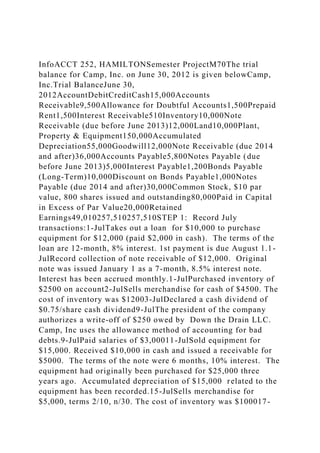

InfoACCT 252, HAMILTONSemester ProjectM70The trial balance for Camp, Inc. on June 30, 2012 is given belowCamp, Inc.Trial BalanceJune 30, 2012AccountDebitCreditCash15,000Accounts Receivable9,500Allowance for Doubtful Accounts1,500Prepaid Rent1,500Interest Receivable510Inventory10,000Note Receivable (due before June 2013)12,000Land10,000Plant, Property & Equipment150,000Accumulated Depreciation55,000Goodwill12,000Note Receivable (due 2014 and after)36,000Accounts Payable5,800Notes Payable (due before June 2013)5,000Interest Payable1,200Bonds Payable (Long-Term)10,000Discount on Bonds Payable1,000Notes Payable (due 2014 and after)30,000Common Stock, $10 par value, 800 shares issued and outstanding80,000Paid in Capital in Excess of Par Value20,000Retained Earnings49,010257,510257,510STEP 1: Record July transactions:1-JulTakes out a loan for $10,000 to purchase equipment for $12,000 (paid $2,000 in cash). The terms of the loan are 12-month, 8% interest. 1st payment is due August 1.1-JulRecord collection of note receivable of $12,000. Original note was issued January 1 as a 7-month, 8.5% interest note. Interest has been accrued monthly.1-JulPurchased inventory of $2500 on account2-JulSells merchandise for cash of $4500. The cost of inventory was $12003-JulDeclared a cash dividend of $0.75/share cash dividend9-JulThe president of the company authorizes a write-off of $250 owed by Down the Drain LLC. Camp, Inc uses the allowance method of accounting for bad debts.9-JulPaid salaries of $3,00011-JulSold equipment for $15,000. Received $10,000 in cash and issued a receivable for $5000. The terms of the note were 6 months, 10% interest. The equipment had originally been purchased for $25,000 three years ago. Accumulated depreciation of $15,000 related to the equipment has been recorded.15-JulSells merchandise for $5,000, terms 2/10, n/30. The cost of inventory was $100017-JulPaid for liability insurance premiums for June 2012 of $30023-Jul$250 worth of merchandise sold on July 15 is returned. The original cost of inventory was $100.27-JulMade payment of $800 to accounts payable28-JulPaid cash for additional land of $1600028-JulSells merchandise for cash of $3600. The cost of inventory was $80029-JulReceives balance due for merchandise sold on July 1530-JulPurchased inventory of $500 on account31-JulPaid cash dividend declared on July 331-JulPaid one year flood insurance of $360031-JulPays in full the outstanding payable for inventory purchased on July 131-JulReceived interest from checking account of $10031-JulPaid bank fees of $30Step 2: The following adjusting entries need to be recorded at the end of the month1Calculate & record monthly depreciation on following fixed assets using straight line depreciationBuilding - Depreciable Cost $75,000; Salvage Value = $3,000; Useful Life = 20 YearsVehicles - Depreciable Cost $30,000; Salvage Value = 0; Life = 5 yearsEquipment - Depreciable Cost $10,000; Salvage Value = $400; annual rate of depreciat.

InfoACCT 252, HAMILTONSemester ProjectM70The trial balance for Cam.docx

1. InfoACCT 252, HAMILTONSemester ProjectM70The trial

balance for Camp, Inc. on June 30, 2012 is given belowCamp,

Inc.Trial BalanceJune 30,

2012AccountDebitCreditCash15,000Accounts

Receivable9,500Allowance for Doubtful Accounts1,500Prepaid

Rent1,500Interest Receivable510Inventory10,000Note

Receivable (due before June 2013)12,000Land10,000Plant,

Property & Equipment150,000Accumulated

Depreciation55,000Goodwill12,000Note Receivable (due 2014

and after)36,000Accounts Payable5,800Notes Payable (due

before June 2013)5,000Interest Payable1,200Bonds Payable

(Long-Term)10,000Discount on Bonds Payable1,000Notes

Payable (due 2014 and after)30,000Common Stock, $10 par

value, 800 shares issued and outstanding80,000Paid in Capital

in Excess of Par Value20,000Retained

Earnings49,010257,510257,510STEP 1: Record July

transactions:1-JulTakes out a loan for $10,000 to purchase

equipment for $12,000 (paid $2,000 in cash). The terms of the

loan are 12-month, 8% interest. 1st payment is due August 1.1-

JulRecord collection of note receivable of $12,000. Original

note was issued January 1 as a 7-month, 8.5% interest note.

Interest has been accrued monthly.1-JulPurchased inventory of

$2500 on account2-JulSells merchandise for cash of $4500. The

cost of inventory was $12003-JulDeclared a cash dividend of

$0.75/share cash dividend9-JulThe president of the company

authorizes a write-off of $250 owed by Down the Drain LLC.

Camp, Inc uses the allowance method of accounting for bad

debts.9-JulPaid salaries of $3,00011-JulSold equipment for

$15,000. Received $10,000 in cash and issued a receivable for

$5000. The terms of the note were 6 months, 10% interest. The

equipment had originally been purchased for $25,000 three

years ago. Accumulated depreciation of $15,000 related to the

equipment has been recorded.15-JulSells merchandise for

$5,000, terms 2/10, n/30. The cost of inventory was $100017-

2. JulPaid for liability insurance premiums for June 2012 of

$30023-Jul$250 worth of merchandise sold on July 15 is

returned. The original cost of inventory was $100.27-JulMade

payment of $800 to accounts payable28-JulPaid cash for

additional land of $1600028-JulSells merchandise for cash of

$3600. The cost of inventory was $80029-JulReceives balance

due for merchandise sold on July 1530-JulPurchased inventory

of $500 on account31-JulPaid cash dividend declared on July

331-JulPaid one year flood insurance of $360031-JulPays in full

the outstanding payable for inventory purchased on July 131-

JulReceived interest from checking account of $10031-JulPaid

bank fees of $30Step 2: The following adjusting entries need to

be recorded at the end of the month1Calculate & record monthly

depreciation on following fixed assets using straight line

depreciationBuilding - Depreciable Cost $75,000; Salvage

Value = $3,000; Useful Life = 20 YearsVehicles - Depreciable

Cost $30,000; Salvage Value = 0; Life = 5 yearsEquipment -

Depreciable Cost $10,000; Salvage Value = $400; annual rate of

depreciation 25%2Accrued interest on long-term note receivable

is $5003On January 1, $9,000 rent for equipment was prepaid

for 6 months. Record the adjustment, if any, necessary for

June4It is estimated that $1000 of accounts receivable will be

uncollectible5Salaries incurred by the month end but not yet

paid is $23006Compute and record the accrued interest on note

payable taken out on July 1.7The president of the company

thinks Goodwill is understated and wants to write it up to

$20,000Step 3: Complet T-Accounts. This will NOT be graded,

but will prove to be extremely beneficial to you in completing

the rest of the assignment.Step 4: Prepare a Trial Balance after

all JE's and AJE's have been postedStep 5: Prepare a balance

sheet, income statement, and statement of stockholders equity

for July

STEP 1 JEDateAccountDRCR1-

JulEquipment12,000Cash2,000Notes Payable10,000(purchased

equipment for cash and 12-month, 8% note payable)1-

JulCash12,510Notes Recievable12,000Interest Revenue5101-

3. JulInventory2,500Accounts Payable2,5002-JulCash4,500Sales

Revenue4,500Cost of Goods Sold1,200Inventory1,2003-JulCash

Dividends600Dividends Payable600(record declaration of cash

dividend)9-JulAllowance for Doubtful Accounts250Accounts

Recievable- Down the Drain LLC2509-JulSalaries

Expense3,000Cash3,00011-JulCash10,000Notes

Recievable5,000Accumlated Depreciation-

Equpiment15,000Equipment25,000Gain on Disposal of Plant

Assets5,00015-JulAccounts Recievable5,000Sales

Revenue5,000(On Terms of 2/10, n/30)Cost of Goods

sold1,000Inventory1,00017-JulInsurance

Expense300Cash300(Paid insurance premium)23-JulSales

Returns and Allowances250Accounts

Recievable250Inventory100Cost of goods sold10027-

JulAccounts Payable800Cash80028-

JulLand16,000Cash16,00028-JulCash3,600Sales

Revenue3,600Cost if Goods sold800Inventory80029-

JulCash4,750Accounts Payable4,750(Collection of balance due

from sale on July-15)30-JulInventory500Accounts

Payable500(purchase of inventory)31-JulDividends

Payable600Cash600(Payment of dividend)31-JulPrepaid

Insurance3,600Cash3,600(paid 1-year flood insuance)31-

JulAccount Payable10,067Cash10,067(paid accounts payable

July-1 in full with 1month interest)31-JulInterest

Recievable100Accounts Payable100(intrest received from

Checking Account)31-JulCash30Service Revenue30(Record the

bank fees)

Step 2 AJEDateAccountDRCR31-JulDepreciation

Expense300Accumulated Depreciation-Building300(to record

monthly depreciation)31-JulDepreciation

Expense500Accumulated Depreciation-Vehicles500(monthly

depreciation)31-JulDepreciation Expense200Accumulated

Depreciation-Equipment200(monthly depreciation)31-JulIntrest

Receviable500Interest Revenue500(record of accured intrest of

long-term notes recievable)31-JulBad Debits

Expense1,000Allowance for Doubtful Accounts1,000(to record

4. the estimated accounts recievable uncollected)31-JulSalary

Expense2,300Salaries Payable2,300(to record Accured

Salaries)31-JulInterest Expense67Intrest Payable67(to record

monthly intrest on note payable)31-JulGood will cannot be

changed unless there is an exchange transaction that involves

the purchase of an entire business. Goodwill is the excess of

cost over the fair value of the net assets aquired.

Step 3 T-AccountsThis is NOT required, but is recommended

and will be helpful to complete the assignment.I have started a

couple of accounts, you can add accounts as you feel is

necessaryCashAccounts RecievableAllowance for Doubtful

AccountsLandSalary expenseAccounts PayableSales Returns &

Allowances12,5102,0002502501,00016,0003000800250025010,

0003,0005,000250230010,0675004,500300Debit 16,000Debit

5300100+47503,600800debit 3,017debit

2504,75016,00030600EquipmentInsurance expenseAccumulated

DepreciationPrepaid

Insurance3,60012,00025,00030015,000300360010,067debit

4,500credit 750500credit 977200Intrest RevenueGain on

Disposal of AssetsCredit 13,000debit 300debit 14,000Debit

36005105000Interest Recievable500Notes RecievableNotes

PayableDepreciation ExpenseBad Debits ExpenseService

Expense500credit 1010Credit

500050001200010,000300100030100500debit 600credit

7,000credit 10,000200debit 1000Debit 30Sales RevenueCash

DividendsInventorydebit 1000450060025001200Cost of Goods

SoldDividends PayableSalary PayableInterest ExpenseInterest

Payable500010010001200100600600230067673600Debit

6005008001000Credit 13,100Debit 100800Debit 29000Credit

2300debit 67credit 67

Step 4 TBTrial BalanceDr.Cr.Cash$977Accounts

Recievable4,500Bad Debits Expense1,000Interest

Recievable600Inventory100Notes Recievable7000Prepaid

Insurance3,600Land16,000Equipment13,000Accumulated

Depreciation-Equipment, building, vehicles14,000Accounts

Payable3,017Notes Payable10,000Interest Payable67Salaries

5. Payable-Accrued2,300Salaries Expense5,300Sales Returns &

Allowances250Retained Earnings0Allowance for Doubtful

Accounts750Interest Revenue1010Sales Revenue13,100Gain on

Disposal of Asset5,000Cost of Goods Sold2,900Insurance

Expense300Depreciation Expense1,000Service Expense30Cash

Dividends600Interest Expense67Dividends053,23453,234

Step 5 Balance Sheet

Step 5 Income Statement

Step 5 Statement of SE

The Case For, or Against, New Orleans

Sometimes one’s choices may involve catastrophic decisions

and bear great risk and yet there can be no clear answer. For

example, if a person gets a divorce, shutters a plant, sells a

losing investment, or closes their business, will he or she be

better off? The following case incorporates nearly all of the

material you have covered this far and presents an example of

one such choice where nearly all of the alternatives have a

significant downside risk.

Review the following information from the article “A Cost-

Benefit Analysis of the New Orleans Flood Protection System”

by Stéphane Hallegatte (2005):

· Hallegatte, an environmentalist, assigns a probability (p) of a

Katrina-like hurricane of 1/130 in his cost-benefit analysis for

flood protection. However, the levees that protect New Orleans

also put other regions at greater risk. You may assume the

frequency of other floods is greater than Katrina-like events

(Vastag & Rein, 2011).

· The new levees that were built in response to Katrina cost

approximately fourteen billion dollars (in 2010). This is in

addition to the direct costs of Katrina (eighty-one billion dollars

in 2005).

· 50 percent of New Orleans is at or below sea level.

· A 100-year event means that there is a 63 percent chance that

such an event will occur within a 100-year period.

· The following are the interested (anchored and/or biased)

6. constituencies:

· Residents of New Orleans—both those that can move and

those who cannot move

· Residents of the surrounding floodplains at risk from New

Orleans levees

· The Mayor of New Orleans

· The federal government—specifically taxpayers and the

Federal Emergency Management Agency (FEMA)

Assume that the availability heuristics makes people more risk

averse (populations drop, at least in the short term). Consider

how this would affect the local economy.

You are an analyst at FEMA and are in charge of developing a

recommendation for both the state and the local governments on

whether or not to redevelop New Orleans.

Write a report with your recommendation. Address the

following in your report:

Part A

· Analyze the economics of New Orleans in light of the above

parameters and develop your own Cost-Benefit Analysis (CBA)

for rebuilding.

· Evaluate the value of the CBA for each constituency and

integrate these estimates into a scenario model and/or decision

tree. Analyze the results.

· Clearly each of these constituencies may both overlap and be

prey to a variety of group dynamics internally. For one of these

options, discuss the decision pitfalls to which they may be

susceptible and make a recommendation on how to alleviate

these pressures.

· Starting with your CBA, estimate the relevant expected utility

for the interested constituencies.

Note: You need not have absolute amounts but your relevant

utilities should be proportional to one another. Hint: If you

assume that your total CBA for New Orleans is fixed for each

constituency (do not forget the overlaps), then each

constituency will have a piece of the utility pie.

Part B

7. · Make a case for or against rebuilding the city of New Orleans.

This should be an executive summary; be concise and brief.

Include exhibits.

· Whether you are for or against, discuss how social heuristics

could be used to your advantage, both ethically and unethically,

in making your case. You may choose to fill the role of one of

the constituents, if you prefer.

Write an 8–10-page report in Word format. Apply APA

standards to citation of sources. Use proper spelling and

grammar throughout, and keep the text legible and balanced

with visuals.

Hallegatte, S. (2006). A cost-benefit analysis of the New

Orleans flood protection system. Center for Environmental

Sciences and Policy. Stanford University. Retrieved from

http://hal.cirad.fr/docs/00/16/46/28/PDF/Hallegatte_NewOrle

ans_CBA9.pdf

Vastag, B., & Rein, L. (2011, May 11). In Louisiana, a choice

between two floods. TheWashington Post. Retrieved from

http://www.washingtonpost.com/national/in-louisiana-a-

choice-between-two- floods/2011/05/11/AFrjFotG_story.html

LASA 2—The Case For, or Against, New Orleans Grading

Rubric

NOTE: If a component is absent, student receives a zero for that

component.

9. points

e.g.

(80% / 100) x 12 =

9.6

Analyze the

economics of New

Orleans in light of

the given

parameters and

develop a Cost-

Benefit Analysis

(CBA) for

rebuilding.

Course Objectives

(CO) 3 & 4

Analysis of New

Orleans economics is

inaccurate or

incomplete. It includes

an estimated cash

flow/CBA, but it is

unreasonable. A few

outcomes and possible

scenarios are

presented but many are

not likely. Too few

constituencies and

interdependencies are

represented.

10. CBA for rebuilding is

unreasonable in

regards to scope,

resources, and/or

objectives. CBA

provides resources

needed but how they

will achieve objectives

is unclear. Research

Analysis of New

Orleans’ economics is

somewhat accurate or

somewhat incomplete. It

includes an estimated

cash flow/CBA but is

somewhat

unreasonable. A variety

of outcomes and several

possible scenarios are

presented but some may

not be likely. Most

constituencies and their

interdependencies are

represented.

CBA for rebuilding is

somewhat unreasonable

in regards to scope,

resources, or objectives.

CBA provides resources

11. needed to achieve

objectives but is not

specific in detail.

Analysis of New

Orleans’ economics is

accurate and complete.

It includes a reasonably

estimated cash

flow/CBA with a variety

of likely outcomes and

several possible

scenarios. All

constituencies and their

interdependencies are

represented.

CBA for rebuilding is

reasonable in regards to

scope, resources, and

objectives. CBA

provides specific details

and resources needed to

achieve objectives.

Research and evidence

from the case study are

used to support ideas.

Analysis of New

Orleans’ economics

is insightful and

thorough. It includes

a soundly estimated

cash flow/CBA with

14. CO 1, 4, & 5

Evaluation presents

benefits of the CBA for

the constituency, but is

either inaccurate or too

vague. Some

constituencies are

described but some are

missing. Most are

appropriate to the

situation.

Scenario model and/or

decision tree is unclear

or does not

appropriately integrate

the estimates.

Integration of

constituencies is

addressed but is

inaccurate. Examples

of how decisions are

conditional upon each

other are present but

are inaccurate.

Evaluation presents

benefits of the CBA for

each constituency but is

not specific. Generally,

each constituency is

described and

15. appropriate to the

situation, but either a

few constituencies are

missing or they are

under-explained.

Scenario model and/or

decision tree is

somewhat clear or does

not completely integrate

the estimates

appropriately. Integration

of constituencies is

addressed but left a bit

vague. Examples of how

the decisions are

conditional upon each

other are present, but

some conditions must be

inferred.

Evaluation presents

specific benefits of the

CBA for each

constituency, and each

constituency is clearly

described and

appropriate to the

situation.

Scenario model and/or

decision tree clearly and

16. appropriately integrates

the estimates.

Integration of

constituencies is clearly

addressed and specific

examples of how the

decisions are conditional

upon each other are

present.

Analysis of the results is

specific and provides a

scenario model and

explains interrelation of

constituencies’

decisions.

Evaluation presents

specific, acute

benefits of the CBA

for each

constituency, and

each constituency is

completely

described and

insightfully apt to the

situation.

Scenario model

and/or decision tree

completely,

concisely, and

18. explains interrelation

of constituencies’

decision in detail.

Discuss the

decision pitfalls to

which the

constituencies may

be susceptible and

make a

recommendation on

how to alleviate

those pressures.

CO 2 & 5

Decision problems to

which the

constituencies may be

susceptible are unclear

or inappropriate to the

situation.

Recommendations are

unreasonable. Any

theory or research

reference is unclear in

regards to its support.

Decision problems to

which the constituencies

may be susceptible are

19. not clearly identified or

they are somewhat

inappropriate to the

situation.

Recommendations are

somewhat reasonable

and reference theory or

research (but support

must be inferred).

Decision problems to

which the constituencies

may be susceptible are

clearly identified and

appropriate to the

situation.

Recommendations are

reasonable and

grounded in theory or

research.

Decision problems

to which the

constituencies may

be susceptible are

astutely identified

and appropriate to

the situation.

Recommendations

are thoughtful and

grounded in theory

or research.

/ 40

Starting with the

20. CBA, estimate the

relevant expected

utility for these

parties.

CO 4

Estimation of the

relevant expected utility

for these parties is

unreasonable or not

proportional to one

another. Evidence are

sporadic or does not

support ideas.

Estimation does not

reflect the CBA

proposed.

Estimation of the

relevant expected utility

for these parties is

somewhat reasonable

and somewhat

proportional to one

another. Evidence is

provided, but how it

supports the ideas is

unclear. Estimation

references the CBA

proposal, but reflection

is unclear.

Estimation of the

relevant expected utility

21. for these parties is

reasonable, proportional

to one another, and

grounded in evidence.

Estimation reflects the

CBA proposed.

Estimation of the

relevant expected

utility for these

parties is thoughtful,

proportional to one

another, and

grounded in

insightful evidence.

Estimation clearly

reflects and relates

to the CBA

proposed.

/ 40

Make a case for or

against rebuilding

the city of New

Orleans. This

should be an

executive

summary—be

concise and brief.

Include exhibits.

Executive summary

waffles between

whether or not to

rebuild New Orleans.

22. Evidence and research

is sporadic or does not

support the ideas.

Stance occasionally is

biased or

Executive summary

takes a stance on

whether to rebuild New

Orleans or not, but

stance is unclear.

Evidence and research

are provided, but how

they support the ideas is

unclear. Stance is

generally reasonable

Executive summary

clearly takes a stance on

whether to rebuild New

Orleans or not. Specific

evidence and research

are provided to support

ideas. Stance is

reasonable and

unbiased.

Executive summary

insightfully takes a

stance on whether

to rebuild New

Orleans or not.

Specific, astute

evidence and

research are

provided to support

24. Evidence and research

are sporadic or does

not support the ideas.

Ethical and unethical

advantages are

incomplete or

inaccurately identified.

Discussion of how social

heuristics can be used to

gain advantage is

somewhat unclear or

somewhat inaccurate.

Evidence and research

is provided, but how they

support the ideas is

unclear. Ethical and

unethical advantages

are identified but are

incomplete or unclear.

Discussion of how social

heuristics can be used to

gain advantage is clear,

accurate, and provides

specific examples to

support its ideas. Ethical

and unethical

advantages are

identified and discussed.

Discussion of how

social heuristics can

be used to gain

advantage is

thoughtful,

25. complete, and

provides specific

examples to support

its ideas. Ethical and

unethical

advantages are

precisely identified

and insightfully

discussed.

/ 40

Estimate what

percentage of the

class was for,

versus against,

rebuilding and

provide a

confidence interval

for the estimate.

CO 2

Estimation is inaccurate

or unsupported.

Confidence interval is

underdeveloped or

inaccurate.

Estimation is somewhat

inaccurate or not clearly

grounded in evidence

from the case study.

Confidence interval is

somewhat vague or

26. inaccurate.

Estimation is accurate

and grounded in

evidence from the case

study. Confidence

interval is detailed and

accurate.

Estimation is

insightful and

grounded in

evidence from the

case study.

Confidence interval

is precise, detailed

clear, and accurate.

/ 12

Ensure academic

writing, such as

grammar, spelling,

and attribution of

sources, is

appropriate.

Writing is unclear and

disorganized and

rereading to solidify

understanding is

frequently necessary.

Although an attempt at

ethical scholarship is

attempted, it is sloppy

or incomplete

27. throughout. Spelling,

grammar, or

punctuation errors

severely interfere with

readers’

Writing is somewhat

clear and is somewhat

organized, although

rereading to solidify

understanding is

occasionally necessary.

It demonstrates an

attempt at ethical

scholarship in accurate

representation and

attribution of sources, but

errors are occasional or

minor. Writing has good

Writing is generally clear

and in an organized

manner. It demonstrates

ethical scholarship in

accurate representation

and attribution of

sources; and generally

displays accurate

spelling, grammar, and

punctuation. Errors are

few, isolated, and do not

interfere with reader’s

comprehension.

Writing is clear,

concise, and in an