Recommended

More Related Content

Similar to Basic accounting credit debit

Similar to Basic accounting credit debit (20)

Recently uploaded

Recently uploaded (20)

Basic accounting credit debit

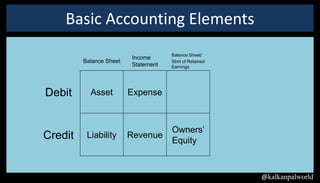

- 1. Basic Accounting Elements Balance Sheet/ Income Balance Sheet Stmt of Retained Statement Earnings Debit Asset Expense Owners’ Credit Liability Revenue Equity @kalkanpalworld

- 2. Example • You purchase $80 worth of inventory for cash Debit Credit • Inventory . . . . . . . . . . . . . . . 80 • Cash . . . . . . . . . . . . . . ….. ………………….80 @kalkanpalworld

- 3. Example • The company borrowed $200 from a bank • Increase in Assets (Cash) by $200 • Increase in Liabilities (Borrowings) by $200 • Journal Entry Debit Credit • Cash 200 • Borrowings 200 @kalkanpalworld

- 4. Example • Company paid $400 salary • Increase in Expenses (Salaries Expense) by $400 • Decrease in Assets (Cash) by $400 • Journal Entry Debit Credit • Salaries Expense 400 • Cash 400 •