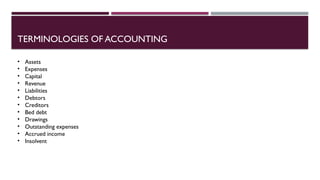

The document provides an overview of accounting, detailing the process of recording, summarizing, and reporting financial transactions for businesses and individuals. Key terminologies include assets, expenses, capital, revenue, and liabilities, each with definitions and examples. It highlights the importance of these concepts in understanding a business's financial health and operations.