Downloaded 12 times

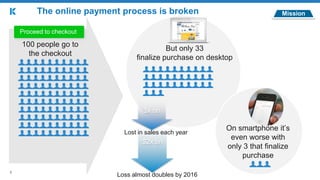

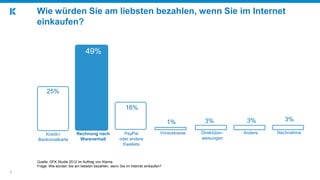

The document discusses the challenges and growth of e-commerce in Europe, highlighting issues such as high checkout abandonment rates due to payment preference and security concerns. It presents data indicating that only a fraction of users complete purchases online due to a lack of preferred payment methods and excessive steps in the process. Klarna 2.0 is introduced as a solution aimed at improving the checkout experience across various platforms while addressing merchants' needs.