1. The Rough Road toward Fixed-

Mobile Convergence

The Impact of an NGN–/IMS–Based Strategy on

Telecommunications Operators

Carlos Ruiz Gómez

Telecommunications Manager

Everis

Fixed telephony providers are “Internetizing” their services and differentiating them from those

of other Internet companies in terms of features and content1, and mobile telephony operators are

heading in the same direction2. In turn, Internet access providers are threatening to become

telecommunications operators3, and cable operators are “invading” the competencies of telephony

and wideband access operators and vice versa4. An increasingly growing number of competitors

are driving operators and telecommunications service providers toward a consolidation that

started several years ago (i.e., the acquisition of mobile operator C&W HKT, Ltd., by PCCW in

2000) and continues to date (i.e., the advertisement of the acquisition this year of BellSouth by

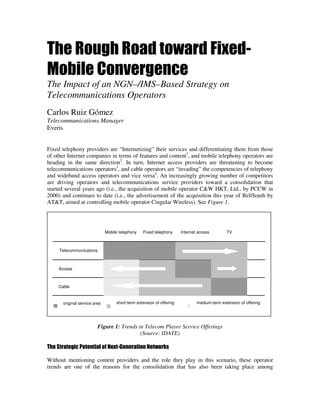

AT&T, aimed at controlling mobile operator Cingular Wireless). See Figure 1.

Mobile telephony Fixed telephony Internet access TV

Telecommunications

Access

Cable

original service area short-term extension of offering medium-term extension of offering

Figure 1: Trends in Telecom Player Service Offerings

(Source: IDATE)

The Strategic Potential of Next-Generation Networks

Without mentioning content providers and the role they play in this scenario, these operator

trends are one of the reasons for the consolidation that has also been taking place among

2. telecommunications network system manufacturers, thereby consolidating their own offering and

client portfolio5.

And there are many reasons for these trends in the telecommunications market. Naturally,

operators see their traditional business under threat: revenues from fixed telephony are

continually falling6, as with voice ARPU in mobile telephony7; the churn between mobile

operators has not declined8. The growing demands of users with regard to service quality and

ubiquity of access, in addition to the demand for new multimedia experiences (i.e., new types of

services), make attracting and retaining shop users increasingly difficult and costly, both in terms

of maintenance and network operation (insufficient client attention, poor service quality, and slow

problem resolution are the main causes for loss of business clients between mobile operators,

with a 34 percent drop in marketing and sales). See Figure 2.

4%

5%

5%

27%

7%

12%

22%

15%

Poor coverage Expensive prices / rates Custom er service

Dissatisfied w ith service provided Slow problem resolution Have other com petitive offers

Invoicing problem s Don't deliver as prom ised

Figure 2: Main Reasons Why Spanish SMBs Change Their Mobile Operator

(Source: The Telecommunications Market in Spanish SMBs, Everis)

This change in demand is no doubt influenced and expedited by new technologies. Faster access

speeds (i.e., enhanced data rates for Global System for Mobile Communications [EDGE];

evolution data optimized [EVDO] Revs. A and B and even C, which are already under

development; high-speed downlink packet access [HSDPA]; the forthcoming high-speed uplink

packet access [HSUPA] in Universal Mobile Telecommunications System [UMTS], future

standards such as long-term evolution) enhances the multimedia service offering. But the

traditional “silo” structure of current networks, with each type of service supplied under types of

access, transport media, and degree of control, severely hinders their development, maintenance,

and universalization; next-generation networks (NGNs) are the best option in this framework.

Each type of operator will start from a different technology and market situation, with different

3. types of access methods and different penetration in the user markets. Examples include the

following:

• Although fixed-access service providers in general will start from a heterogeneous

environment that will complicate migration to an all–Internet protocol (IP) architecture as

a first step toward NGNs, it must nevertheless be carried out. These providers will focus

primarily on developing their current services and enhancing them to combat growing

competition from cable operators. They must also consider convergent fixed-mobile

services (such as dual-mode services or fixed-mobile continuity, via protocols such as

unlicensed mobile access/general access network [UMA/GAN]) would allow their clients

to take advantage of fixed-access operators’ increasing presence in the wireless

environment, using their own infrastructure or renting it from mobile operators (i.e.,

mobile virtual network operators [MVNOs]).

• Mobile access providers must first adapt their networks to the new wireless wideband

standards and start developing a multimedia service catalog that leverages these faster

speeds. They should consider launching continuity services in conjunction with fixed

operators in regions where they cannot offer clients adequate coverage (e.g., third-world

countries). They should also think about systematically migrating all their networks to

all–IP so as not to eventually lose market share to the more aggressive fixed-access

operators in this aspect.

• Cable operators pose an obvious threat to fixed-access providers (in fact, there is a

growing number of agreements/joint ventures in the United States between mobile and

cable operators, in addition to these wanting to become MVNOs). These types of

providers can leverage and build on their multimedia and television services, in addition

to adopting the standard PacketCable that will allow them to launch services that compete

with the traditional services offered by telephony and fixed wideband access operators.

Therefore, by scaling the speed of adaptation of the types of operators to this new environment

and the launching of multimedia services, the question of whether the adoption of an NGN

architecture based on all–IP is based on a tactical (cost savings, due to the adoption of an IP–

based architecture) or strategic line of action (an attempt to increase the competitiveness of

operators based on a new source of income) quickly comes to mind. But the heavy initial

investment required (in view of which the effect of cost savings will by no means be felt

immediately) combined with the need for differentiation between convergent operators will make

an NGN a strategic option, capable of reducing the churn and driving revenues from new

services.

IP Multimedia Subsystems as Strategy Drivers

IP multimedia subsystems (IMS) form the cornerstone of NGNs, freeing the degree of control

over transport and application, unifying and freeing access type services, and defining a more

dynamic and collaborative multimedia service development framework (see Figure 3).

4. “Silo” architecture IMS architecture

Applicatio

Applicatio

Applicatio

Service Level –

Application and content

Applicatio

Applicatio

Applicatio

servers

Control Level –

Control

Control

Control

Control

Network, security, invoicing and

network interconnection control

Internet

Mobile

PSTN

Internet

Network Level –

Mobile

PSTN

Routers, switches and

gateways

Figure 3: IMS Frees Control and Transport

(Source: Everis)

While convergent services do not necessarily have to be based on IMS, they help speed fixed-

mobile convergence while operators migrate to IMS architecture (i.e., BT’s agreement with

Vodafone in the United Kingdom, or France Telecom’s Unik service). DMS’s pre–IMS

continuity services have become a trial-and-error method for service providers to measure the

demand and acceptance of fixed-mobile convergent services. But this method has its limitations,

such as it does not allow the user to evaluate the advantages of inter-service collaboration. For

this reason, service providers must have clear ideas of their evolution to a full–IMS environment

that will increase their competitive edge.

In fact, a closed network model severely hinders the development of services accessed by users.

Depending on the type of access, the services are deployed through a specialized and specific

set of network elements for that service and through a network access: the “silo” concept. Apart

from a specific network infrastructure, communication interfaces, and support applications,

each service requires its own “silo” and specific network elements and network management.

This silo may include a unique charging functionality, presence, list group management,

routing, and supply, which makes the construction and maintenance of this structure very

expensive.

IMS architecture emerges as a model that will unify the control layer between types of access

networks, standardizing the relationship between the network and services, thereby expediting

the development of the latter. IMS offers a network architecture whereby the software

infrastructure, due to the use of standards, allows network functionalities to be reused and

shared between multiple access networks, thus enabling the creation of services.

As a standard that expedites migration to NGN architecture, IMS should drive revenues from

new convergent services. This blurs the boundaries of current segmentation between cable

operators, wideband Internet access, and fixed and mobile (voice and data) services, thereby

5. intensifying competition between these and defining the new business relationships between the

players that cover different parts of the convergent service provider’s value chain. In this way,

the operator must relate to content providers in a different way and must depend increasingly

on third parties for external development and integration services.

Generation of New Revenues

IMS defines not the applications or services that can be offered to the end user, but rather a

network architecture that operators can use to generate an increasingly rich service offering.

However, IMS must ultimately expedite the development of multimedia and collaborative

services independent of the access network. IMS must expedite the following:

• IP multimedia sessions composed of diverse multimedia flows and content, with an

adequate level of service quality for video, audio, sound, text, application data, etc.

• Dynamic integration of media in the course of a communication (text, voice, video, etc.)

• Identification of users, services, and nodes through universal identifiers, which increases

usability of services for subscribers

• Information on user availability and communication capacity (PC or mobile connection,

multimedia capacities)

• Management and use of user groups in multi-user communications

• Fixed-mobile application convergence, as the system is independent from access

In fact, ABI Research predicts that world revenues from this type of service will reach U.S. $49.6

billion in 2011, in line with the trend that predicts that revenues from multimedia services will

replace voice services in operators’ bottom lines8.

For this purpose, operators must constantly reflect on the types of services that will soon be

demanded by users. This is of great importance, since service sale margins must not only

compensate development and production efforts, but also affect operation or competitiveness. For

example, Gartner proposes a mobile service identification method based on Maslow’s pyramid of

needs (see Figure 4). This method refers to the two essential concepts of mobility and

customization of the services to be developed, concepts that enable IMS services by freeing

access and simplifying development.

6. Source: Gartner

Maslow’s hierarchy of needs Revenue by type of need

Customization

Mobility and ubiquity

Figure 4: Identification of Services with Greater Revenue Generation Potential

But the industry no longer speaks of “killer applications.” In fact, voice services will continue to

lead due to their indispensable nature, as compared to others such as those aimed at the leisure

industry, but margins are undergoing a downward trend. Revenues from short message service

(SMS) are also expected to fall between now and 2010; they will drop 8 percent in western

Europe and up to 11.2 percent in eastern Europe9. Now it refers to a set of applications (bundles),

the value of which will increase parallel to their integration in the same session: according to

Lucent Bell Labs, “unique service churn varies between 1.7 and 2.5 percent, while bundle churn

based on multiple collaborative services drops between 1 and 1.5 percent,” boosting mobile

operator voice and data ARPU 40 percent on average during the next five years. Service bundling

is not new—it is used in double-, triple-, and quadruple-play offerings—and supposedly drive

revenues in proportion to the number of applications in the bundle (however, revenues are

estimated to stabilize on reaching four or five services in the same bundle). However, according

to Forrester only 1 percent of Italian consumers, 8 percent of French consumers and 10 percent of

British consumers have contracted triple-play services. In fact, an estimated 44 percent of

European consumers are not interested in bundles, thereby theoretically dismantling the

possibilities of success of this strategy. However, IMS allows applications to interact in a more

natural way, whereby bundles would evolve from a sales-oriented concept to a collaborative

service (blended services). This is expected to not only reduce churn, but also boost the number

of new contracts.

While each type of operator (fixed, mobile, cable, MVNO) adapts to an all–IP and IMS

environment at different speeds, they will all have different requirements—initial and strategic—

with regard to the type of services to be developed. In the long term, this will tend toward the

development of a similar product catalog by the different types of service providers in an

increasingly competitive manner (see Figure 5).

7. VoIP IP VideoTelephony IM

VCC On-Demand Conference

IP Centrex Click-to-dial

Online games VoiceMail Push-to-x

Fixed / cable

Convergent Offering

VoIP PodCasting IP VideoTelephony Online games

VCC PodCasting

Content-Sharing On-Demand Conference Click-to-dial

IP Centrex

IM Online games Content-Sharing

VoiceMail Push-to-x

Convergent

PodCasting IP VideoTelephony VoIP

IM

Content-Sharing On-Demand Conference Click-to-dial

Online games VoiceMail Push-to-x VCC

Mobile

Figure 5: Examples of Operator Approach to Services

(Source: Everis)

Thus, the identification of services and combinations of these in bundles according to type of

client, needs, and behavior, tending toward ultra-segmentation and marketing-to-one, will be

crucial. Complexity increases parallel to the uncertain and unpredictable demand for new services

with increasingly greater costs. The service catalog will depend on the type of operator (its

strategy), invoicing method, location, and type of user (massive/business). Those service provider

offerings that best adapt to client demands will generate greater fidelity and therefore higher

average revenue per user (ARPU) and revenues.

The Need for a More Flexible Environment …

The adoption of IMS should be a strategic rather than tactical line of action aimed at ensuring the

operator’s competitiveness. But this competitiveness would also be determined by the company’s

capacity to adapt to the new environment. Evidently, this affirmation will be more or less

vehement depending on the operator’s situation, e.g., if it is an incumbent, two-tier or new player;

in the last case, for example, the operator would have to be more aggressive in its value

proposition to end users, although the incumbent operator will generally carry greater dead

weight in its organization, such as a wider infrastructure and higher personnel costs. In this

section, we wish to emphasize the importance of the need to adapt to the new environment,

pointing out that cost savings are not immediately felt due to the complex nature of migration in a

fixed-mobile convergent environment favored by IMS.

The studies carried out indicate that cost savings will be achieved. According to Loudhouse for

Apertio, e.g., operator operational expenses (OPEX) will decrease 10 percent on adoption of IMS,

dropping from U.S. $805 million to U.S. $723 million. However, as we already anticipated, this

will require a heavy initial investment, and ABI Research foresees that operators worldwide will

8. invest a total of U.S. $10.1 billion in IMS infrastructure in the next five years and the return on

investment (ROI) will not be short-term (between two and five years, according to the same

source), although with a 5 percent decrease in capital expenses (CAPEX) (also according to the

same source). Additionally, operators are expected to spend U.S. $4 billion in service

development platforms (service delivery platforms) in the next five years and U.S. $470 million

in operations support systems (OSSs) (according to OSS Observer) at best. According to our own

experience, a business case based exclusively on investment and cost savings could have an even

longer payback period than expected.

Not counting personnel costs, which vary from country to country and can represent a high

percentage of the total adaptation costs of an incumbent operator, the initial cost of infrastructure

and next-generation OSSs and business support systems (BSSs) will account for the greater part

of initial investment costs. In addition to introducing new network elements, IMS will force

operators to take applicability into account in service management, the number of which must be

higher and with less time to market (TTM). For this reason, OSS and BSS systems are

particularly delicate, not only due to their importance to the operator’s capacity to manage its

network and relationship with clients, but also because these systems are not considered in the

scope of IMS. At present, current services are deployed on many platforms, each with its own

dedicated databases, interfaces, functionality, and interaction with OSSs and BSSs such as service

delivery and client attention. These services are either developed in silos or under a vertical

architecture. This method gives rise to significant technical problems on introduction of new

services, increasing both cost and TTM, which is contrary to one of the objectives of IMS and

NGNs. Additionally, the management and control of the deployed services are increasingly

expensive and confusing. Areas impacted by IMS in OSSs and BSSs include the following:

• Order management and fulfillment—The estimated number of service components

increases up to 100 times in customized services, while clients expect real-time order

fulfillment.

• Monitoring of resources—Service delivery must be ensured the first time around.

• Service quality—Service and quality as specified in the service-level agreement (SLA)

must be ensured.

• Mediation and invoicing—Users expect a convergent rate with a wide range of invoicing

options.

• Automation of outbound and inbound marketing tools with real or potential clients.

• Greater relevance of customer-experience management (CEM) systems to detect, track

and solve service availability problems; these systems can even become a differentiating

factor for operators.

The adaptation of systems to the IMS environment is one of the key aspects that must be

considered to ensure its ROI. The convergence of fixed-mobile access networks, the need for

greater operating efficiency, and a growing number of services with less TTM will force service

providers to change the systems map.

… That Includes the Organization and Processes

But infrastructure and system costs are not the only problems an operator must tackle in its

adaptation process. From the determination to migrate to a full–IMS environment to the

adaptation of its IT systems, internal processes, client attention, and even its own internal

organization, there are determinant factors in the operator’s capacity to offer a so-called optimum

user experience, which will become an even greater differentiating factor than it is today (see

9. Figure 6).

Project Portfolio Management

Excellence

Strategic Master

Plan Plan

Telco XXI

Initiatives

Business

Processes

Change Management

Figure 6: Aiming at Optimum User Experience through Operating Excellency

(Source: Everis)

Impact on the Organization

Although IMS is a network architecture—a technological concept—its implications on the

organization as a fixed-mobile convergence enabler are very important, and service providers will

have to reconsider their organizational structure. The boundary between the network and IT

systems is becoming increasingly blurred, in addition to the distinction of functions between

workstations in service providers. The following are examples of what must be considered:

• Redistribution of responsibilities between work teams (merger between networks and

systems, thereby strengthening the product marketing department, greater emphasis on

user support, etc.), giving more and more importance to certain functions (such as that of

service manager)

• Organizational adaptation to the new service/product life cycles (product life-cycle

management)

Additionally, as with all major projects that affect a company and its business model, it is very

important to be able to count on the support of the company’s management team.

Impact on Processes

For each value-chain model, and with business model characteristics based on NGN–IMS

architecture, the service provider must revise its third-party and client management processes.

The service provider must revise its processes with regard to different content providers and

other operators. Examples include the following:

• Management of client operations to ensure that content providers and other operators can

give an adequate response to the operation of services offered to end clients

• Integration of third-party needs (e.g., content providers) in procurement processes

10. • Definition and management of SLAs throughout the third-party chain (diverse providers)

to ensure correct delivery to the end client

• Alignment of invoicing processes to ensure that the service provider’s concepts and

processes for content provider invoicing are adequate and in accordance with service

capacities

It is also important for the operator to modify its client attraction/treatment processes, expediting

them, adapting and/or modifying them, creating new ones, and standardizing the processes

between the service provider’s departments to maintain user quality. Examples are as follows:

• Adaptation of invoicing processes to the new possibilities created by IMS

• Generalization of self-procurement and self-activation of services by clients

• Streamlining of attention processes for increasingly skilled users who increasingly

demand SLAs, homogenizing them between departments and creating processes to

improve user experience, detecting, tracking, and solving service availability problems

while managing end-to-end quality

All of these process modifications can be summarized in three concepts: the homogenization of

processes between the operator’s departments to lower costs; the automation of said processes to

improve end-client attention; and the generation of added value for the client.

IMS will not succeed in achieving these objectives unless operators tackle the impact of IMS, not

only from a technical point of view but also in terms of streamlined processes and business

generation. IMS, as an essential part of a next-generation fixed-mobile convergent network, not

only favors an agile operating environment, but also needs this greater agility, which impacts

everything from network infrastructure maintenance to the organization, process by process,

resulting in improved service to end clients: the concepts of lean and agile operations as a way of

guaranteeing the competitiveness of telecommunications operators.

Conclusion

Taking the figures and timelines anticipated above as a more or less accurate reference, and in

spite of the many challenges, fixed-mobile convergence must be adopted by operators, since it is

the IMS standard and a key part of its implementation.

But beyond the technological challenge, the identification of services (which includes

customization as a client acceptance strategy) is probably one of the areas of greatest difficulty

and greatest strategic impact.

In this way, this new environment does not exclusively affect network infrastructure and

operation, but also impacts corporate strategy; marketing, product, and service launches (defining

new product/service catalogs, which are increasingly segmented by client type and are no longer

offered individually but in bundles that favor cross-selling of services); and business operations

(see Figure 7).

11. •Customer

•Processes •Systems

• Are the processes sufficiently • Can current OSS and BSS systems support

automated to adapt to the new IMS requirements?

business model?

• Is attention in line with customer •Operator • Are the SDP platforms IMS-ready (operators

will invest US$4B in these platforms over the

1

expectations? next 5 years )?

•Organization •Network

• Does the operator already have an IP

infrastructure in place? Is there a plan to

• Do fixed and mobile areas operate independently in migrate to All-IP?

the case of convergent operators?

• Does the operator have multiple network

• Have timely alliances been established with relevant equipment suppliers?

market players?

Figure 7: The Operator Approach towards Customers

(Source: Everis)

Each type of operator will have different requirements and will adapt to the new rules at different

speeds, being the remainder of the period 2006–08 key to said adaptation (see Figure 8).

Figure 8: Examples of Operator Approaches to Services

Eventually, service providers will tend toward offering a similar service catalog, making fast

adaptation to the new environment crucial to operator competitiveness. In this way, launching

12. new services, adapting them to client needs, and quickly supplying an optimum user experience

become the most powerful strategies to drive operator growth, though clients must be able to

perceive the value of those services. Access control does not guarantee client retention:

customization, brand, and service value are the differentiating factors of the new model.

Carlos Ruiz Gómez

Gerente Telecomunicaciones – Innovación

Pº del Club Deportivo s/n, Bloque 10, La Finca

28223, Pozuelo de Alarcón - Madrid

Notes:

1

Attempt by operators to control IP traffic (according to IDC, the number of minutes of VoIP will

increase 717 percent from 2006–09), placing special emphasis on service quality, for example.

2

Siemens foresees a decrease in monthly mobile voice ARPU of 18 percent from 2006–09.

3

Positioning of Skype as a new type of voice service provider.

4

Multiple-system operators (MSOs) launch voice services and ADSL wideband fixed access

providers launch TV services.

5

Merger between Lucent and Alcatel and agreement between Nokia and Siemens.

6

Gartner foresees that revenues from traditional PSTN telephony in the 10 largest European

operators will drop approximately 30 percent from 2006–09.

7

See note 2.

8

According to the same source and in the same period and region as in note 2, the representativity

of monthly voice ARPU in the total will decrease approximately 28 percent in favor of data and

multimedia services.

9

EnterData as from GSMA, Ovum, and Tekelek.

![telecommunications network system manufacturers, thereby consolidating their own offering and

client portfolio5.

And there are many reasons for these trends in the telecommunications market. Naturally,

operators see their traditional business under threat: revenues from fixed telephony are

continually falling6, as with voice ARPU in mobile telephony7; the churn between mobile

operators has not declined8. The growing demands of users with regard to service quality and

ubiquity of access, in addition to the demand for new multimedia experiences (i.e., new types of

services), make attracting and retaining shop users increasingly difficult and costly, both in terms

of maintenance and network operation (insufficient client attention, poor service quality, and slow

problem resolution are the main causes for loss of business clients between mobile operators,

with a 34 percent drop in marketing and sales). See Figure 2.

4%

5%

5%

27%

7%

12%

22%

15%

Poor coverage Expensive prices / rates Custom er service

Dissatisfied w ith service provided Slow problem resolution Have other com petitive offers

Invoicing problem s Don't deliver as prom ised

Figure 2: Main Reasons Why Spanish SMBs Change Their Mobile Operator

(Source: The Telecommunications Market in Spanish SMBs, Everis)

This change in demand is no doubt influenced and expedited by new technologies. Faster access

speeds (i.e., enhanced data rates for Global System for Mobile Communications [EDGE];

evolution data optimized [EVDO] Revs. A and B and even C, which are already under

development; high-speed downlink packet access [HSDPA]; the forthcoming high-speed uplink

packet access [HSUPA] in Universal Mobile Telecommunications System [UMTS], future

standards such as long-term evolution) enhances the multimedia service offering. But the

traditional “silo” structure of current networks, with each type of service supplied under types of

access, transport media, and degree of control, severely hinders their development, maintenance,

and universalization; next-generation networks (NGNs) are the best option in this framework.

Each type of operator will start from a different technology and market situation, with different](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)