1. MAY 2011

Market Matters

APRIL HIGHLIGHTS

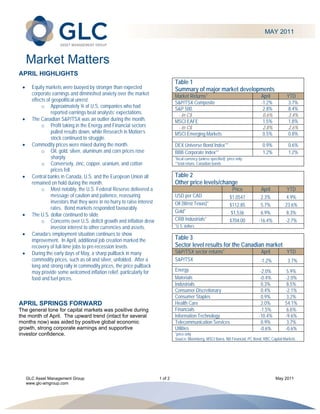

Table 1

Equity markets were buoyed by stronger than expected Summary of major market developments

corporate earnings and diminished anxiety over the market Market Returns* April YTD

effects of geopolitical unrest. S&P/TSX Composite -1.2% 3.7%

o Approximately ¾ of U.S. companies who had S&P 500 2.8% 8.4%

reported earnings beat analysts’ expectations. - in C$ 0.6% 3.4%

The Canadian S&P/TSX was an outlier during the month. MSCI EAFE 1.5% 1.8%

o Profit taking in the Energy and Financial sectors - in C$ 2.8% 2.6%

pulled results down, while Research in Motion’s MSCI Emerging Markets 0.5% 0.8%

stock continued to struggle.

Commodity prices were mixed during the month. DEX Universe Bond Index** 0.9% 0.6%

o Oil, gold, silver, aluminum and corn prices rose BBB Corporate Index** 1.2% 1.2%

sharply. *local currency (unless specified); price only

o Conversely, zinc, copper, uranium, and cotton **total return, Canadian bonds

prices fell.

Central banks in Canada, U.S. and the European Union all Table 2

remained on hold during the month. Other price levels/change

o Most notably, the U.S. Federal Reserve delivered a Price April YTD

message of caution and patience, reassuring USD per CAD $1.0547 2.3% 4.9%

investors that they were in no hurry to raise interest Oil (West Texas)* $112.85 5.7% 23.6%

rates. Bond markets responded favourably.

Gold* $1,536 6.9% 8.3%

The U.S. dollar continued to slide.

o Concerns over U.S. deficit growth and inflation drew CRB Industrials* $704.00 -16.4% -2.7%

investor interest to other currencies and assets. *U.S. dollars

Canada’s employment situation continues to show

improvement. In April, additional job creation marked the Table 3

recovery of full-time jobs to pre-recession levels. Sector level results for the Canadian market

During the early days of May, a sharp pullback in many S&P/TSX sector returns* April YTD

commodity prices, such as oil and silver, unfolded. After a S&P/TSX -1.2% 3.7%

long and strong rally in commodity prices, the price pullback

may provide some welcomed inflation relief, particularly for Energy -2.0% 5.9%

food and fuel prices. Materials -0.4% -2.0%

Industrials 0.3% 8.5%

Consumer Discretionary 0.4% -2.1%

Consumer Staples 0.9% 3.2%

APRIL SPRINGS FORWARD Health Care 2.0% 54.1%

The general tone for capital markets was positive during Financials -1.5% 6.6%

the month of April. The upward trend (intact for several Information Technology -10.4% -9.6%

months now) was aided by positive global economic Telecommunication Services 0.9% 3.7%

growth, strong corporate earnings and supportive Utilities -0.6% -0.6%

investor confidence. *price only

Source: Bloomberg, MSCI Barra, NB Financial, PC Bond, RBC Capital Markets

GLC Asset Management Group 1 of 2 May 2011

www.glc-amgroup.com

2.

U.S. equity markets in particular had a very strong ROAD WORK AHEAD. EXPECT DELAYS.

month in April (see Table 1). Small and mid-cap One of the surest signs of spring is the resurgence of

companies hit all-time highs, fully recovering from their construction crews and road repair across the country.

financial crisis battering, while even the tech-heavy Delays and bumpy roads quickly become commonplace.

Nasdaq Composite index reached its highest closing Even though we know delays along our route are

value in over 10 years. inevitable from time to time, we still seem to be caught

off guard. It takes a while to find our patience and avoid

The Canadian S&P/TSX was the noted exception to the disappointment by building in extra time to reach our

positive equity markets (see Table 2). Perhaps as a destination. The commodity pullback in early May

foreshadowing glimpse of what was to come in early delivered the same lesson.

May, the Energy sector declined, despite oil prices rising

almost 6% during the month. Investors took profit on Canadians are more sensitive to significant moves in

assumptions that oil prices (up just shy of 25% year-to- commodity prices because the impact can affect our

date) would not persist. Instead investors factored in economy and markets in several ways. Not only are

more moderate expectations for oil prices and sold off many of our businesses and exports driven by our

Canadian energy companies. Similarly, after a strong fortunate supply of natural resources in Canada, but our

run, the stock price of Canadian financial companies currency and stock market results are positively

took a breather and declined modestly in the month. correlated with commodity prices as well. The slide in

The most significant sector decline came in the commodity prices will cause an initial shock to the

Information Technology sector. As is usually the case strength of the Canadian dollar and to our equity

with this sector in Canada, it was the stock-specific story markets, but there may also be some positive outcomes.

of Research in Motion (RIM) that defined the sector For example, a moderation in commodity prices will be a

performance. RIM’s market share has been declining welcome relief for those concerned about inflation and

over the past year due to increased competition from the rising cost of fuel and food around the world.

Apple's iPhone and various Android smartphones. This Likewise, market setbacks often give investors a

led RIM executives to warn that the company’s first breather - time to reassess their assumptions and

quarter earnings would be lower than initially anticipated. outlooks for companies – and effectively lay the ground

As well, a "less-than-favourable debut" of the company's work for the next leg of a market rally.

PlayBook tablet on April 19 sealed the negative

sentiment for the company. With commodity prices having risen sharply over the

past several months, a pullback and moderation of

CAREFULLY CONSIDERED prices (such as we’ve seen in early May) was not

Bond markets, which have been weaker overall this completely unexpected. However, when faced with the

year, managed a relatively strong result in April. Fixed headlines, anxiety and frustration rise. Consider the

income investors took comfort in Bank of Canada advice written in bold in advance of road construction:

Governor Carney’s comments that he remains cautious “expect delays”. Find your patience and avoid future

about the timing of further tightening monetary policy. disappointments by planning ahead for the inevitable

By doing so, he pushed back the timing expectations for setback from time to time. It might just help you reach

the next interest rate hike, previously anticipated for your investment destination safely and comfortably.

early summer. Similarly dovish comments made by U.S.

Federal Reserve Chairman Bernanke also contributed to

an improved near-term outlook for bond investors.

Copyright GLC, You may not reproduce, distribute, or otherwise use any of this article without the prior written consent of GLC Asset Management Group

The views expressed in this commentary are those of GLC Asset Management Group Ltd. (GLC) as at the date of publication and are subject to change

without notice. This commentary is presented only as a general source of information and is not intended as a solicitation to buy or sell specific

investments, nor is it intended to provide tax or legal advice. Prospective investors should review the offering documents relating to any investment

carefully before making an investment decision and should ask their advisor for advice based on their specific circumstances.

GLC Asset Management Group 2 of 2 May 2011

www.glc-amgroup.com