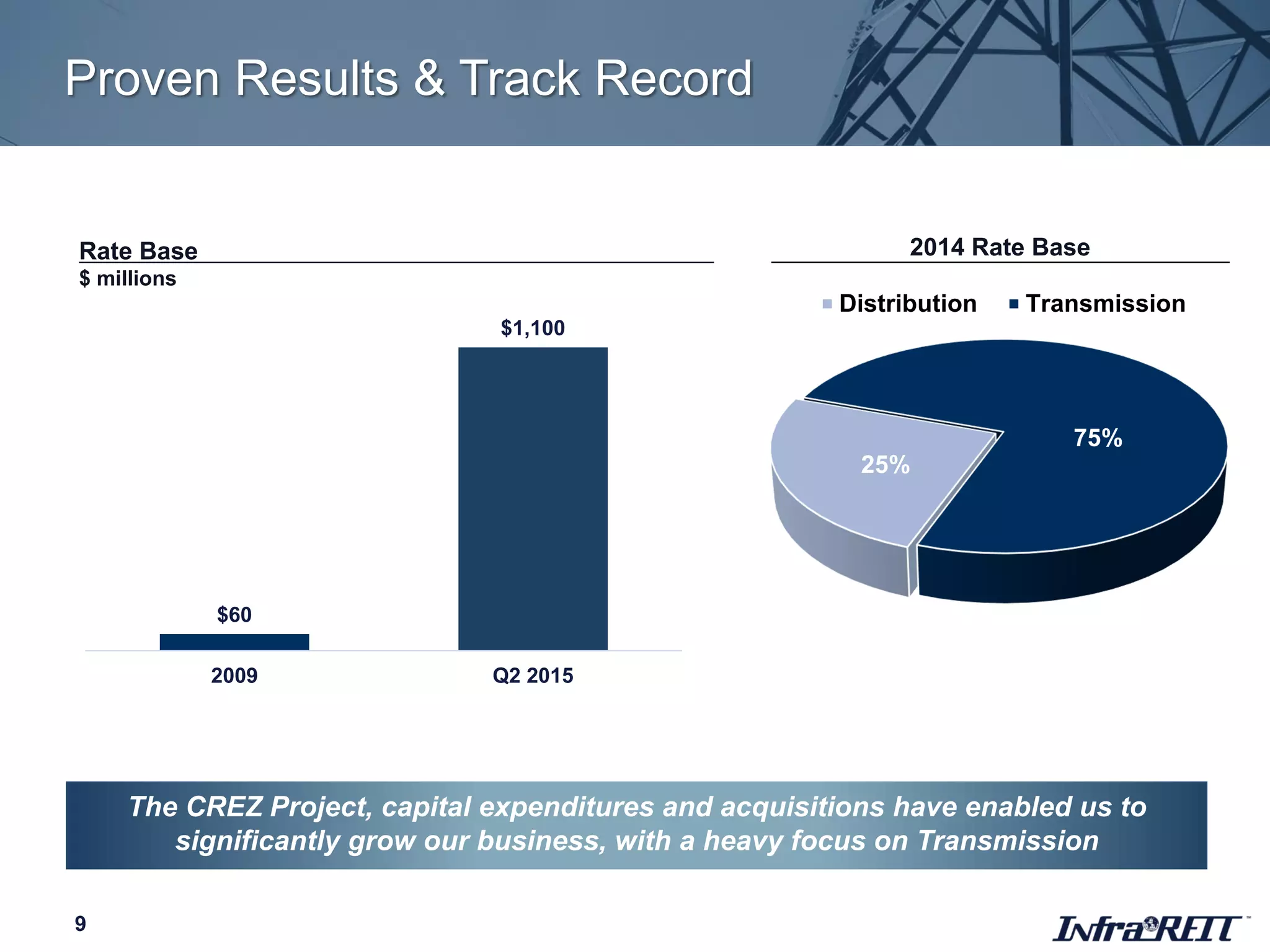

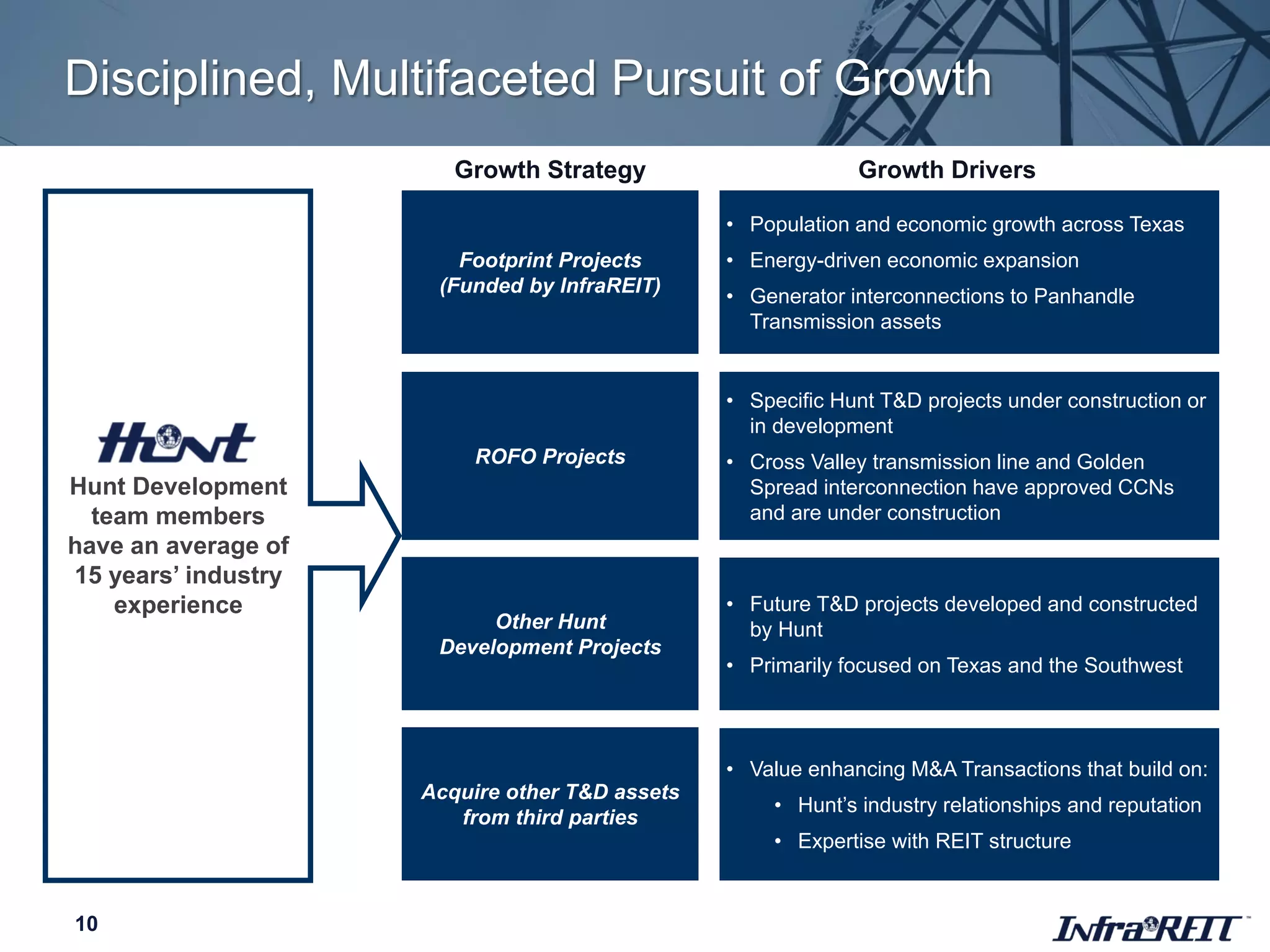

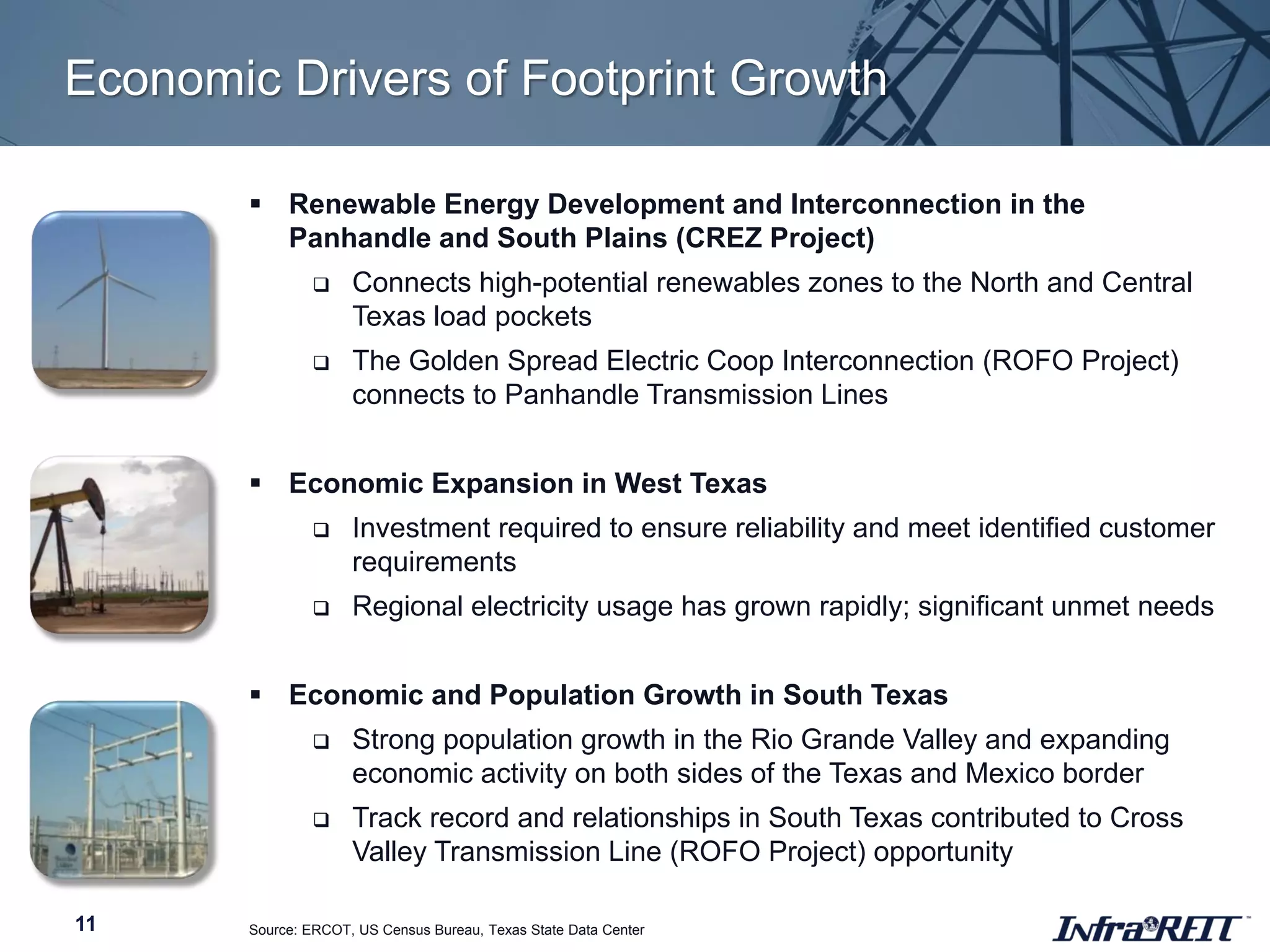

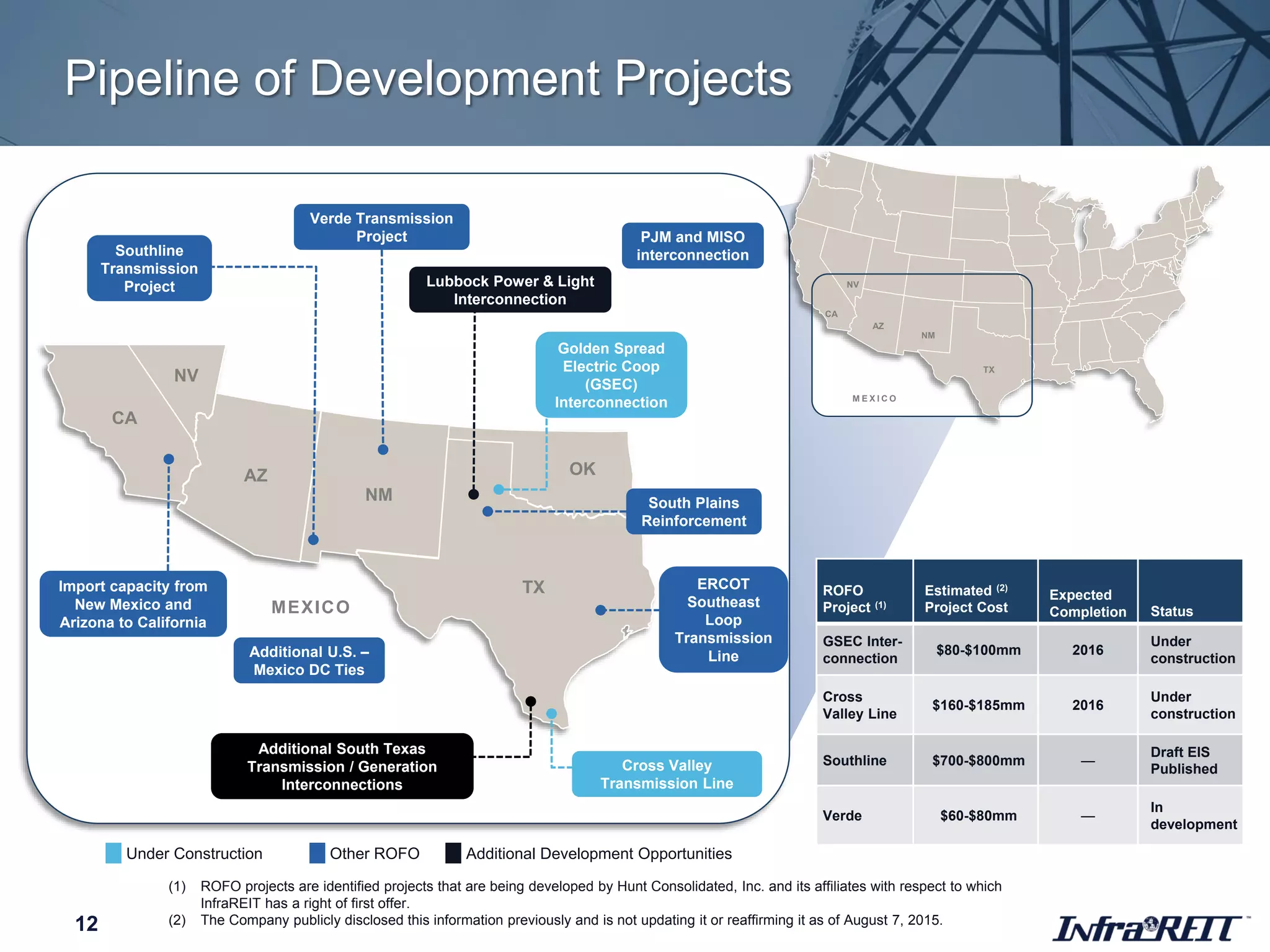

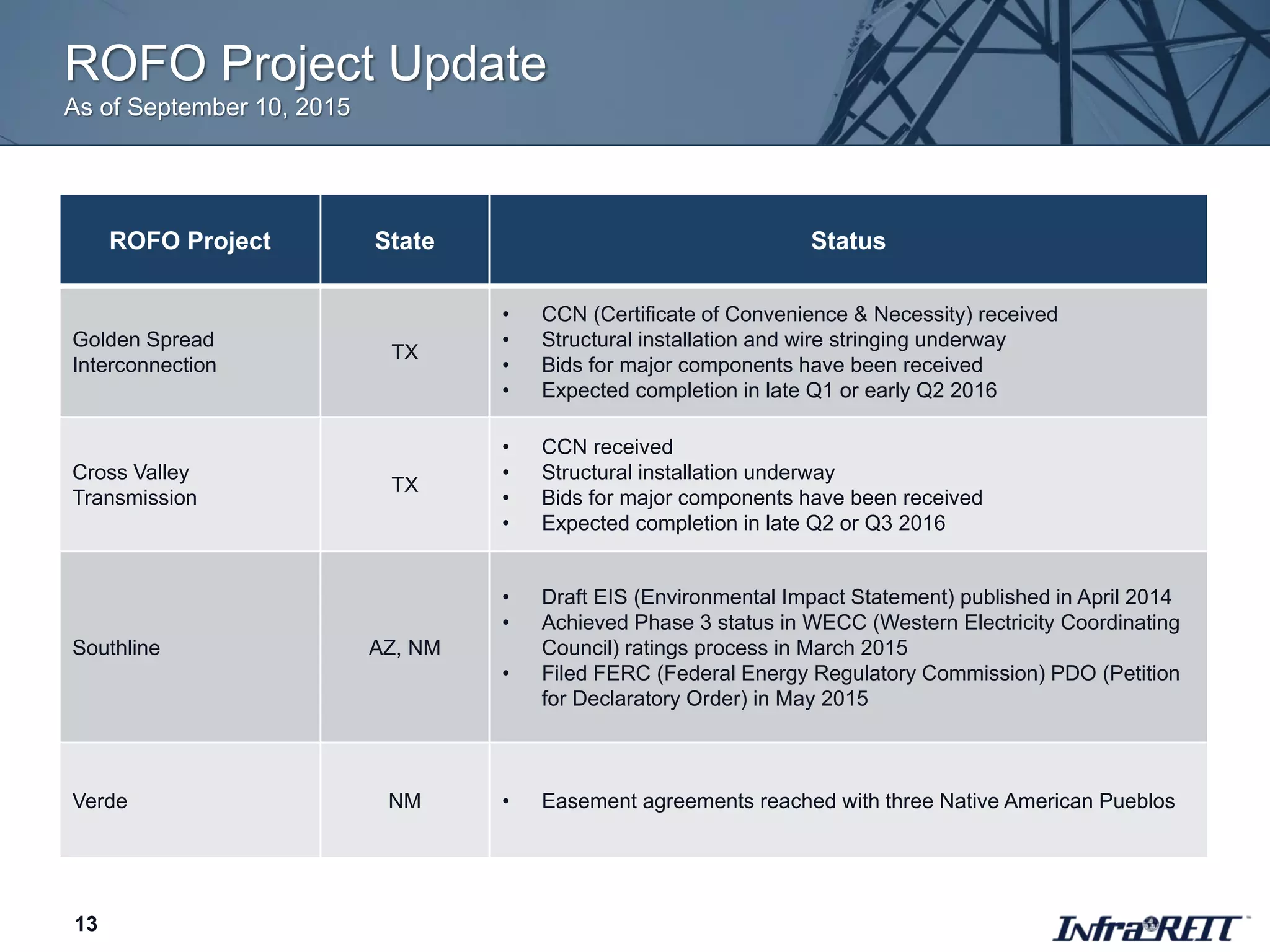

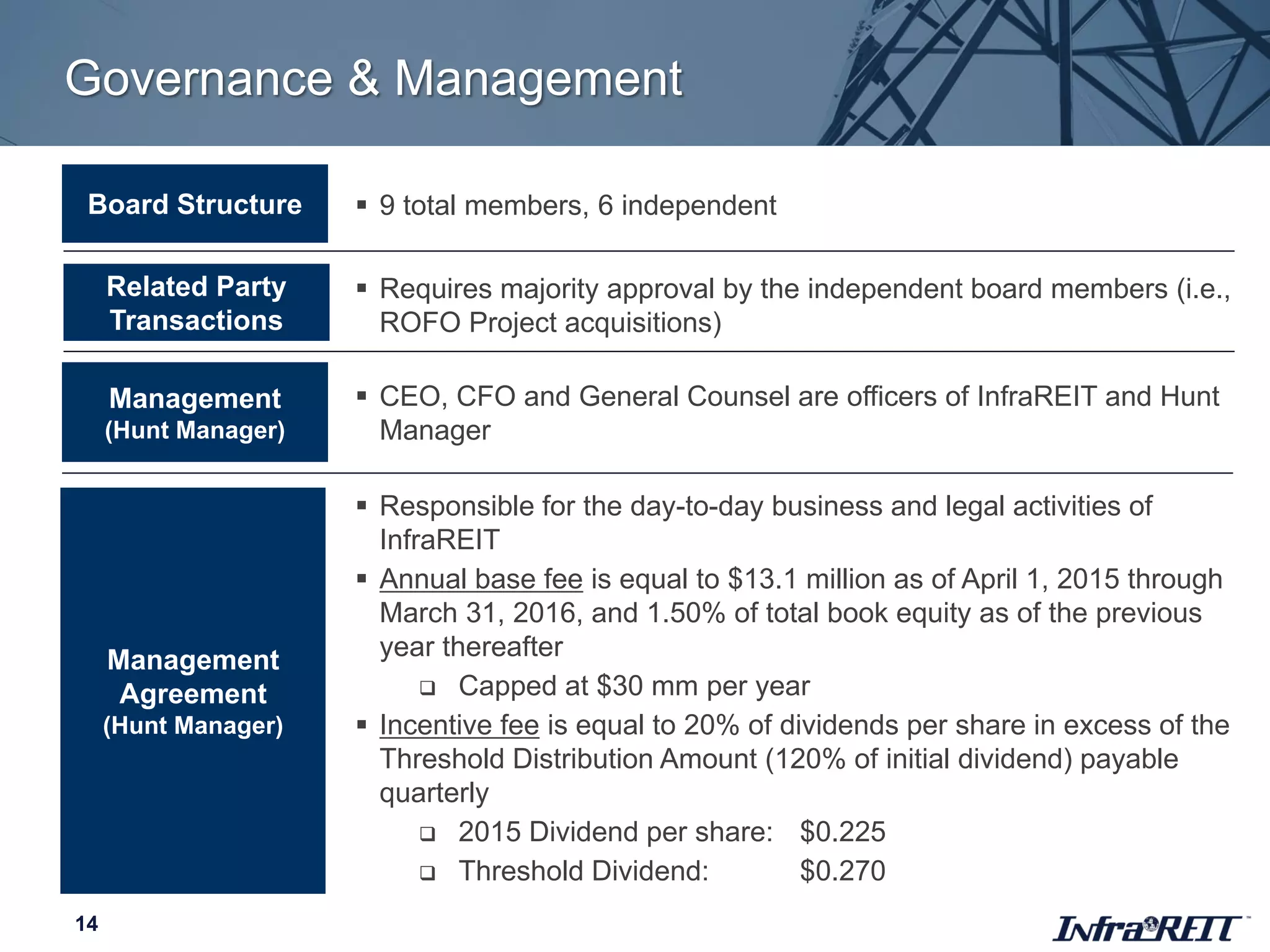

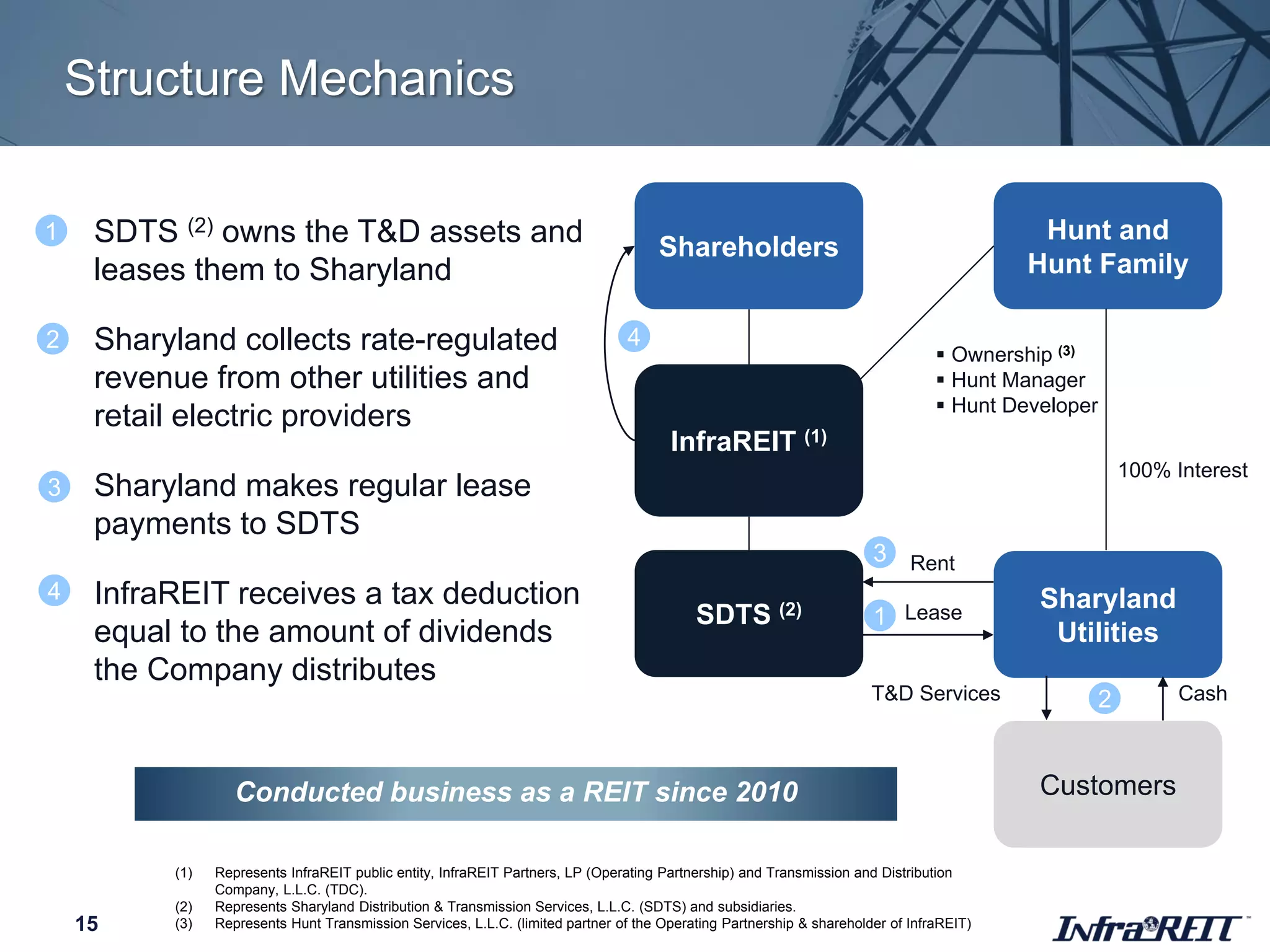

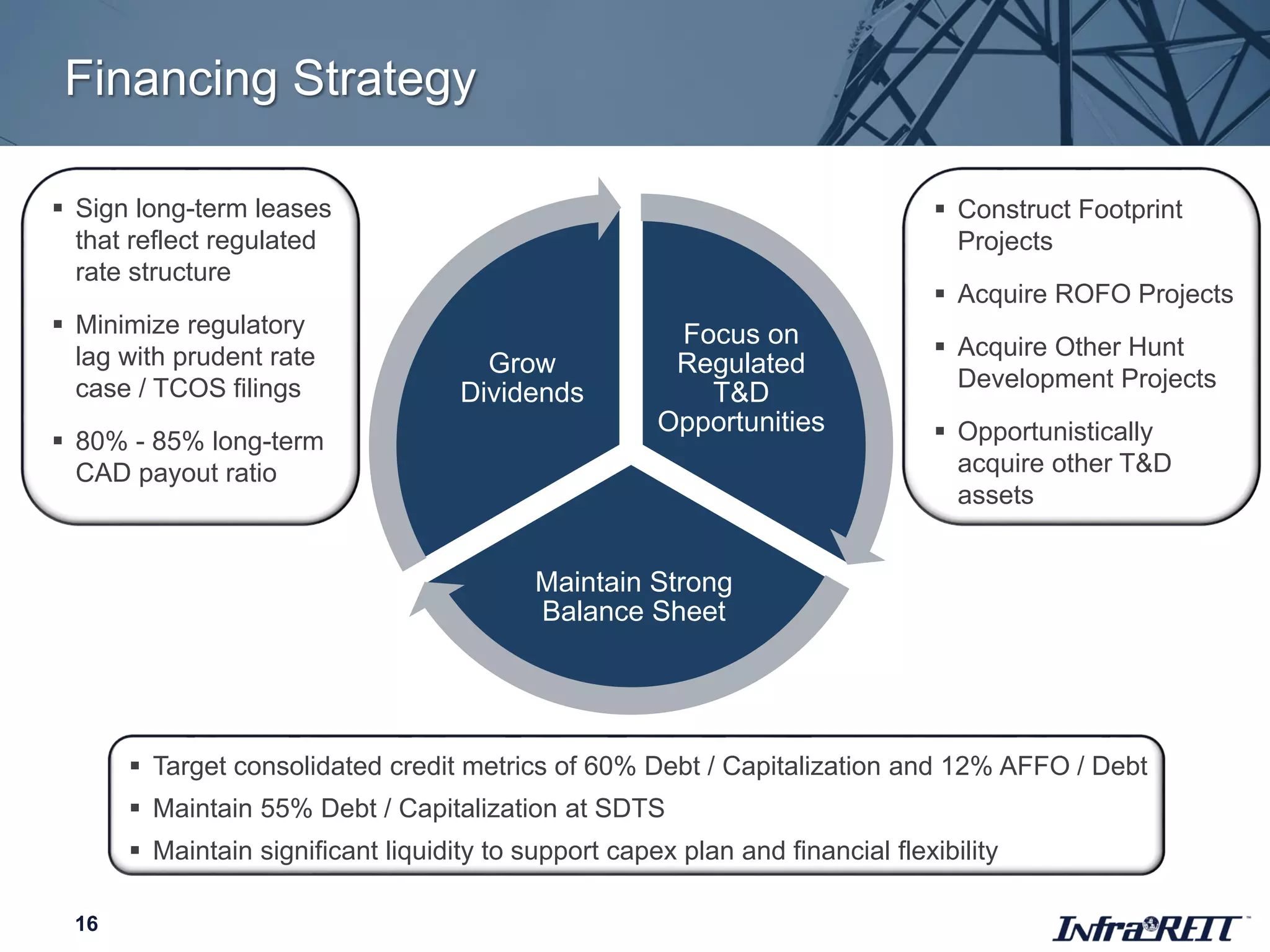

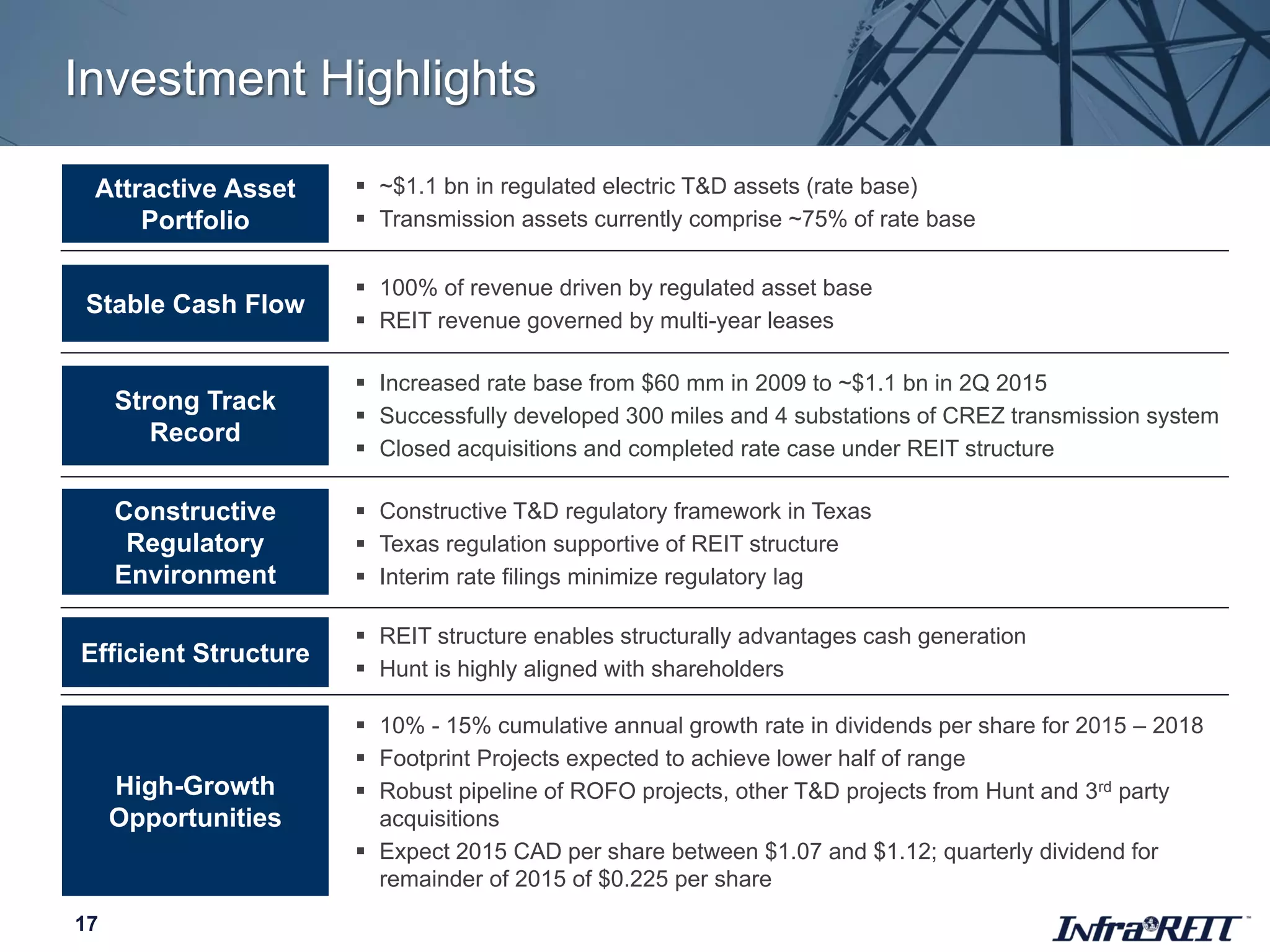

InfraREIT provided a corporate update in September 2015. The document discusses InfraREIT's asset portfolio of $1.1 billion in regulated electric transmission and distribution assets located primarily in Texas. It highlights InfraREIT's stable cash flows from long-term leases of its regulated assets and its track record of significant growth through developing projects and acquisitions. The update also outlines InfraREIT's growth opportunities through further developing projects in its footprint, acquiring additional rights of first offer projects from Hunt, and pursuing third party acquisitions, with the goal of achieving double-digit annual growth in cash available for distribution.