]

Markets rallied in May, with all three major U.S. equity indices up for the month, said Sam Millette, director of fixed income, in his latest Market Risk Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

Recently uploaded (20)

University of North Carolina at Charlotte degree offer diploma Transcript

University of North Carolina at Charlotte degree offer diploma Transcript

The Rise and Fall of Ponzi Schemes in America.pptx

The Rise and Fall of Ponzi Schemes in America.pptx

13 Jun 24 ILC Retirement Income Summit - slides.pptx

13 Jun 24 ILC Retirement Income Summit - slides.pptx

Discover the Future of Dogecoin with Our Comprehensive Guidance

Discover the Future of Dogecoin with Our Comprehensive Guidance

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

Governor Olli Rehn: Inflation down and recovery supported by interest rate cu...

Governor Olli Rehn: Inflation down and recovery supported by interest rate cu...

Tdasx: Interpreting the 2024 Cryptocurrency Market Funding Trends and Technol...

Tdasx: Interpreting the 2024 Cryptocurrency Market Funding Trends and Technol...

Power point analisis laporan keuangan chapter 7 subramanyam

Power point analisis laporan keuangan chapter 7 subramanyam

Economic Risk Factor Update: June 2024 [SlideShare]

Economic Risk Factor Update: June 2024 [SlideShare]

Monthly Market Risk Update: June 2024 [SlideShare]

Monthly Market Risk Update: June 2024 [SlideShare]

Adjusting Entries - introduction finance

- 1. The Accounting Cycle Analyze Transactions Journalize and Post Adjusting Entries During Period Unadjusted Trial Balance End of Period KNOWLEDGE FOR ACTION

- 2. KNOWLEDGE FOR ACTION Adjusting Entries • Adjusting entries – Internal transactions that update account balances in accordance with accrual accounting prior to the preparation of financial statements • Deferred Revenues and Expenses – Update existing account balances to reflect current accounting values – Cash flow in past; record revenue/expense now • Accrued Revenues and Expenses – Create new account balances to reflect unrecorded assets or liabilities – Record revenue/expense now; cash flow in future

- 3. KNOWLEDGE FOR ACTION Deferred Expenses • Question: Are there any assets that have been “used up” this period and should be expensed? • Examples: – Prepaid Rent – Prepaid Insurance – Depreciation or amortization • Journal Entry: Dr. Expense Cr. Prepaid Asset

- 4. KNOWLEDGE FOR ACTION Deferred Revenues • Question: Are there any liabilities that have been fulfilled by delivery of goods or services that should be recognized as revenue? • Examples: – Unearned rental revenue – Deferred subscription revenue • Journal Entry: Dr. Unearned Revenue Liability Cr. Revenue

- 5. KNOWLEDGE FOR ACTION Accrued Expenses • Question: Have any expenses accumulated during the period that have not yet been recorded? • Examples: – Income Taxes Payable – Interest Payable – Salaries and Wages Payable • Journal Entry: Dr. Expense Cr. Payable Liability

- 6. KNOWLEDGE FOR ACTION Accrued Revenue • Question: Have any revenues accumulated during the period that have not yet been recorded? • Examples: – Interest Receivable – Rent Receivable • Journal Entry: Dr. Receivable Asset Cr. Revenue

- 7. KNOWLEDGE FOR ACTION Depreciation and Amortization • Allocate the original cost of a long-lived asset over its useful life – Matches the total cost of asset to the revenues it generates over its period of use • Terminology – Tangible assets (physical assets) require depreciation – Intangible assets (abstract assets) require amortization

- 8. KNOWLEDGE FOR ACTION Depreciation and Amortization • Accounting Procedure – Depreciation is not deducted from the tangible asset account. Rather, it is recorded in a Contra Asset Account (XA) called Accumulated Depreciation, which • has a credit balance • is subtracted from PP&E on the balance sheet to get the “Net Book Value” – Amortization is often (but not always) deducted directly from the intangible asset account • Straight-line Depreciation: – Depreciation expense = (Original Cost – Salvage Value) / Useful Life

- 9. KNOWLEDGE FOR ACTION Super T-account Assets Liabilities Contributed Capital Assets Liabilities & Shareholders’ Equity Revenues Retained Earnings Dr. + Cr. - Dr. - Cr. + Dr. - Cr. + Cr. + Dr. - Cr. + Dr. - Cr. - Dr. + Expenses Contra Assets Dr. - Cr. +