BP And Volatility

•

0 likes•178 views

A few slides illustrating the changes in volatility term structure since the April high of 1219 on the S&P and since a week before the spill in the Gulf.

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

BP And Volatility

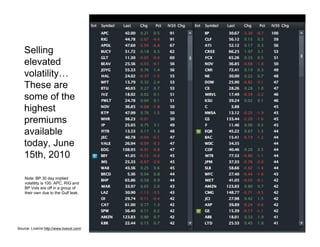

- 1. Selling elevated volatility… These are some of the highest premiums available today, June 15th, 2010 Note: BP 30 day implied volatility is 100. APC, RIG and BP Vols are off in a group of their own due to the Gulf leak. Source: LiveVol http://www.livevol.com/

- 2. BP “a week before the leak” Front month of May (and July) show elevated put skew due to dividends, but otherwise the surface from front month to the Jan’12 leaps are flat. 30 Day Implied volatility is ~18, and while puts are trading “rich” to calls, the curve or volatility surface is fairly flat, with all contracts below 50 volatility... Source: LiveVol http://www.livevol.com/

- 3. BP “this week, still a leak” and a week of June expiration Front month of June only had five trading days, so everything was priced to move. Skew across Puts to calls is very obvious, but front to back, the surface points to more noise in the near term. Now, 30 Day Implied vol is ~100, and there is massive skew past July expiration. Note - the best calls to write are June and July relative to buying October and the leap calls. Source: LiveVol http://www.livevol.com/

- 4. VIX “Skew” across time - the 4th and 5th dimensions The volatility surface is rotated to better show the differences across time. Despite a spot VIX in the mid teens, there was a contango to the low 20s from May into all months. In April at the most recent peak of the S&P 500, December is expensive relative to 30 day levels suggesting more volatility ahead. Dec’12 skew is fairly flat… Source: LiveVol http://www.livevol.com/

- 5. VIX skew today, June 15th - More volatile times A large put spread traded the week of expiration, so some market participants seem to expect volatility to fall into the Summer, but stay above the teens seen in April. Now, while very elevated, the drop from July to December suggests front month volatility will come down. Dec’12 skew steepened significantly but should flatten with a market rally. Source: LiveVol http://www.livevol.com/