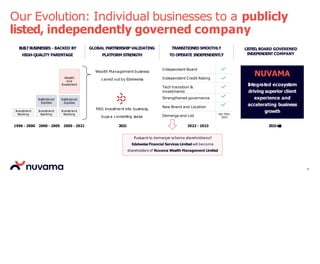

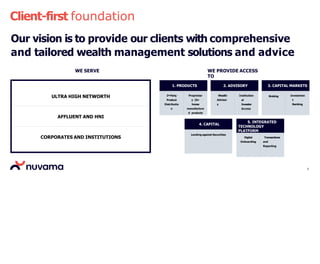

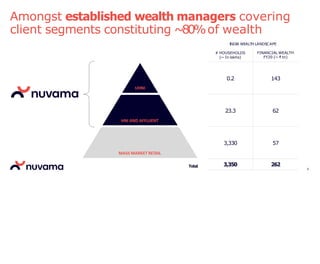

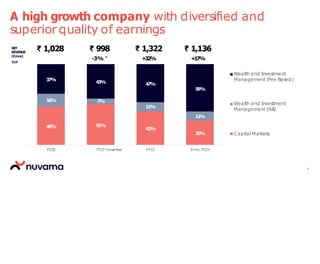

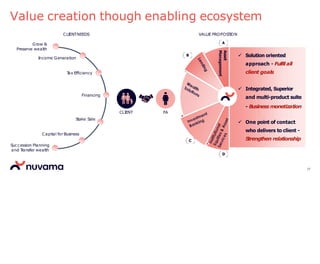

The document provides an update on Nuvama Wealth Management Business. It announces that an update on the business has been provided to stock exchanges and is attached. Nuvama is an integrated wealth management platform that serves ultra high net worth individuals, high net worth and affluent clients, and corporates and institutions. It has diversified revenue streams from wealth and investment management as well as capital markets businesses.