IFRS 2010 conceptual framework

•

0 likes•25 views

IFRS 2010 Brief - All 7 Chapters

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Similar to IFRS 2010 conceptual framework

Similar to IFRS 2010 conceptual framework (20)

More from Debre Tabor University Ethiopia

More from Debre Tabor University Ethiopia (20)

Recently uploaded

Recently uploaded (20)

IFRS 2010 conceptual framework

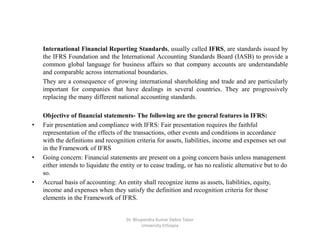

- 1. International Financial Reporting Standards, usually called IFRS, are standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB) to provide a common global language for business affairs so that company accounts are understandable and comparable across international boundaries. They are a consequence of growing international shareholding and trade and are particularly important for companies that have dealings in several countries. They are progressively replacing the many different national accounting standards. Objective of financial statements- The following are the general features in IFRS: • Fair presentation and compliance with IFRS: Fair presentation requires the faithful representation of the effects of the transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework of IFRS • Going concern: Financial statements are present on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so. • Accrual basis of accounting: An entity shall recognize items as assets, liabilities, equity, income and expenses when they satisfy the definition and recognition criteria for those elements in the Framework of IFRS. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 2. • Materiality and aggregation: Every material class of similar items has to be presented separately. Items that are of a dissimilar nature or function shall be presented separately unless they are immaterial. • Offsetting: Offsetting is generally forbidden in IFRS. However certain standards require offsetting when specific conditions are satisfied (such as in case of the accounting for defined benefit liabilities in IAS 19 and the net presentation of deferred tax liabilities and deferred tax assets in IAS 12. • Frequency of reporting: IFRS requires that at least annually a complete set of financial statements is presented. However listed companies generally also publish interim financial statements (for which the accounting is fully IFRS compliant)for which the presentation is in accordance with IAS 34 Interim Financing Reporting. • Comparative information: IFRS requires entities to present comparative information in respect of the preceding period for all amounts reported in the current period's financial statements. In addition comparative information shall also be provided for narrative and descriptive information if it is relevant to understanding the current period's financial statements. The standard IAS 1 also requires an additional statement of financial position (also called a third balance sheet) when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements. This for example occurred with the adoption of the revised standard IAS 19 (as of 1 January 2013) or when the new consolidation standards IFRS 10-11-12 were adopted (as of 1 January 2013 or 2014 for companies in the European Union). Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 3. • Consistency of presentation: IFRS requires that the presentation and classification of items in the financial statements is retained from one period to the next unless: 1- it is apparent, following a significant change in the nature of the entity's operations or a review of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in IAS 8; or 2- an IFRS standard requires a change Adoption • IFRS are used in many parts of the world, including the South Korea, European Union , India, Hong Kong, Australia , Malaysia, Pakistan, GCC countries, Russia, Chile, Philippines, South Africa, Singapore, and Turkey but not in the United States. • It is generally expected that IFRS adoption worldwide will be beneficial to investors and other users of financial statements, by reducing the costs of comparing alternative investments and increasing the quality of information. Companies are also expected to benefit, as investors will be more willing to provide financing. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 4. • Ghana • Ghana transitioned from the Ghana Accounting Standards (GAS) to adopt the IFRS on January 1, 2007.[ As of 2008 and beyond, a legislative injunction has been imposed on the Bank of Ghana to prepare financial statements in accordance with IFRS; thereby making it mandatory for all public entities in the country. • South Africa • All companies listed on the Johannesburg Stock Exchange have been required to comply with the requirements of International Financial Reporting Standards since 1 January 2005. • The IFRS for SMEs may be applied by 'limited interest companies', as defined in the South African Corporate Laws Amendment Act of 2006 (that is, they are not 'widely held'), if they do not have public accountability (that is, not listed and not a financial institution). Alternatively, the company may choose to apply full South African Statements of GAAP or IFRS. • South African Statements of GAAP are entirely consistent with IFRS, although there may be a delay between issuance of an IFRS and the equivalent SA Statement of GAAP (can affect voluntary early adoption). • South African Statements of GAAP were withdrawn by the Financial Reporting Standards Council (FASC) per the South African Institute of Chartered Accountants (SAICA) for financial years commencing on or after 1 December 2012. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 5. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 6. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 7. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 8. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 9. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 10. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 11. Why Accrual accounting Important? Capital Market to judge productivity .. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 12. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 13. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 14. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 15. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 16. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 17. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 18. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 19. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 20. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 21. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 22. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 23. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 24. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 25. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 26. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 27. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 28. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 29. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 30. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 31. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 32. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 33. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 34. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 35. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 36. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 37. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 38. Dr. Bhupendra Kumar Debre Tabor University Ethiopia

- 39. Dr. Bhupendra Kumar Debre Tabor University Ethiopia