This document provides an introduction to an English language textbook titled "Introduction to Accounting" which is intended to teach accounting terminology to Russian university students studying accounting and auditing.

The textbook contains 5 units that present original English language texts from accounting literature along with exercises using carefully selected terminology. The goal is to develop students' professional communication skills in English and improve their ability to quickly understand accounting texts.

Each unit contains main texts, additional readings, and exercises to practice vocabulary and develop language skills through accounting terms. Appendices provide tables of accounting term equivalents in different English varieties and lists of international accounting standards. The textbook is designed to facilitate independent and instructor-guided study of accounting in English.

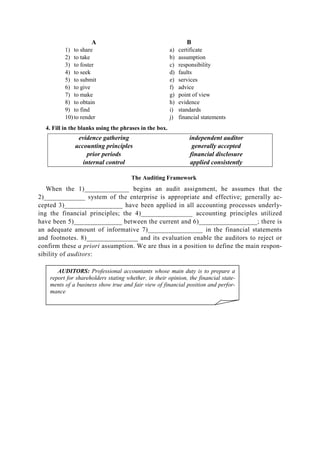

![The traditional definition of auditing is a review and an evaluation of financial records by a second

set of accountants. An internal audit is a control by a company's own accountants, checking for com-

pleteness, (1) exactness and reliability. Among other things, internal auditors are looking for (2) de-

partures from a firm's (3) established methods for recording business transactions. In most coun-

tries, the law requires all firms to have their accounts audited by an outside company. An (4) indepen-

dent audit is thus a review of financial statements and accounting records by an accountant not belong-

ing to the firm. The auditors have to (5) judge whether the accounts give what in Britain is known as a

«true and fair view» and in the US as a «fair presentation» of the company's [corporation's] financial

position. Auditors are appointed by a company's (6) most senior executives and advisors, whose

choice has to be (7) approved by the (8) owners of the company's equity at the company's (9) yearly

assembly. Auditors write an official audit report. They may also address a «management letter» to the

directors, outlining (10) inadequacies and recommending improved operating procedures. This leads

to the more recent use of the word «audit» as (11) an equivalent term for «control»: (12) multination-

al companies, for example, might undertake inventory, marketing and technical audits. Auditing in

this sense means (13) verifying that general management (14) instructions are being (15) executed in

branches, (16) companies which they control, etc.

(b) add appropriate words to these phrases:

1) Auditors _____________ companies' accounts.

2) Accounts have to ______________ a fair presentation.

3) Auditors write a ______________.

4) It's the directors who _____________ the auditors.

5) Auditors sometimes ______________ better accounting procedures.

6) Using external auditors is a _____________requirement.

11. Translate the following definitions of the economic terms relating to audit.

Auditor — ревизор, сотрудник аудиторской фирмы, контролирующий и анализирующий фи-

нансовую деятельность предприятий, а также дающий заключение по годовым бухгалтерским

отчетам и балансам;

External audit — проверка годовой отчетности организации независимым квалифицирован-

ным специалистом (аудиторской службой, аудитором), который должен определить степень дос-

товерности и правдивости информации, содержащейся в бухгалтерской отчетности и ее соответ-

ствие требованиям закона;

Internal audit — проверка годовой отчетности организации внутренним аудитором или специ-

ально подготовленным служащим организации с целью информирования менеджмента об эффектив-

ности и надежности применяемых компанией систем и выработки рекомендаций по их улучшению;

Inaudit — хозрасчетное акционерное общество, задачей которого является консультирова-

ние отечественных и иностранных партнеров совместных предприятий и осуществление кон-

троля за бухгалтерским учетом и финансовой отчетностью совместных предприятий;

Accounting — функциональная сфера бизнеса, связанная со сбором, обработкой, классифицировани-

ем, анализом и оформлением различных видов финансовой информации;

Auditor’sopinion—заключениеназначенныхаудиторов о проверке отчетности организации;

Reporting — периодическое составление предприятиями, организациями отчетов о своей деятельности,

представляемыхв государственные органы.

12. Make a free translation of the following extract from Russian into English.

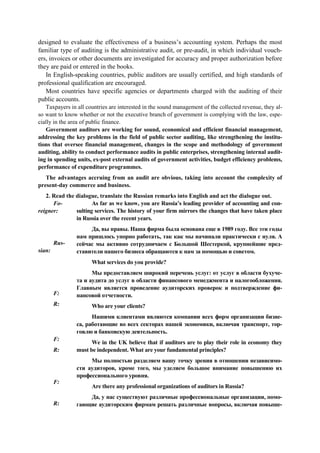

Аудиторское заключение

Цель аудитора подтвердить правильность бухгалтерской отчетности, И собственникам

и кредиторам важно знать: можно ли доверять числам, с которыми их знакомит админи-

страция предприятия.](https://image.slidesharecdn.com/oholfzwhqjkyjridwjbn-signature-2dfd883d34a9150c84f328602acf26f21197bd60f9f2637420b7ac825ad7b362-poli-160712065932/85/586-85-320.jpg)