Recommended

More Related Content

Viewers also liked

Viewers also liked (14)

Similar to Minneapolis–St. Paul Office Insight Q4 2015

Similar to Minneapolis–St. Paul Office Insight Q4 2015 (20)

More from Carolyn Bates

More from Carolyn Bates (20)

Recently uploaded

Recently uploaded (20)

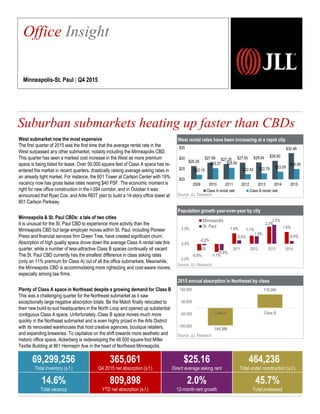

Minneapolis–St. Paul Office Insight Q4 2015

- 1. West rental rates have been increasing at a rapid clip Source: JLL Research Population growth year-over-year by city Source: JLL Research 2015 annual absorption in Northeast by class Source: JLL Research West submarket now the most expensive The first quarter of 2015 was the first time that the average rental rate in the West surpassed any other submarket, notably including the Minneapolis CBD. This quarter has seen a marked cost increase in the West as more premium space is being listed for lease. Over 50,000 square feet of Class A space has re- entered the market in recent quarters, drastically raising average asking rates in an already tight market. For instance, the 601 Tower at Carlson Center with 19% vacancy now has gross lease rates nearing $40 PSF. The economic moment is right for new office construction in the I-394 corridor, and in October it was announced that Ryan Cos. and Artis REIT plan to build a 14-story office tower at 801 Carlson Parkway. Minneapolis & St. Paul CBDs: a tale of two cities It is unusual for the St. Paul CBD to experience more activity than the Minneapolis CBD but large employer moves within St. Paul, including Pioneer Press and financial services firm Green Tree, have created significant churn. Absorption of high quality space drove down the average Class A rental rate this quarter, while a number of less-attractive Class B spaces continually sit vacant The St. Paul CBD currently has the smallest difference in class asking rates (only an 11% premium for Class A) out of all the office submarkets. Meanwhile, the Minneapolis CBD is accommodating more rightsizing and cost-aware moves, especially among law firms. Plenty of Class A space in Northeast despite a growing demand for Class B This was a challenging quarter for the Northeast submarket as it saw exceptionally large negative absorption totals. Be the Match finally relocated to their new build-to-suit headquarters in the North Loop and opened up substantial contiguous Class A space. Unfortunately, Class B space moves much more quickly in the Northeast submarket and is even highly prized in the Arts District with its renovated warehouses that host creative agencies, boutique retailers, and expanding breweries. To capitalize on the shift towards more aesthetic and historic office space, Ackerberg is redeveloping the 48,500 square foot Miller Textile Building at 861 Hennepin Ave in the heart of Northeast Minneapolis. Suburban submarkets heating up faster than CBDs 2,257 $26.29 $27.89 $27.25 $27.93 $28.04 $28.80 $32.48 $22.15 $25.27 $25.50 $22.42 $22.79 $23.59 $24.90 $20 $25 $30 $35 2009 2010 2011 2012 2013 2014 2015 Class A rental rate Class B rental rate Office Insight Minneapolis-St. Paul | Q4 2015 69,299,256 Total inventory (s.f.) 365,061 Q4 2015 net absorption (s.f.) $25.16 Direct average asking rent 464,236 Total under construction (s.f.) 14.6% Total vacancy 809,898 YTD net absorption (s.f.) 2.0% 12-month rent growth 45.7% Total preleased -0.9% -1.1% 1.4% 1.1% 2.3% 1.6% -0.2% -0.8% 0.5% 1.0% 2.5% 0.4% -2.0% 0.0% 2.0% 2009 2010 2011 2012 2013 2014 Minneapolis St. Paul -144,266 110,394 -150,000 -50,000 50,000 150,000 Class A Class B

- 2. Current conditions – submarket Historical leasing activity (s.f.) Source: JLL Research Source: JLL Research Total net absorption (s.f.) Source: JLL Research Total vacancy rate (%) Source: JLL Research Direct average asking rent ($ p.s.f.) Source: JLL Research 966,371 929,169 253,779 -1,661,963 -312,099 585,965 174,317 63,187 913,797 809,898 -2,000,000 -1,500,000 -1,000,000 -500,000 0 500,000 1,000,000 1,500,000 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 $22.78 $23.32 $23.89 $23.92 $23.58 $23.50 $23.94 $24.35 $24.66 $25.16 $20.00 $22.00 $24.00 $26.00 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 18.0% 16.3% 15.8% 18.2% 18.7% 17.8% 17.5% 17.4% 16.0% 14.6% 12.0% 14.0% 16.0% 18.0% 20.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Landlordleverage Tenantleverage Peaking market Falling market Bottoming market Rising market 4,126,595 4,378,569 4,111,400 3,837,051 3,400,000 3,600,000 3,800,000 4,000,000 4,200,000 4,400,000 4,600,000 2012 2013 2014 2015 ©2015 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Carolyn Bates | carolyn.bates@am.jll.com Southwest Minneapolis CBD Southeast Northeast St. Paul CBD Northwest West Minneapolis market