Arizona Charitable Contribution Credits

•

1 like•160 views

Contribution credits for working poor, foster care, private school tuition and public school fees.

Recommended

Recommended

More Related Content

What's hot

What's hot (13)

Viewers also liked

Viewers also liked (20)

Similar to Arizona Charitable Contribution Credits

Similar to Arizona Charitable Contribution Credits (20)

More from CBIZ & MHM Phoenix

More from CBIZ & MHM Phoenix (20)

Recently uploaded

Recently uploaded (20)

Arizona Charitable Contribution Credits

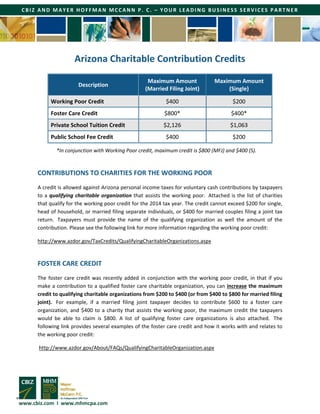

- 1. www.cbiz.com I www.mhmcpa.com CBIZ AND MAYER HOFFMAN MCCANN P. C. – YOUR LEADING BUSINESS SERVICES PARTNER Arizona Charitable Contribution Credits *In conjunction with Working Poor credit, maximum credit is $800 (MFJ) and $400 (S). CONTRIBUTIONS TO CHARITIES FOR THE WORKING POOR A credit is allowed against Arizona personal income taxes for voluntary cash contributions by taxpayers to a qualifying charitable organization that assists the working poor. Attached is the list of charities that qualify for the working poor credit for the 2014 tax year. The credit cannot exceed $200 for single, head of household, or married filing separate individuals, or $400 for married couples filing a joint tax return. Taxpayers must provide the name of the qualifying organization as well the amount of the contribution. Please see the following link for more information regarding the working poor credit: http://www.azdor.gov/TaxCredits/QualifyingCharitableOrganizations.aspx FOSTER CARE CREDIT The foster care credit was recently added in conjunction with the working poor credit, in that if you make a contribution to a qualified foster care charitable organization, you can increase the maximum credit to qualifying charitable organizations from $200 to $400 (or from $400 to $800 for married filing joint). For example, if a married filing joint taxpayer decides to contribute $600 to a foster care organization, and $400 to a charity that assists the working poor, the maximum credit the taxpayers would be able to claim is $800. A list of qualifying foster care organizations is also attached. The following link provides several examples of the foster care credit and how it works with and relates to the working poor credit: http://www.azdor.gov/About/FAQs/QualifyingCharitableOrganization.aspx Description Maximum Amount (Married Filing Joint) Maximum Amount (Single) Working Poor Credit $400 $200 Foster Care Credit $800* $400* Private School Tuition Credit $2,126 $1,063 Public School Fee Credit $400 $200

- 2. www.cbiz.com I www.mhmcpa.com CBIZ AND MAYER HOFFMAN MCCANN P. C. – YOUR LEADING BUSINESS SERVICES PARTNER PRIVATE SCHOOL TUITION CREDIT A credit is allowed for cash contributions by a taxpayer to a school tuition organization up to the amount of $528 ($1,056 for married filing joint). An additional credit is allowed for contributions to a school tuition organization of up to $535 ($1,070 for married filing joint), thus allowing for a maximum credit of $1,063 ($2,126 for MFJ). Attached is a list of school tuition organizations that qualify for this credit. In addition, a contribution made after January 1st, but before April 15th may be applied to either the current or the preceding taxable year. For example, if a taxpayer contributes $1,000 to a private tuition organization on March 4, 2015, then the contribution may be applied to either the 2014 or the 2015 tax year. Keep in mind that the credit is not allowed if the taxpayer designates the donation for the direct benefit of any dependent of the taxpayer, and the credit is not allowed if the taxpayer designates a student beneficiary as a condition of the taxpayer’s contribution. For more information regarding this credit, click the following link: http://www.azdor.gov/TaxCredits/SchoolTaxCreditsforIndividuals.aspx CREDIT FOR PUBLIC SCHOOL FEE CONTRIBUTIONS A credit is allowed for the fees or cash contributions made by a taxpayer to support public school extra- curricular activities, up to $200 for a single individual or $400 for married couples filing a joint return. The credit applies to extra-curricular activities or character education programs. Extra- curricular activities are school-sponsored activities that require enrolled students to pay a fee in order to participate. Character education programs must include (1) instruction in the definition and application of prescribed character traits, (2) activities and discussions to reinforce character traits, and (3) presentations by teachers that demonstrate character traits. Nongovernmental schools, pre-schools, community colleges, and universities do not qualify for the credit. To determine if an extracurricular activity is tax credit eligible and other guidelines click here.