Esterhuyse LT transparency

•Download as PPT, PDF•

0 likes•27 views

Lightning Talk presented at the 'Transparency and Society - Between Promise and Peril' Herrenhausen Conference in Berlin from 12-14 June 2018.

Recommended

Recommended

More Related Content

Similar to Esterhuyse LT transparency

Similar to Esterhuyse LT transparency (20)

Recently uploaded

Recently uploaded (20)

Esterhuyse LT transparency

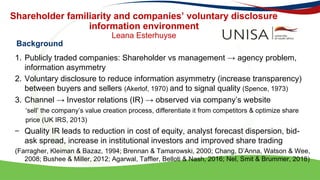

- 1. Shareholder familiarity and companies’ voluntary disclosure information environment Leana Esterhuyse 1. Publicly traded companies: Shareholder vs management → agency problem, information asymmetry 2. Voluntary disclosure to reduce information asymmetry (increase transparency) between buyers and sellers (Akerlof, 1970) and to signal quality (Spence, 1973) 3. Channel → Investor relations (IR) → observed via company’s website ‘sell’ the company’s value creation process, differentiate it from competitors & optimize share price (UK IRS, 2013) – Quality IR leads to reduction in cost of equity, analyst forecast dispersion, bid- ask spread, increase in institutional investors and improved share trading (Farragher, Kleiman & Bazaz, 1994; Brennan & Tamarowski, 2000; Chang, D’Anna, Watson & Wee, 2008; Bushee & Miller, 2012; Agarwal, Taffler, Belloti & Nash, 2016; Nel, Smit & Brummer, 2018) Background

- 2. Research Problem Given the benefits of an IR programme, why is there such a divergence in online IR practices amongst Johannesburg Stock Exchange-listed companies? JSE has low liquidity and high block holdings Investors’ investment horizon influences management’s behaviour. Predominantly short-term investors are associated with: – Lack of investment in infrastructure and R&D (Porter, 1992; Bushee, 1998; Souder et al., 2016) – Increased return volatility (Bushee & Noe, 2000) – 3% lower control premiums accepted by target co’s in M&As (Gaspar et al, 2005) – Shortened strategic planning horizon, pressure to meet targets (Bailey et al., 2014) Long-horizon investors have long-term relationship and therefore are FAMILIARFAMILIAR with: – Quality of management (ability to deliver long-term sustainable returns) – Risks and rewards of investee company → Lower demand for voluntary information disclosures → catering Hypothesis: higher (lower) proportions of long-horizon investors are associated with lower (higher) quality voluntary disclosures/transparency Literature review and hypothesis

- 3. Methodology Test hypothesis with OLS regression → DSt = α + β1STABt-1 + CONTROLS + ε Proxies: – Voluntary disclosure information environment – Online Investor Relations Disclosure Scores (DS) – Shareholder familiarity – shareholder stability (average of 9 years’ inverse share turnover); lagged Data sources: – Primary data – hand collected → DS; 205 JSE companies (main board), various industries and sizes, content analyses of websites: July – mid-Sept 2012 – Secondary data – Industry and company data – from IRESS database • Average DS 39.8%; std dev 13.5% • ↑ stability (familiarity); ↓DS; p < .000; Accept hypothesis Voluntary information demand (transparency) is bounded by investors’ investment horizon; developing market; Sub-Saharan country → Determine shareholders’ investment horizon BEFORE spending on increasing IR Results Contribution