Outline

Outline

1. Fundamental Principlesof Cost Engineering

Introduction

Definitions and Terminology for Cost Engineers

Cost Engineering Traits

Functions of Cost Engineering in Construction

Considerations in Costing

2

3.

1.

1. Introduction

1. 1Cost Engineering

Cost engineering is concerned with problems of cost

estimation, cost control, and business planning and

management science, including problems of project

management, planning, scheduling, and profitability

analysis of engineering projects and processes.

It needs understanding of

Construction Technology

Quantity surveying including understanding of contract

documents and forms of contract

Management Theory and technique: pre contract

planning, tendering policy and the organization of

resources

Construction economics

3

4.

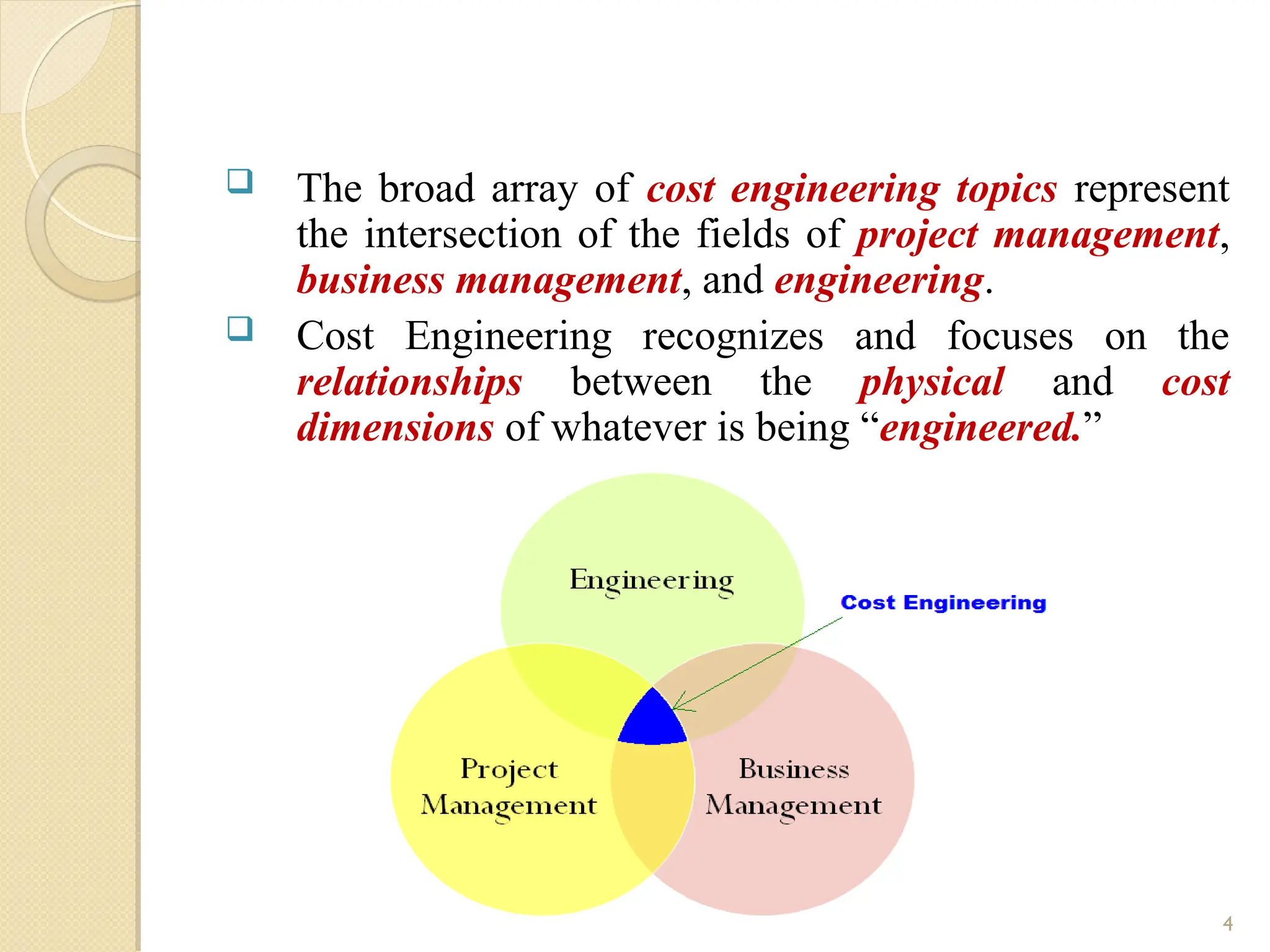

The broadarray of cost engineering topics represent

the intersection of the fields of project management,

business management, and engineering.

Cost Engineering recognizes and focuses on the

relationships between the physical and cost

dimensions of whatever is being “engineered.”

4

5.

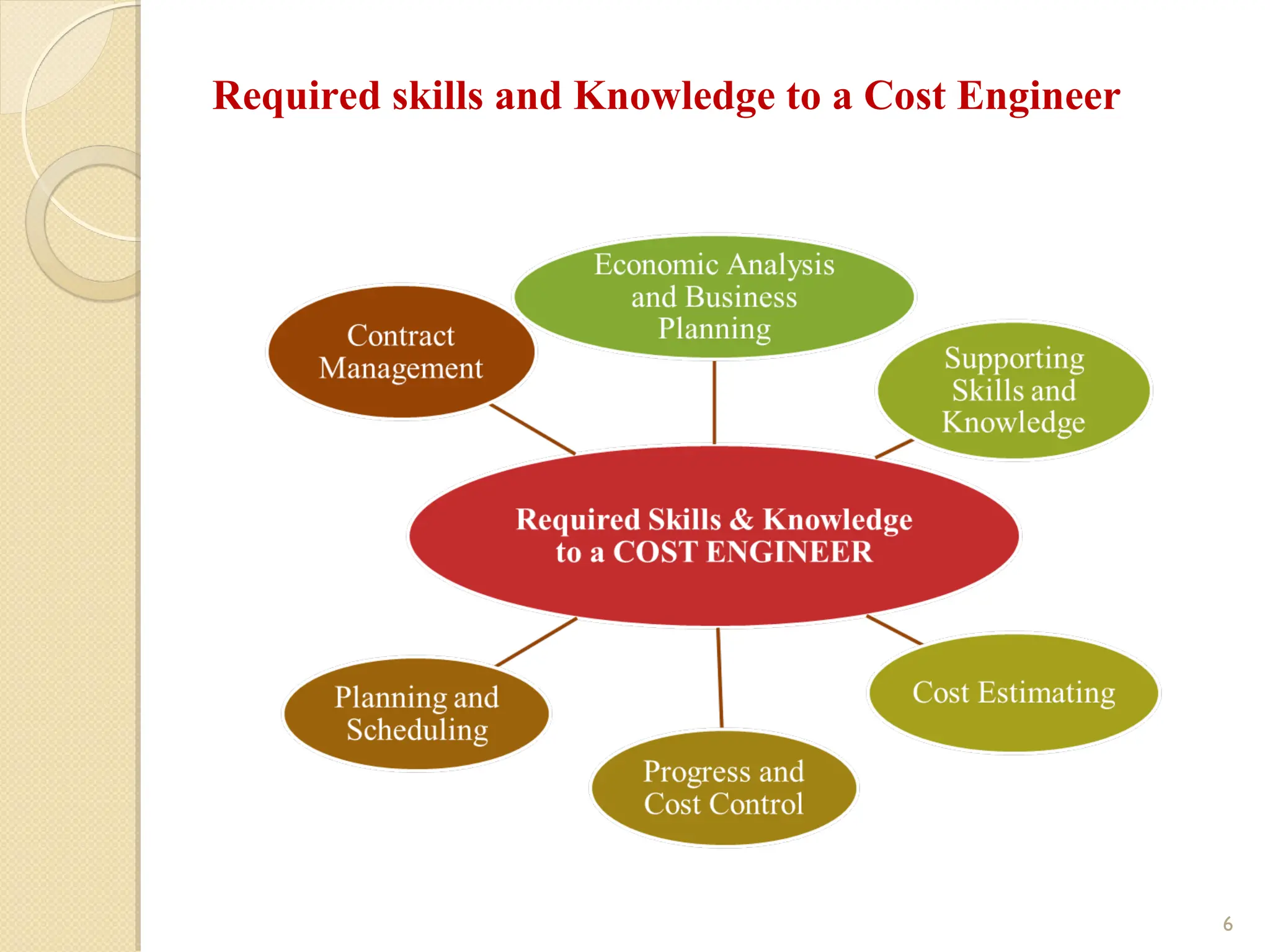

1.2 Cost Engineers

Cost Engineer: is a qualified professional dedicated to

TCM over the life cycle of a project, facility or

manufacturing operation.

Cost Engineers are responsible for carefully managing

and maintaining the integrity of all project capitalizable,

and related non-capitalizable, cost data.

A Cost Engineer determines how much money,

resources, and time a project will require prior to its

launch.

Cost Engineers may have different titles such as: cost

estimator, quantity surveyor, parametric analyst, strategic

planner, planner/scheduler, value engineer, cost/schedule

engineer, claims consultant, project manager, or project

control lead.

5

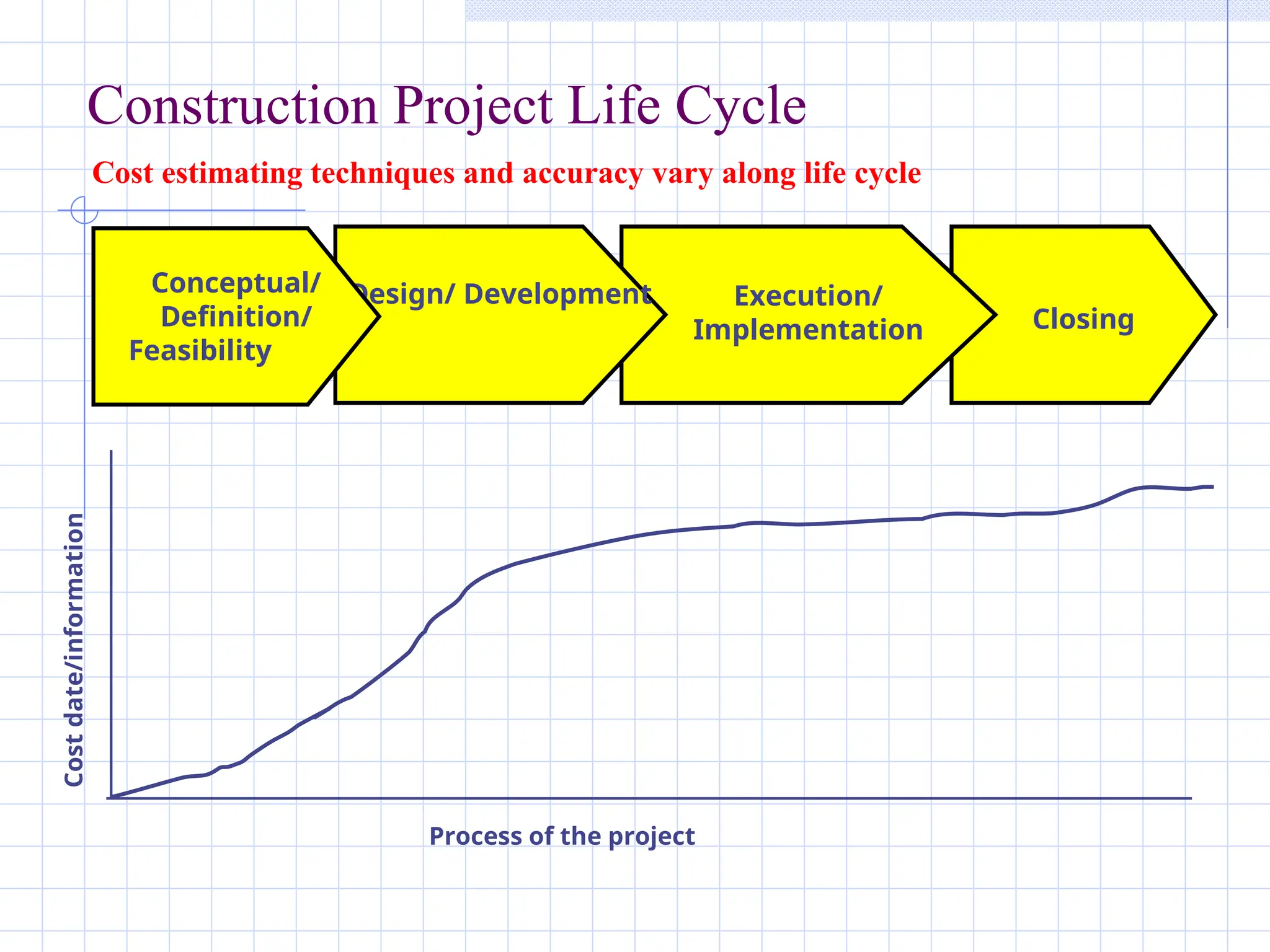

Construction Project LifeCycle

Closing

Execution/

Implementation

Design/ Development

Conceptual/

Definition/

Feasibility

Cost estimating techniques and accuracy vary along life cycle

Cost

date/information

Process of the project

8.

Cost Estimation

Cost estimatingis the process of determining quantities

and predicting or forecasting, within a defined scope, the

costs required to construct and equip a facility.

Cost estimates are performed at a certain point in time,

based on information available at the time with given

resources and time constraints.

Estimates are based on:

• Previously recorded data (historical data)

• The estimators own past experience.

• Previous experience of others.

• Hunches (Intuition).

9.

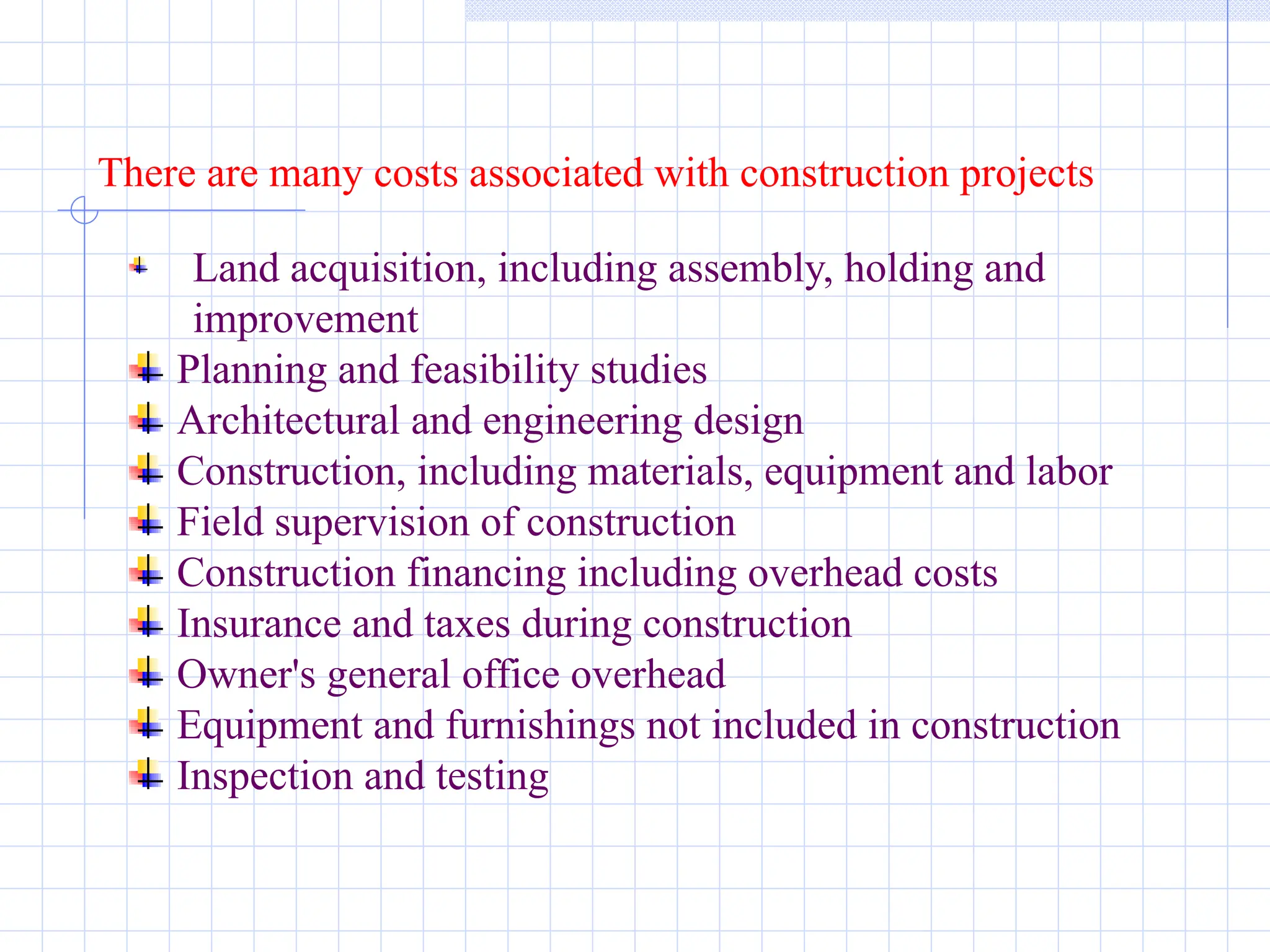

There are manycosts associated with construction projects

Land acquisition, including assembly, holding and

improvement

Planning and feasibility studies

Architectural and engineering design

Construction, including materials, equipment and labor

Field supervision of construction

Construction financing including overhead costs

Insurance and taxes during construction

Owner's general office overhead

Equipment and furnishings not included in construction

Inspection and testing

10.

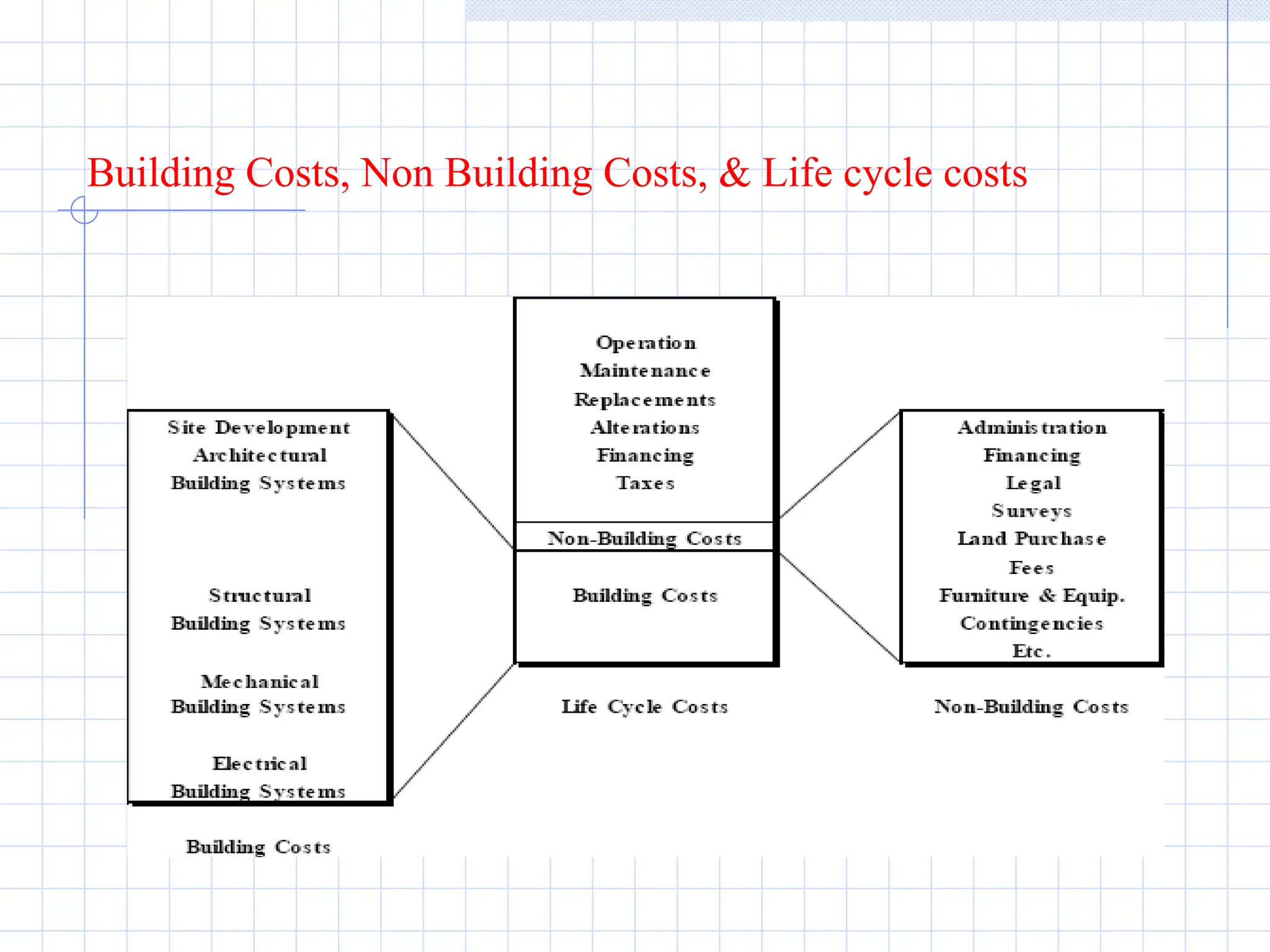

Subsequent Operation andMaintenance Costs

and rent, if applicable

perating staff

abor and material for maintenance and repairs

eriodic renovations

nsurance and taxes

inancing costs

tilities

wner's other expenses

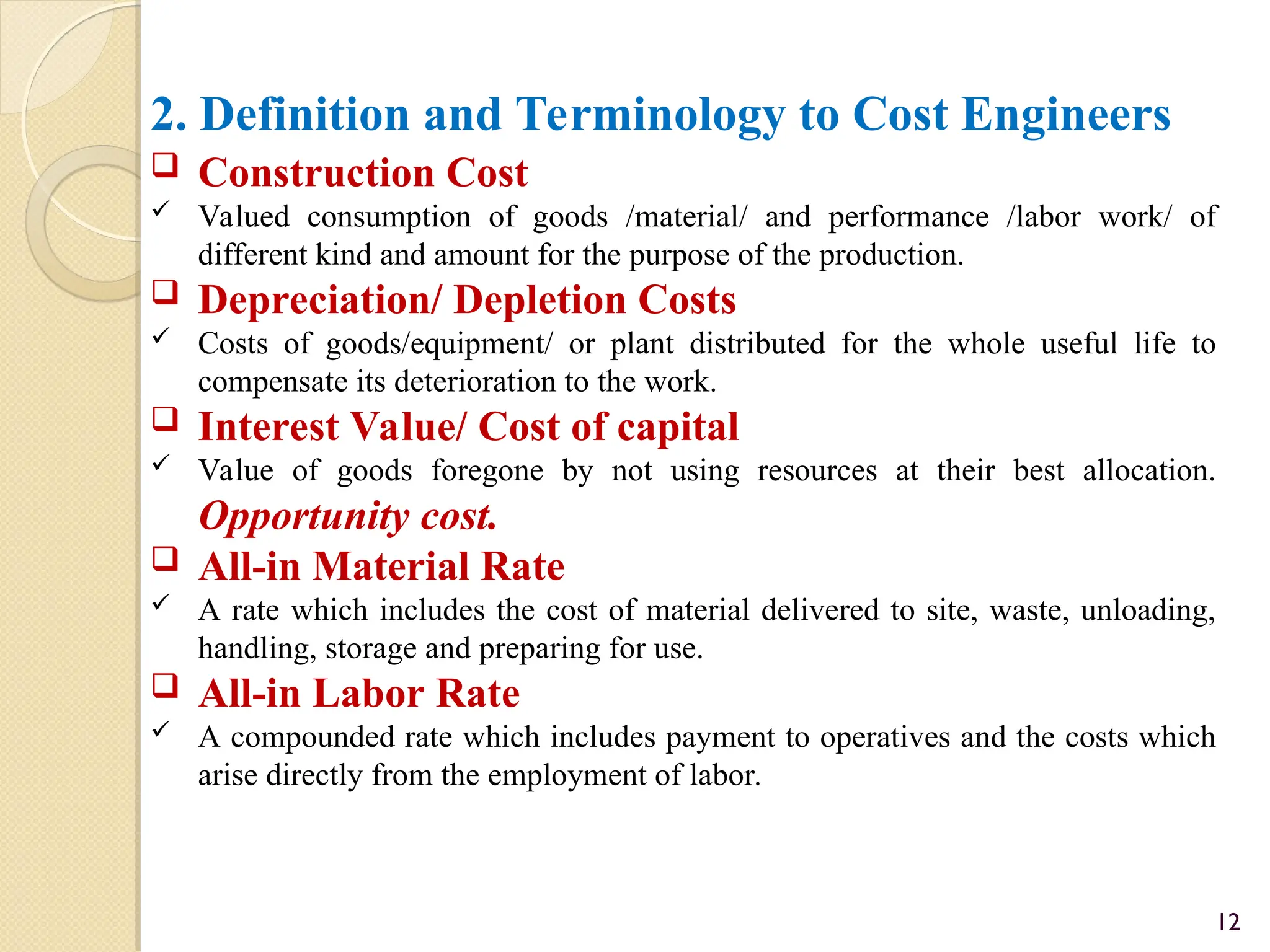

2. Definition andTerminology to Cost Engineers

Construction Cost

Valued consumption of goods /material/ and performance /labor work/ of

different kind and amount for the purpose of the production.

Depreciation/ Depletion Costs

Costs of goods/equipment/ or plant distributed for the whole useful life to

compensate its deterioration to the work.

Interest Value/ Cost of capital

Value of goods foregone by not using resources at their best allocation.

Opportunity cost.

All-in Material Rate

A rate which includes the cost of material delivered to site, waste, unloading,

handling, storage and preparing for use.

All-in Labor Rate

A compounded rate which includes payment to operatives and the costs which

arise directly from the employment of labor.

12

13.

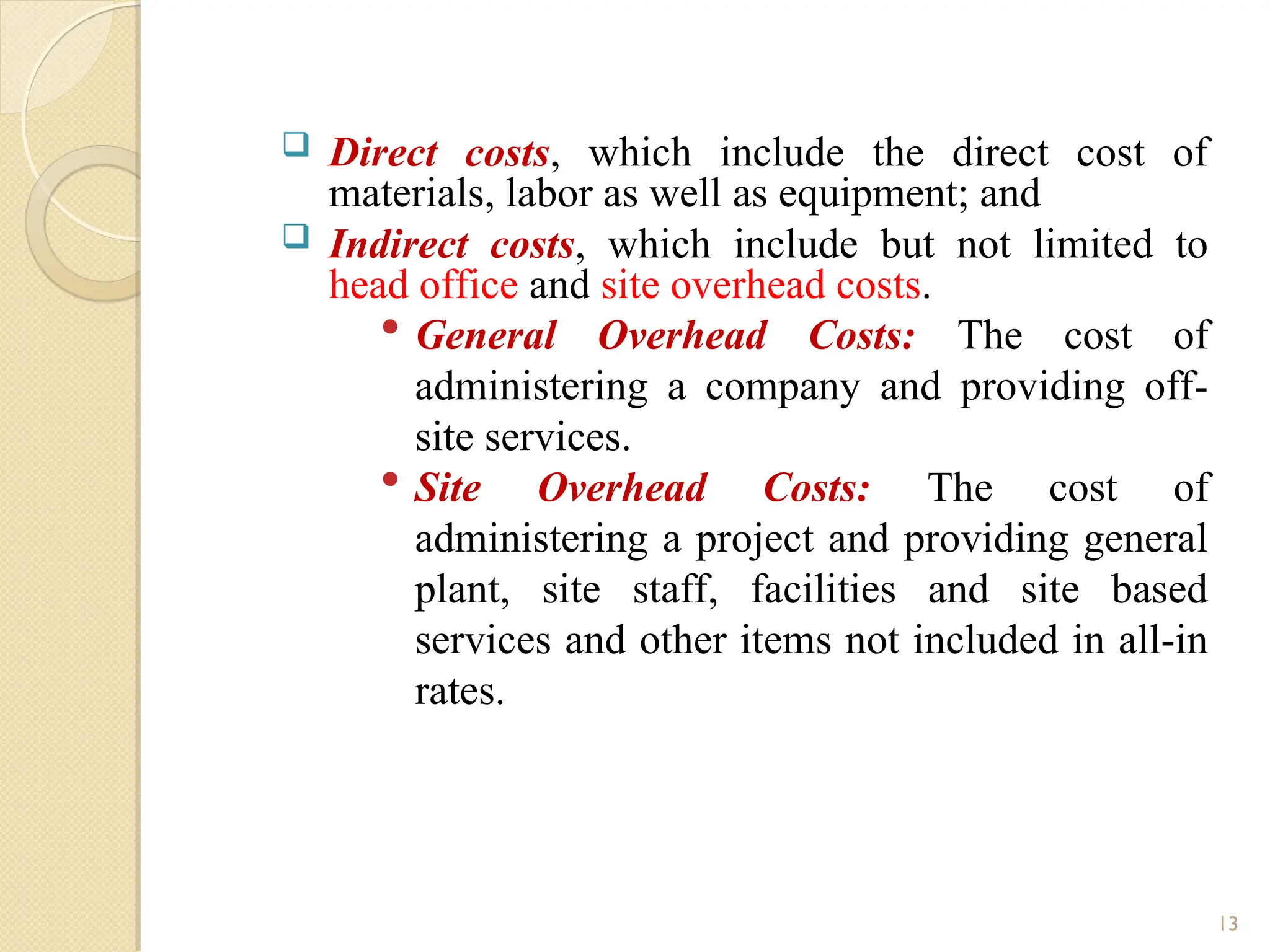

Direct costs,which include the direct cost of

materials, labor as well as equipment; and

Indirect costs, which include but not limited to

head office and site overhead costs.

General Overhead Costs: The cost of

administering a company and providing off-

site services.

Site Overhead Costs: The cost of

administering a project and providing general

plant, site staff, facilities and site based

services and other items not included in all-in

rates.

13

14.

Mark-up Cost

The sum added to an estimate in respect of the general

overhead costs including profit and risk.

Production Cost

Costs representing the sum of direct costs (all-in costs)

and site overhead costs.

Costs required for production of the works on site.

14

15.

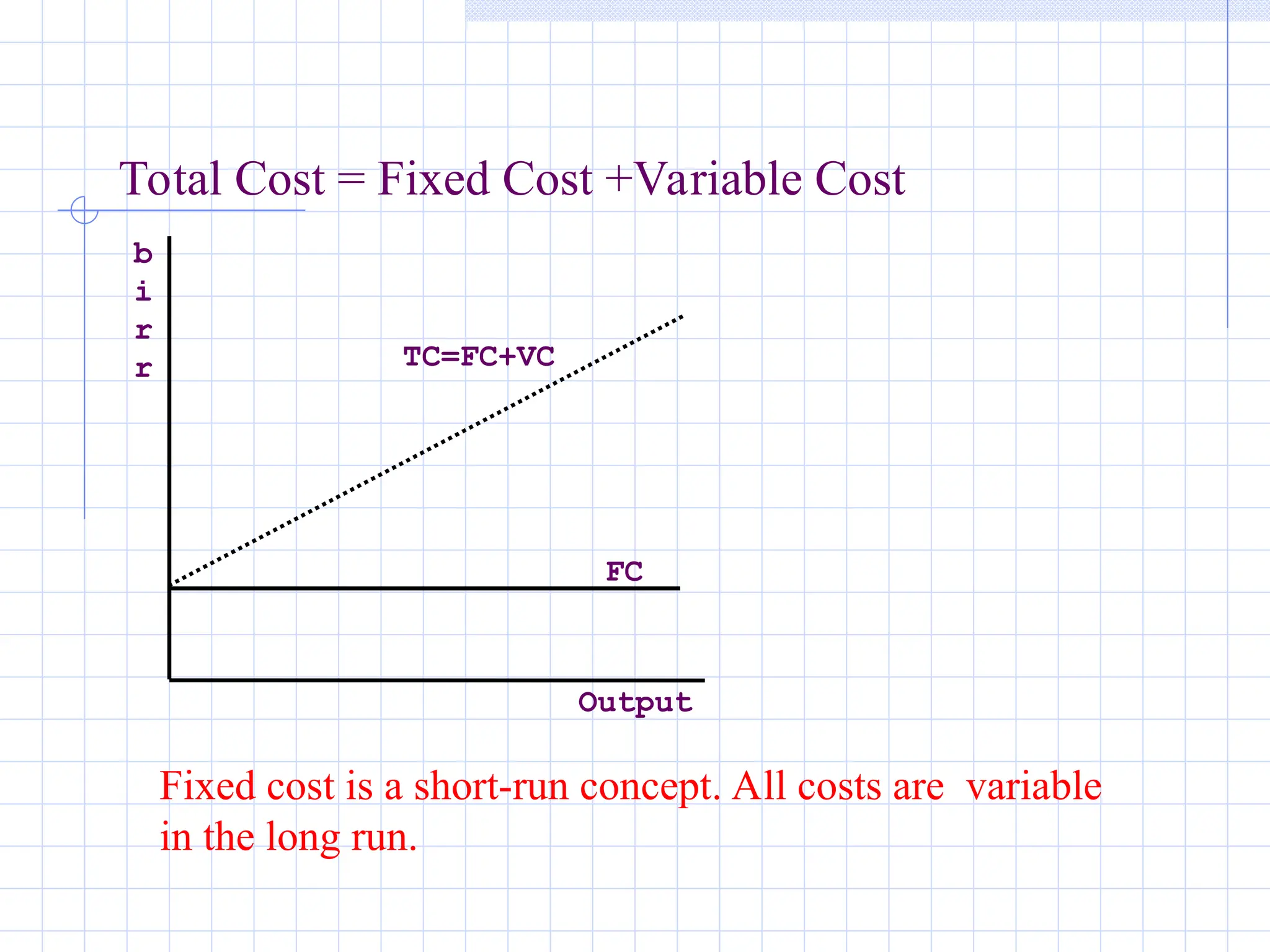

Total Cost =Fixed Cost +Variable Cost

b

i

r

r

FC

Output

TC=FC+VC

Fixed cost is a short-run concept. All costs are variable

in the long run.

16.

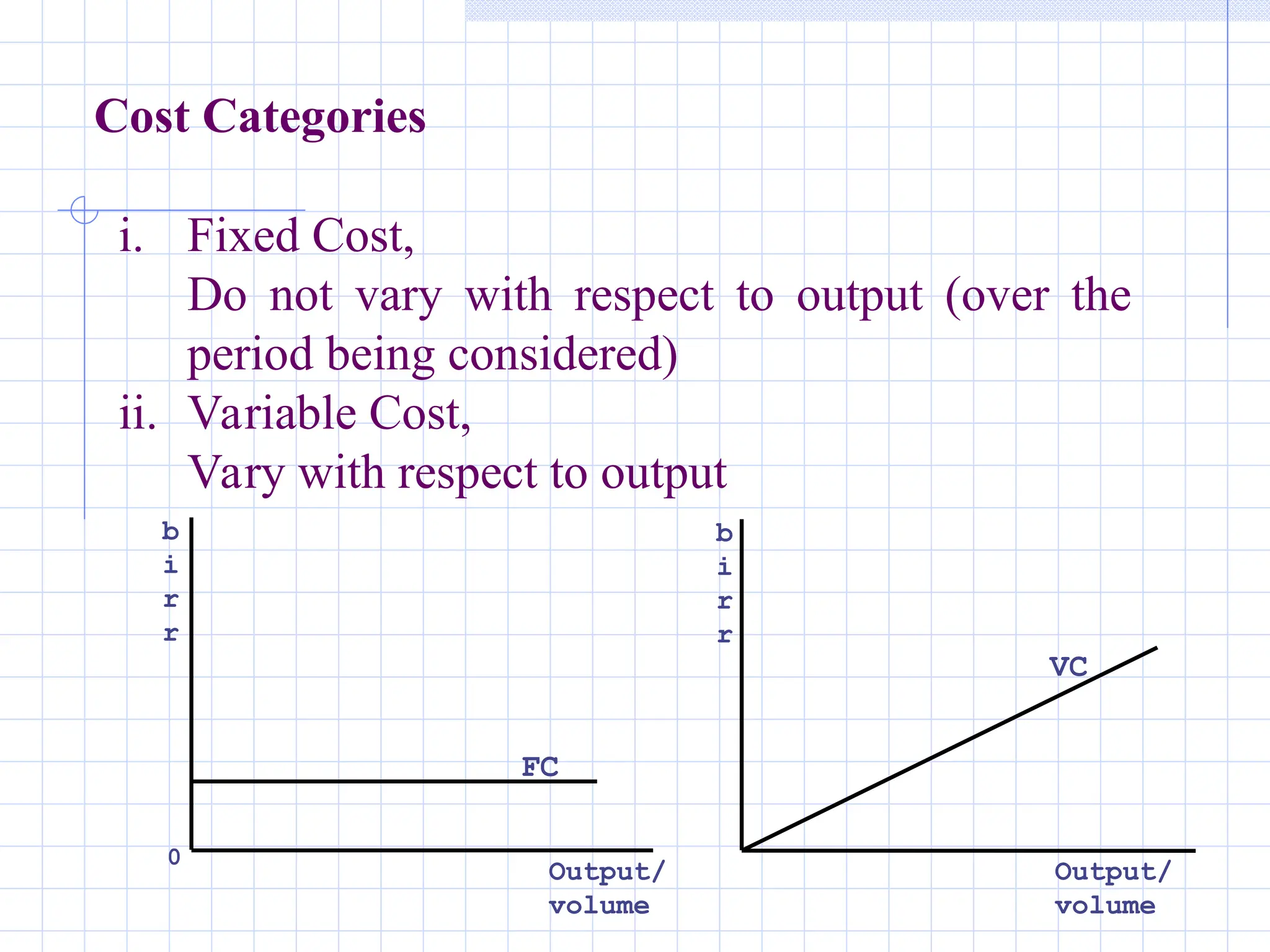

Cost Categories

i. FixedCost,

Do not vary with respect to output (over the

period being considered)

ii. Variable Cost,

Vary with respect to output

b

i

r

r

FC

0

Output/

volume

b

i

r

r

VC

Output/

volume

17.

3. Cost EngineeringTraits

Cost Engineering shares common traits of the following:

Conflicting Issues of quality, size, performance and cost

As projects develop, there is continual competition among

issues of quality, size, performance and cost.

Owners want to have the biggest facility with the best

finishes and systems that will perform over time with least

possible amount of money. With these criteria, it is likely

that conflicts are bound to arise.

17

18.

Cost Engineeringcombines both science and art:

Cost estimates are a product of information supplied by the

designer, the owner and the suppliers.

Experienced Cost Engineers use much judgment in

interpreting and configuring this information.

Cost Engineering does not offer guarantees of costs: Used

properly, however, can be important tool in bringing a

project under or at budget.

The costs developed during design and even at the bidding

stage are almost never the final and complete costs of the

project.

18

19.

Costing canonly be as accurate as the information upon which

it is based:

Cost accuracy depends on many factors. Document

completeness, data base accuracy, the skill and judgment of the

Cost Engineer.

Cost estimate accuracy increases as the design becomes more

precisely defined:

A normal feature of the design process is that earlier stages of

design are less precise than later stages.

Cost information provided at schematic and preliminary design

will by nature be less accurate than the ones provided at design

developments.

19

20.

Cost estimateis based on previous estimates:

A good, accurate estimate does not stand alone. It is the

product of lessons learned from previous estimates.

Costing requires standard computing methodology and

procedures:

As the design proceeds, the level of details increases.

Costing as a consequence becomes more complex

reflecting the many different factors that go into each

unit of work.

20

21.

4. Functions ofCost Engineering in Construction

Arranging finance, administrative approval and fund

allotment

Guide decision making among alternatives

Provides guidelines to the designer (on material, size

Prepare engineering estimate

Negotiation tool between contracting parties

Help in fixing completion periods

To justify investment : Cost benefit analysis

To invite tenders

For Valuation purposes

21

22.

5. Considerations inCosting

Project price is affected by

i. size of the project,

ii. quality of the project,

iii. Location of the project,

iv. construction time, and

v. other general market conditions.

22