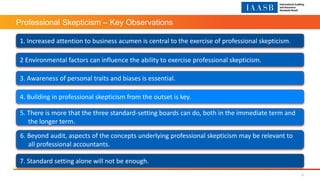

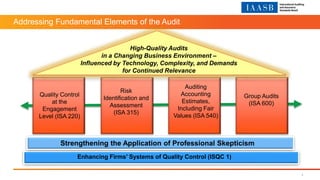

1. The document discusses enhancing professional skepticism in auditing. It notes that increased attention to business acumen, awareness of personal biases, and building in skepticism from the outset are key to exercising skepticism. 2. It also recommends that the standard-setting boards can do more to strengthen the application of professional skepticism, both immediately and long-term, including in areas like accounting estimates, group audits, and risk assessment. 3. Beyond auditing, aspects of professional skepticism may also be relevant for all professional accountants. However, standard-setting alone will not be enough, and other stakeholders must also play a role in supporting high-quality financial reporting.