- Monetary policy aims to control money supply, contain inflation, stabilize exchange rates, and maintain balance of payments equilibrium. This helps support macroeconomic stability.

- Pakistan's economy grew reasonably well in recent years, with GDP growth reaching 4.04% in FY2015 and 4.71% in FY2016, despite slower global growth and economic challenges. Private sector credit expansion has helped manufacturing and industry.

- Broad money supply (M2) increased 6.93% during the period as net domestic assets grew. However, net foreign assets only saw modest growth as scheduled bank foreign assets declined slightly while SBP foreign assets grew.

![Pakistan Economic Survey 2015-16

84

Overall credit grew by 7.2 percent during Jul-Mar,

FY2016 as compared to 6.9 percent during the

comparable period of last year FY2015.Sector

wise growth demonstrates that loans to private

sector business witnessed a significant growth of

8.3 percent during Jul-Mar, FY2016 against 6.6

percent in same period of last year.

In flow terms, credit expansion to private business

reached to Rs.249.0 billion during July-March,

FY2016 as compared to Rs.187.6 billion in the

corresponding period of FY 2015.The expansion

in credit to private sector is broad based during

FY 2016 and mainly came from construction

(40.5 percent), followed by Electricity, Gas and

Water supply (14.9 percent), Transport, Storage

and Communication (14.3 percent),

Manufacturing (12.1 percent) of which Textile by

(15.0 percent).The expansion in private sectors

loans during Jul-Mar, FY2016 primarily in

Manufacturing sector that received share 82.9

percent of private sector loan (Rs. 206.4 billion),

followed by textile (33.1 percent or Rs. 82.5

billion), Electricity, Gas and Water supply (16.0

percent or Rs.39.8 billion), construction (10.7

percent or Rs.26.7 billion) and transport, storage

and communication (8.4 percent or Rs. 20.9

billion).

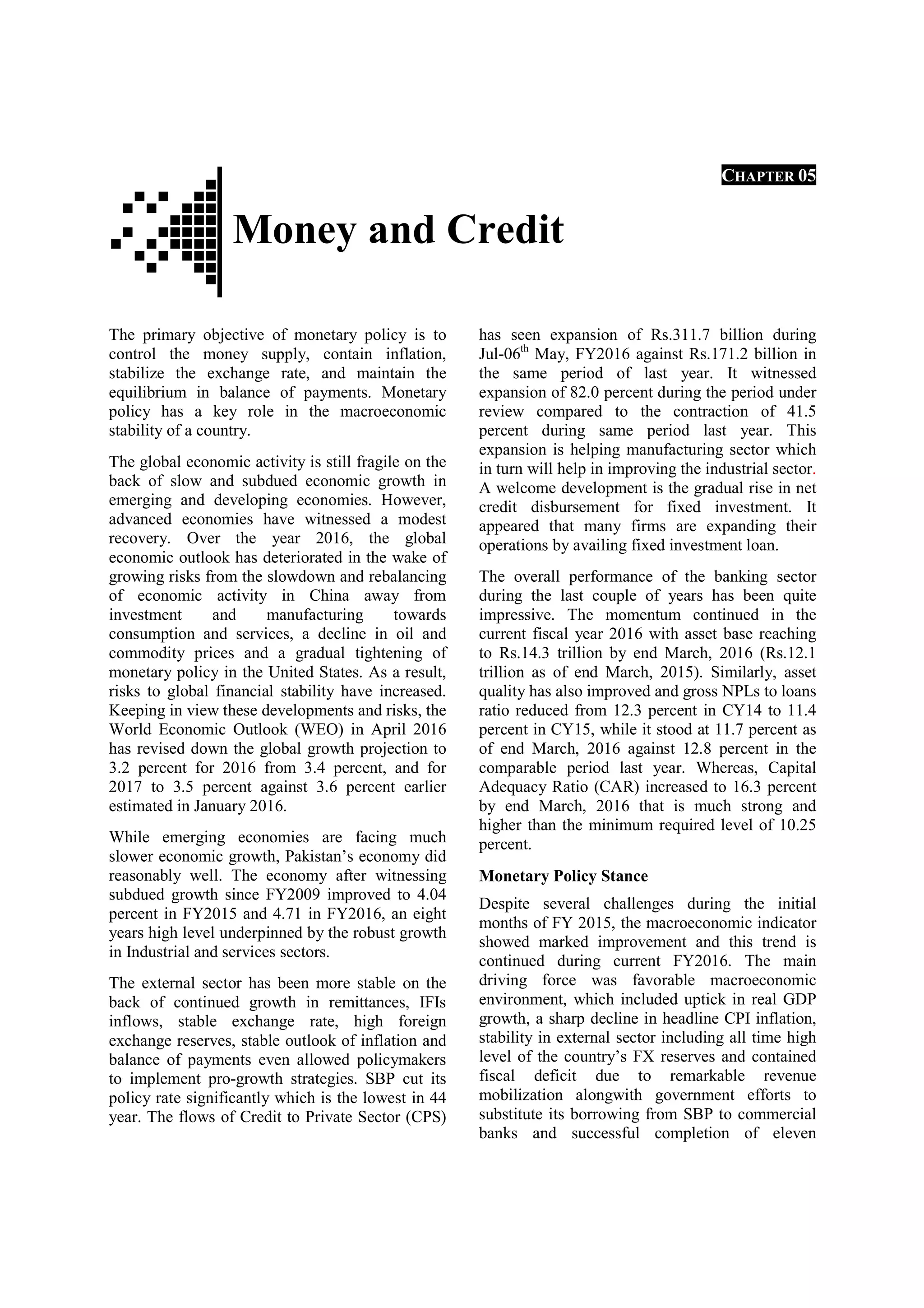

Table 5.4: Loans to Private Sector Businesses [Jul-Mar (Flows)] Rs. Billion

Total Credit Working Capital Fixed investment Trade financing

FY15 FY16 FY15 FY16 FY15 FY16 FY15 FY16

Total 185.1 319.8 50.6 119.2 84.4 150.1 50.2 50.4

Agriculture 14.3 -1.4 6.8 -7.4 8.2 6.1 -0.7 -0.1

Manufacturing 104.6 206.4 26.7 116.5 44.0 34.1 34.0 55.7

Food & beverages 56.8 68.7 24.2 42.9 17.2 11.9 15.4 13.9

Textiles 29.5 82.5 15.9 58.0 1.8 9.3 11.8 15.1

Coke & petroleum 18.0 10.4 10.7 1.9 9.1 -5.9 -1.7 14.4

Chemicals 1.9 33.1 -8.1 22.1 11.4 7.5 -1.4 3.5

Electricity -3.2 39.8 1.0 13.0 -6.0 31.9 1.9 -5.1

Construction 11.0 26.7 -2.0 -2.6 11.3 28.1 1.8 1.3

Commerce and trade 11.1 11.3 -0.4 4.0 7.8 7.1 3.7 0.1

Transport & comm. 9.9 20.9 7.1 -9.2 2.6 30.2 0.2 0.0

Real estate 17.8 7.1 6.3 3.2 11.7 1.0 -0.2 3.0

Others -1.8 -9.8 2.4 -1.9 -1.3 3.3 -0.4 0.5

Source: State Bank of Pakistan

The credit to private sector has witnessed

significant growth by type of finance during Jul-

Mar, FY2016 for working capital, fixed

investment and trade financing categories as

compared to same period of last year. The gradual

increase in credit disbursement for all categories

mainly used by major sectors of the economy and

particularly notable in production, transmission

and distribution of electricity; road transport;

construction of roads; telecommunications; sugar;

manufacturers of electricity distribution

machinery; cement; fertilizer; and pharmaceutical

sectors. Credit for fixed investment reached to

Rs.150.1 billion (increase by 78.0 percent) during

Jul-Mar, FY2016 against Rs.84.4 billion in

comparable period of FY2015, working capital

credit amounted to Rs.119.2 billion (grew by

135.8 percent) during the Jul-Mar, of FY2016 as

compared to Rs.50.6 billion in same period of last

year, similarly trade financing increased to

Rs.50.4 billion (grew by marginally 0.44 percent)

in Jul-Mar, FY2016 from Rs.50.2 billion in the

corresponding period of last year FY2015.

A continuation of credit demand requires

favourable monetary conditions and improvement

in performance of manufacturing and services

sectors. Realization of this could augur well for

growth in private sector going forward2

.

2

2nd

Quarterly Report FY16, SBP](https://image.slidesharecdn.com/05moneyandcredit-210914040059/85/05-money-and_credit-6-320.jpg)