Recommended

More Related Content

Featured

Featured (20)

Tactical Allocation Factsheet

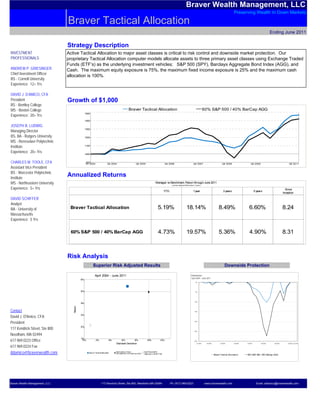

- 1. Braver Wealth Management, LLC Preserving Wealth In Down Markets Braver Tactical Allocation Ending June 2011 Strategy Description INVESTMENT Active Tactical Allocation to major asset classes is critical to risk control and downside market protection. Our PROFESSIONALS proprietary Tactical Allocation computer models allocate assets to three primary asset classes using Exchange Traded Funds (ETF’s) as the underlying investment vehicles; S&P 500 (SPY), Barclays Aggregate Bond Index (AGG), and ANDREW P. GRIESINGER Cash. The maximum equity exposure is 75%, the maximum fixed income exposure is 25% and the maximum cash Chief Investment Officer allocation is 100%. BS - Cornell University Experience: 12+ Yrs DAVID J. D’AMICO, CFA President Growth of $1,000 BS - Bentley College MS - Boston College Braver Tactical Allocation 60% S&P 500 / 40% BarCap AGG 1500 Experience: 20+ Yrs 1400 JOSEPH B. LUDWIG 1300 Managing Director BS, BA - Rutgers University 1200 MS - Rensselaer Polytechnic Institute 1100 Experience: 20+ Yrs 1000 CHARLES M. TOOLE, CFA 900 Q1 2004 Q4 2004 Q4 2005 Q4 2006 Q4 2007 Q4 2008 Q4 2009 Q2 2011 Assistant Vice President BS - Worcester Polytechnic Institute Annualized Returns MS - Northeastern University Manager vs Benchmark: Return through June 2011 (not annualiz ed if les s than 1 y ear) Experience: 5+ Yrs Since YTD 1 year 3 years 5 years Inception DAVID SCHIFFER Analyst BA - University of Braver Tactical Allocation 5.19% 18.14% 8.49% 6.60% 8.24 Massachusetts Experience: 5 Yrs 60% S&P 500 / 40% BarCap AGG 4.73% 19.57% 5.36% 4.90% 8.31 Risk Analysis Superior Risk Adjusted Results Downside Protection April 2004 - June 2011 Drawdown April 2004 - June 2011 6% 0% 5% -5% -10% 4% Return Contact -15% David J. D'Amico, CFA 3% President -20% 117 Kendrick Street, Ste 800 2% -25% Needham, MA 02494 1% 617.969.0223 Office 0% 2% 4% 6% 8% 10% 12% -30% Standard Deviation Q1 2004 Q4 2004 Q4 2005 Q4 2006 Q4 2007 Q4 2008 Q4 2009 Q4 2010 Q2 2011 617.969.0224 Fax ddamico@braverwealth.com Braver Tactical Allocation Mark et Benc hmark : 60% S&P 500 / 40% BarCap AGG Cash Equivalent: Citigroup 3-month T-bill Braver Tactical Allocation 60% S&P 500 / 40% BarCap AGG Braver Wealth Management, LLC 117 Kendrick Street, Ste 800, Needham MA 02494 Ph: (617) 969-0223 www.braverwealth.com Email: ddamico@braverwealth.com

- 2. Tactical Allocation Braver Wealth Management, LLC Page 2 Ending June 2011 Multi-Statistic Analysis Braver Wealth Management ZephyrStyleADVISOR: Braver Wealth Management Multi-Statistic April 2004 - June 2011 2.5 2 1.5 1 Braver Tactical Allocation 60% S&P 500 / 40% BarCap AGG 0.5 0 Alp ha Be ta Ex c e s s R e tur n Sha r pe In for matio n R atio Pain v s. vs . vs . R a tio vs . R atio Ma r k e t Mar k et Mar k et Mar k et Peer Review Braver Wealth Management ZephyrStyleADVISOR: Braver Wealth Management Manager vs Morningstar Moderate Allocation: Return April 2004 - June 2011 (not annualized if less than 1 year) 30 25 Brav er Tactical Allocation 20 60% S&P 500 / 40% BarCap AGG Return 15 5th to 25th Percentile 25th Percentile to Median 10 Median to 75th Percentile 5 75th to 95th Percentile 0 YTD 1 year 3 years 5 years GIPS Performance Disclosures Tactical Allocation Composite 1-January-2004 through 31-December-2010 Total Benchmark Internal Number of Total Composite Total Firm Year Return Return Dispersion Portfolios Assets ($Million) Assets ($Million) (percent) (percent) (percent) 2004 6.6 8.4 17 0.5 8.2 326.2 2005 1.0 3.9 67 0.5 19.0 334.4 2006 8.6 11.1 57 0.4 19.0 381.6 2007 2.8 6.2 57 0.6 21.1 394.5 2008 -7.1 -21.6 44 1.3 14.4 327.9 2009 15.6 18.5 96 0.6 26.4 432.4 2010 10.6 12.2 111 0.8 32.2 524.2 Braver Wealth Management, LLC. has prepared and presented this report in compliance with the Global Investment Performance Standards (GIPS®) 1 Braver Wealth Management, LLC. (f/k/a Tandem Financial Services Inc.) is an independent investment management firm established in 1987. The firm manages a variety of equity, fixed income, and balanced portfolios for individuals and institutions. Additional information regarding the firm's policies and procedures for calculating and reporting performance is available upon request. 2 The Tactical Allocation composite uses computer models to allocate assets among money market funds, US bonds, and US equity. The portfolios can have up to 100% in money markets, 75% in US equity, and 25% in US bonds. 3 The benchmark is 60% S&P 500 / 40% BarCap AGG. 4 This composite was created in January 1st, 2004. A complete list and description of firm composites is available upon request. 5 Valuations are computed and performance reported in US dollars. 6 Performance figures are presented before management and custodial fees but after all trading expenses. 7 Portfolios in this composite have a fixed fee schedule. The fixed fee is 1.00% on the first $2.5MM, 0.8% on the next $2.5 to $5MM, 0.6% on next $5 to $10MM and 0.4% over $10MM. 8 Internal dispersion is calculated using the equal-weighted standard deviation of all portfolios that were included in the composite for the entire year. Braver Wealth Management, LLC 117 Kendrick Street, Ste 800, Needham MA 02494 Ph: (617) 969-0223 www.braverwealth.com Email: ddamico@braverwealth.com