The document provides an overview of InfraREIT's recent performance and events. Some key points:

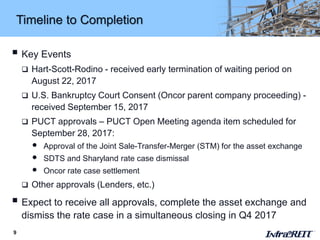

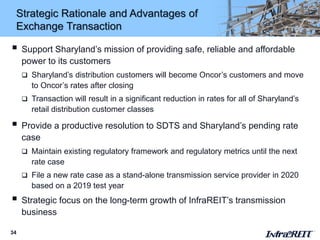

- InfraREIT reached agreements for an asset exchange transaction with Oncor and proposed dismissal of a rate case.

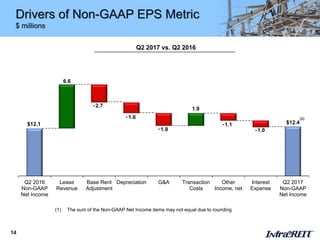

- InfraREIT reported solid Q2 2017 performance with increases in lease revenue and net income. Non-GAAP metrics were consistent with prior year.

- The asset exchange and rate case dismissal are expected to close simultaneously in Q4 2017 pending required regulatory approvals.