3

Accounting Cycle Overview

Definition:The accounting cycle refers to the series of

steps taken in recording financial transactions and

producing financial statements for a specific period.

🞭Importance: Provides a systematic approach to maintain

accurate financial records and ensure compliance with

accounting principles.

4.

4

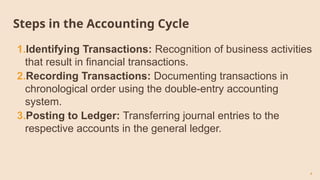

Steps in theAccounting Cycle

1.Identifying Transactions: Recognition of business activities

that result in financial transactions.

2.Recording Transactions: Documenting transactions in

chronological order using the double-entry accounting

system.

3.Posting to Ledger: Transferring journal entries to the

respective accounts in the general ledger.

5.

5

Steps in theAccounting Cycle

4.Trial Balance: Preparing a trial balance to ensure debits

equal credits and to detect any errors.

5.Adjusting Entries: Making adjustments for accrued

revenues, expenses, prepayments, and depreciation.

6.Adjusted Trial Balance: Creating a trial balance after

adjusting entries to ensure accuracy before preparing

financial statements.

6.

6

Steps in theAccounting Cycle

7. Financial Statements: Generating financial statements

(income statement, balance sheet, statement of cash

flows).

8.Closing Entries: Closing temporary accounts (revenue,

expense, and dividend accounts) to retained earnings.

9.Post-Closing Trial Balance: Verifying that all temporary

accounts have been closed properly.

7.

7

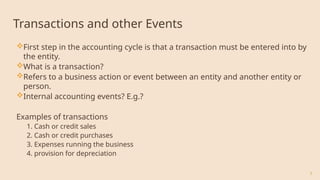

Transactions and otherEvents

First step in the accounting cycle is that a transaction must be entered into by

the entity.

What is a transaction?

Refers to a business action or event between an entity and another entity or

person.

Internal accounting events? E.g.?

Examples of transactions

1. Cash or credit sales

2. Cash or credit purchases

3. Expenses running the business

4. provision for depreciation

8.

8

Source Documents

Source documentare the original records providing evidence of a

transaction. It is the entity’s written proof showing that a transaction did

actually take place.

Serve as the foundation for recording transactions accurately and for

audit trail purposes (For owners of the business to remember the

transactions that took place during the period, it is necessary to record

the transaction in a structured manner regularly).

NB: There must be a source document for every transaction.

What about ad hoc payments e.g. Travel allowance for employees?

9.

9

Source Documents

Source Documentsshould contain:

Serial number of the source document

Nature of the transaction or the name of source document

The amount of the transaction

The date of the transaction

The identity of the parties involved in the transaction

Description

VAT

The source documents should be in duplicate, the Entity issuing the document retains the copy

and the Customer receives the original document.

The source data needs to be complete and correct to ensure that accounting records are correct.

10.

10

Common Source Documents

Sales Invoice: Document issued to customers for goods or services sold, including details such as date,

quantity, price, and terms.

Purchase Invoice: Received from suppliers for goods or services purchased on credit, containing similar

details to sales invoices.

Receipts: Acknowledgment of cash received, specifying the date, amount, and purpose of the payment.

Cheques: Written orders to pay a specified sum to a person or entity, including details of the payee, date,

amount, and purpose.

Bank Statements: Records provided by the bank showing all transactions, including deposits, withdrawals,

and charges.

Payroll Records: Documents detailing employee compensation, deductions, and taxes withheld for each pay

period.

![What Is Blockchain Technology A Simple Beginner’s Guide [2026]](https://cdn.slidesharecdn.com/ss_thumbnails/whatisblockchaintechnologyasimplebeginnersguide2026-260101112141-cf432b44-thumbnail.jpg?width=640&height=640&fit=bounds)