Recommended

Recommended

More Related Content

Similar to Issue or ConsiderationSole Prop.General PartnershipLimited P.docx

Similar to Issue or ConsiderationSole Prop.General PartnershipLimited P.docx (15)

More from priestmanmable

More from priestmanmable (20)

Recently uploaded

Recently uploaded (20)

Issue or ConsiderationSole Prop.General PartnershipLimited P.docx

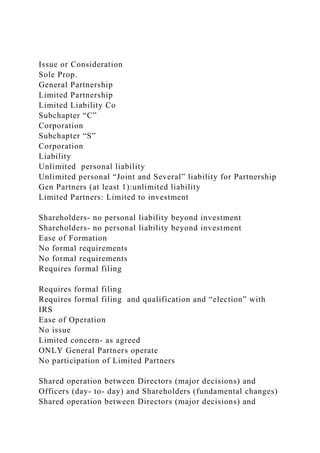

- 1. Issue or Consideration Sole Prop. General Partnership Limited Partnership Limited Liability Co Subchapter “C” Corporation Subchapter “S” Corporation Liability Unlimited personal liability Unlimited personal “Joint and Several” liability for Partnership Gen Partners (at least 1):unlimited liability Limited Partners: Limited to investment Shareholders- no personal liability beyond investment Shareholders- no personal liability beyond investment Ease of Formation No formal requirements No formal requirements Requires formal filing Requires formal filing Requires formal filing and qualification and “election” with IRS Ease of Operation No issue Limited concern- as agreed ONLY General Partners operate No participation of Limited Partners Shared operation between Directors (major decisions) and Officers (day- to- day) and Shareholders (fundamental changes) Shared operation between Directors (major decisions) and

- 2. Officers (day- to- day) and Shareholders (fundamental changes Taxation No additional tax issue or burden Partnership return with Pass through to individual partners Partnership return with Pass through to individual partners Possibility of double taxation Avoids possibility of double taxation Capitalization Limited to loans (usually banks) Limited to loans (usually banks) Also have limited partner investment Issue stock or Bonds Issue stock or Bonds Duration Limited duration Limited duration Limited duration (gen. Partners) flexibility with limited partners Perpetual Perpetual Alienation No No No-General Possible with Limited partners Simple stock transfer Simple stock transfer Partnership Form of Business The partnership is defined as the type of business operation

- 3. formed between two or more persons interested in a common course: Making profits. The government recognizes a few kinds of partnerships (Lorette, n.d., para. 1). At the point when setting up an association, the first thing you will need to do is pick a name for the organization. While this may sound basic, it is imperative to make certain the name does not abuse the trademark privileges of another business. There are a few approaches to figure out whether another business as of now, has such a name. Firstly, one can do a name search online on the U.S. Patent and Trademark Office website. Also, one can conduct an inquiry of enrolled entrepreneurs. However, this procedure is followed via the legal office (secretary of state.) Likewise, partners should decide the specifics of how the organization will be overseen, how much every accomplice will contribute, and how the benefits will be shared. While the more prominent the extent of the venture implies the bigger the rate of proprietorship, the greatest investor may not even need to maintain the business. Additionally, while you may confirm that all accomplices have equal force in choice making, certain accomplices ought to be recognized as having the power to settle on choices on everyday operations and the general administration of the business. Making prior auxiliary determinations will guarantee that the enterprise begins off quickly. Two types of partnership are most common; they include limited and general partnerships. If the business more than one person, it is wise to considers setting it up as a partnership. As such, partnership presents itself in two ways: general and limited partnerships. In the former, the accomplices familiarize and accept duties regarding the businesses policies and responsibilities. The latter has general and limited partners. General partners are the owners who control the business and have set out specific responsibilities to specific partners. On the other hand, restricted accomplices assume the role of investors; therefore, it means that they have no power over the organization; and

- 4. hence, they cannot be subjected to similar liabilities with the general partners. Not if there is an expectation of numerous inactive speculators, limited partnerships are not deemed to be the best choice. The reason is the required filings and organizational complexities. One of the real focal points of an organization is the tax treatment it enjoys. A partnership is not inclined to pay a charge on its wage, however, it must pass the generated profits and incurred losses to the business partners. In the event of taxation, a partnership must document a government form that provides sufficient details about revenues or incomes and its losses. Likewise, partners are required to give relevant details of their profits and losses. Personal risk is a critical factor when one considers setting up any form of partnership. Similar to entrepreneurs, general partners assume liability on an individual level, the dangers of the partnership’s responsibilities and commitments. Notably, a major partner can monitor and also represent for business. For instance, they can take out advances and agree on choices that are expected to impact and bind the partners if the terms of the agreement allow it. Likewise, it is imperative to note that partnership is costly compared to sole-proprietorships. The reason is that they require more complicated legal procedures and book-keeping practices. If one chooses to come up with a partnership form of business, it is essential to set up an association agreement that highlights means of making business choices, debating strategies, and dealing with a buyout. It is helpful if for unknown reasons there is a disagreement between partners or when a person needs to take advantage of a similar game plan. Such an agreement addresses the motivation behind the business and the power entitled to every partner, and their responsibilities in the enterprise. Similarly, “it is important to seek legal advice from a lawyer with sufficient experience in the business realm to aid in making the agreement” (Sba.gov, n.d.) For instance, it stipulates clearly the mode of making

- 5. decisions. Likewise, it is crucial to come up with a voting strategy and exclusive voting rights if a disagreement arises among partners. Notably, if the partners have exactly equal shares, there's the likelihood of a gridlock. To evade such a situation, it is a common practice for some business to involve a third partner in advance. As such, it should be a trusted partner entitled to one percent of the company, and who has critical vote necessary for breaking a tie. The other important factor is sharing of interests among partners. It is cumbersome, for two proprietors to just as offer possession and power. On the other hand, if one chooses to do it, one must ensure the proportion is expressed unmistakably in the agreement. From a source of capital perspective, “partnerships get their money via loans, plowed back profits, additional partners, and also individual contributions” (Lorette, n.d.) Taking everything into account, partnerships can be said to be moderately inexpensive and with structures that are simple to establish. A lot of time used in coming up with a partnership is consumed during the formation of the association agreement. Also, in this type of business, every accomplice is at a benefit of pooling resources into the achievement of the enterprise. A Partnership has an upper hand in pooling assets to acquire capital. This could be valuable when securing credit, or doubling seed cash.

- 6. References Lorette, K. (n.d.). Sources of finance for partnerships. Demand Media. Retrieved from http://smallbusiness.chron.com/sources- finance-partnership-3663.html Sba.gov (n.d.). Choose your business structure: Partnership. Retrieved from https://www.sba.gov/content/partnership 2