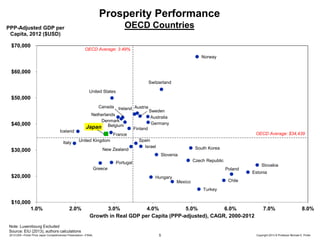

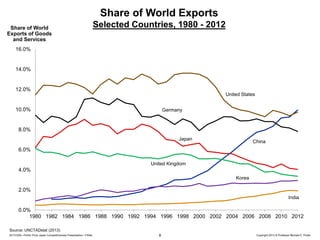

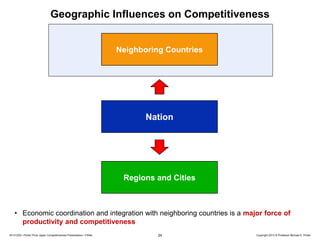

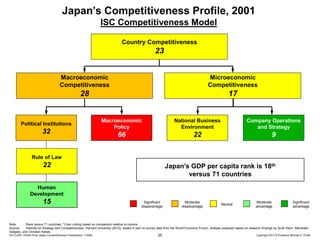

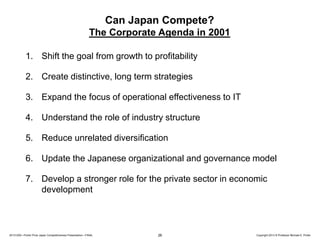

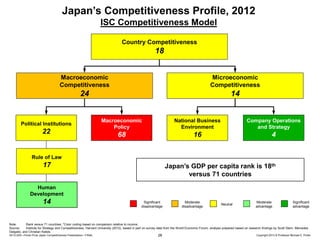

This document summarizes a presentation by Professor Michael Porter on Japan's competitiveness. It discusses Japan's economic performance since 2000, noting disappointing overall growth despite productivity gains. It also examines Japan's declining exports and workforce participation as well as low foreign investment. Porter then outlines his framework for competitiveness, emphasizing the importance of microeconomic factors like cluster development and business environment quality. The presentation concludes by calling for regional strategies to upgrade clusters and institutions to improve Japan's competitiveness.