Recommended

Recommended

More Related Content

Similar to Form 2106 Employee Business Expenses

Similar to Form 2106 Employee Business Expenses (20)

More from budbarber38650

More from budbarber38650 (20)

Recently uploaded

Recently uploaded (20)

Form 2106 Employee Business Expenses

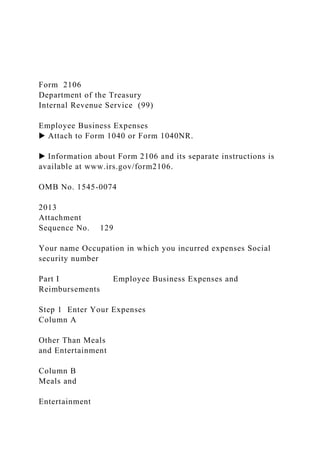

- 1. Form 2106 Department of the Treasury Internal Revenue Service (99) Employee Business Expenses ▶ Attach to Form 1040 or Form 1040NR. ▶ Information about Form 2106 and its separate instructions is available at www.irs.gov/form2106. OMB No. 1545-0074 2013 Attachment Sequence No. 129 Your name Occupation in which you incurred expenses Social security number Part I Employee Business Expenses and Reimbursements Step 1 Enter Your Expenses Column A Other Than Meals and Entertainment Column B Meals and Entertainment

- 2. 1 Vehicle expense from line 22 or line 29. (Rural mail carriers: See instructions.) . . . . . . . . . . . . . . . . . . 1 2 Parking fees, tolls, and transportation, including train, bus, etc., that did not involve overnight travel or commuting to and from work . 2 3 Travel expense while away from home overnight, including lodging, airplane, car rental, etc. Do not include meals and entertainment . 3 4 Business expenses not included on lines 1 through 3. Do not include meals and entertainment . . . . . . . . . . . . . . 4 5 Meals and entertainment expenses (see instructions) . . . . . 5 6 Total expenses. In Column A, add lines 1 through 4 and enter the result. In Column B, enter the amount from line 5 . . . . . . 6 Note: If you were not reimbursed for any expenses in Step 1, skip line 7 and enter the amount from line 6 on line 8. Step 2 Enter Reimbursements Received From Your Employer for Expenses Listed in Step 1 7

- 3. Enter reimbursements received from your employer that were not reported to you in box 1 of Form W-2. Include any reimbursements reported under code “L” in box 12 of your Form W-2 (see instructions) . . . . . . . . . . . . . . . . . . . 7 Step 3 Figure Expenses To Deduct on Schedule A (Form 1040 or Form 1040NR) 8 Subtract line 7 from line 6. If zero or less, enter -0-. However, if line 7 is greater than line 6 in Column A, report the excess as income on Form 1040, line 7 (or on Form 1040NR, line 8) . . . . . . . 8 Note: If both columns of line 8 are zero, you cannot deduct employee business expenses. Stop here and attach Form 2106 to your return. 9 In Column A, enter the amount from line 8. In Column B, multiply line 8 by 50% (.50). (Employees subject to Department of Transportation (DOT) hours of service limits: Multiply meal expenses incurred while away from home on business by 80% (.80) instead of 50%. For

- 4. details, see instructions.) . . . . . . . . . . . . . . 9 10 Add the amounts on line 9 of both columns and enter the total here. Also, enter the total on Schedule A (Form 1040), line 21 (or on Schedule A (Form 1040NR), line 7). (Armed Forces reservists, qualified performing artists, fee-basis state or local government officials, and individuals with disabilities: See the instructions for special rules on where to enter the total.) . . . . . ▶ 10 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11700N Form 2106 (2013) Form 2106 (2013) Page 2 Part II Vehicle Expenses Section A—General Information (You must complete this section if you are claiming vehicle expenses.) (a) Vehicle 1 (b) Vehicle 2 11 Enter the date the vehicle was placed in service . . . . . . . . . 11 / / / / 12 Total miles the vehicle was driven during 2013 . . . . . . . . . 12 miles miles 13 Business miles included on line 12 . . . . . . . . . . . . . 13 miles miles 14 Percent of business use. Divide line 13 by line 12 . . . . . . . .

- 5. . 14 % % 15 Average daily roundtrip commuting distance . . . . . . . . . . 15 miles miles 16 Commuting miles included on line 12 . . . . . . . . . . . . 16 miles miles 17 Other miles. Add lines 13 and 16 and subtract the total from line 12 . . 17 miles miles 18 Was your vehicle available for personal use during off-duty hours? . . . . . . . . . . . . . Yes No 19 Do you (or your spouse) have another vehicle available for personal use? . . . . . . . . . . . Yes No 20 Do you have evidence to support your deduction? . . . . . . . . . . . . . . . . . . Yes No 21 If “Yes,” is the evidence written? . . . . . . . . . . . . . . . . . . . . . . . . Yes No Section B—Standard Mileage Rate (See the instructions for Part II to find out whether to complete this section or Section C.) 22 Multiply line 13 by 56.5¢ (.565). Enter the result here and on line 1 . . . . . . . . . . 22 Section C—Actual Expenses (a) Vehicle 1 (b) Vehicle 2 23 Gasoline, oil, repairs, vehicle insurance, etc. . . . . . . 23 24a Vehicle rentals . . . . . . 24a b Inclusion amount (see instructions) . 24b c Subtract line 24b from line 24a . 24c 25 Value of employer-provided vehicle (applies only if 100% of annual lease value was included on Form W-2—see instructions) . . . . 25

- 6. 26 Add lines 23, 24c, and 25 . . . 26 27 Multiply line 26 by the percentage on line 14 . . . . . . . . 27 28 Depreciation (see instructions) . 28 29 Add lines 27 and 28. Enter total here and on line 1 . . . . . 29 Section D—Depreciation of Vehicles (Use this section only if you owned the vehicle and are completing Section C for the vehicle.) (a) Vehicle 1 (b) Vehicle 2 30 Enter cost or other basis (see instructions) . . . . . . . 30 31 Enter section 179 deduction and special allowance (see instructions) 31 32 Multiply line 30 by line 14 (see instructions if you claimed the section 179 deduction or special allowance). . . . . . . . 32 33 Enter depreciation method and percentage (see instructions) . 33 34 Multiply line 32 by the percentage on line 33 (see instructions) . . 34 35 Add lines 31 and 34 . . . . 35 36 Enter the applicable limit explained in the line 36 instructions . . . 36 37 Multiply line 36 by the percentage

- 7. on line 14 . . . . . . . . 37 38 Enter the smaller of line 35 or line 37. If you skipped lines 36 and 37, enter the amount from line 35. Also enter this amount on line 28 above . . . . . . . . . 38 Form 2106 (2013) Version A, Cycle 2 Internal Use Only DRAFT AS OF April 17, 2013 2013 Form 2106 SE:W:CAR:MP Employee Business Expenses Form 2106 Department of the Treasury Internal Revenue Service (99) Employee Business Expenses ▶ Attach to Form 1040 or Form 1040NR. ▶ Information about Form 2106 and its separate instructions is available at www.irs.gov/form2106. OMB No. 1545-0074 2013 2013. Catalog number 11700N. Attachment Sequence No. 129 Attachment Sequence Number 129. For Paperwork Reduction Act Notice, see your tax return instructions. Social security number Part I Employee Business Expenses and Reimbursements

- 8. Step 1 Enter Your Expenses Column A Other Than Meals and Entertainment Column B Meals and Entertainment 1 Vehicle expense from line 22 or line 29. (Rural mail carriers: See instructions.) 1 2 Parking fees, tolls, and transportation, including train, bus, etc., that did not involve overnight travel or commuting to and from work 2 3 Travel expense while away from home overnight, including lodging, airplane, car rental, etc. Do not include meals and entertainment 3 4 Business expenses not included on lines 1 through 3. Do not include meals and entertainment 4 5 Meals and entertainment expenses (see instructions) 5 6 Total expenses. In Column A, add lines 1 through 4 and enter

- 9. the result. In Column B, enter the amount from line 5 6 Note: If you were not reimbursed for any expenses in Step 1, skip line 7 and enter the amount from line 6 on line 8. Step 2 Enter Reimbursements Received From Your Employer for Expenses Listed in Step 1 Column A. Other Than Meals and Entertainment. Column A. Other Than Meals and Entertainment. Column A. Other Than Meals and Entertainment. Column B. Meals and Entertainment. Column B. Meals and Entertainment. Column B. Meals and Entertainment. 7 Enter reimbursements received from your employer that were not reported to you in box 1 of Form W-2. Include any reimbursements reported under code “L” in box 12 of your Form W-2 (see instructions) 7 Step 3 Figure Expenses To Deduct on Schedule A (Form 1040 or Form 1040NR) Column A. Other Than Meals and Entertainment. Column A. Other Than Meals and Entertainment. Column A. Other Than Meals and Entertainment. Column B. Meals and Entertainment. Column B. Meals and Entertainment. Column B. Meals and Entertainment. 8 Subtract line 7 from line 6. If zero or less, enter -0-. However, if line 7 is greater than line 6 in Column A, report the excess as income on Form 1040, line 7 (or on Form 1040NR, line 8)

- 10. 8 Note: If both columns of line 8 are zero, you cannot deduct employee business expenses. Stop here and attach Form 2106 to your return. 9 In Column A, enter the amount from line 8. In Column B, multiply line 8 by 50% (.50). (Employees subject to Department of Transportation (DOT) hours of service limits: Multiply meal expenses incurred while away from home on business by 80% (.80) instead of 50%. For details, see instructions.) 9 10 Add the amounts on line 9 of both columns and enter the total here. Also, enter the total on Schedule A (Form 1040), line 21 (or on Schedule A (Form 1040NR), line 7). (Armed Forces reservists, qualified performing artists, fee-basis state or local government officials, and individuals with disabilities: See the instructions for special rules on where to enter the total.) ▶ Add the amounts on line 9 of both columns and enter the total here. Also, enter the total on Schedule A (Form 1040), line 21 (or on Schedule A (Form 1040NR), line 7). (Armed Forces reservists, qualified performing artists, fee-basis state or local government officials, and individuals with disabilities: See the instructions for special rules on where to enter the total.) 10 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11700N

- 11. Form 2106 (2013) Form 2106 (2013) Page 2 Part II Vehicle Expenses Section A—General Information (You must complete this section if you are claiming vehicle expenses.) (a) Vehicle 1 (b) Vehicle 2 11 Enter the date the vehicle was placed in service 11 12 Total miles the vehicle was driven during 2013 12 13 Business miles included on line 12 13 14 Percent of business use. Divide line 13 by line 12 14 15 Average daily roundtrip commuting distance 15 16 Commuting miles included on line 12 16 17 Other miles. Add lines 13 and 16 and subtract the total from line 12 17 18 Was your vehicle available for personal use during off-duty hours? 19

- 12. Do you (or your spouse) have another vehicle available for personal use? 20 Do you have evidence to support your deduction? 21 If “Yes,” is the evidence written? Section B—Standard Mileage Rate (See the instructions for Part II to find out whether to complete this section or Section C.) 22 Multiply line 13 by 56.5¢ (.565). Enter the result here and on line 1 22 Section C—Actual Expenses (a) Vehicle 1 (b) Vehicle 2 23 Gasoline, oil, repairs, vehicle insurance, etc. 23 24a Vehicle rentals 24a b Inclusion amount (see instructions) 24b c Subtract line 24b from line 24a 24c 25 Value of employer-provided vehicle (applies only if 100% of annual lease value was included on Form W-2—see instructions) 25 26 Add lines 23, 24c, and 25 26 27

- 13. Multiply line 26 by the percentage on line 14 27 28 Depreciation (see instructions) 28 29 Add lines 27 and 28. Enter total here and on line 1 29 Section D—Depreciation of Vehicles (Use this section only if you owned the vehicle and are completing Section C for the vehicle.) (a) Vehicle 1 (b) Vehicle 2 30 Enter cost or other basis (see instructions) 30 31 Enter section 179 deduction and special allowance (see instructions) 31 32 Multiply line 30 by line 14 (see instructions if you claimed the section 179 deduction or special allowance) 32 33 Enter depreciation method and percentage (see instructions) 33 34 Multiply line 32 by the percentage on line 33 (see instructions) 34 35 Add lines 31 and 34 35 36

- 14. Enter the applicable limit explained in the line 36 instructions 36 37 Multiply line 36 by the percentage on line 14 37 38 Enter the smaller of line 35 or line 37. If you skipped lines 36 and 37, enter the amount from line 35. Also enter this amount on line 28 above 38 Form 2106 (2013) p1-t1: p1-t2: p1-t3: p1-t50: p1-t51: p1-t6: p1-t7: p1-t8: p1-t9: p1-t10: p1-t11: p1-t12: p1-t13: p1-t14: p1-t15: p1-t16: p1-t17: p1-t18: p1-t19: p1-t20: p1-t21: p1-t22: p1-t23: p1-t24: p1-t25: p1-t26: p1-t27: p1-t28: p1-t29: p1-t30: p1-t31: p1-t32: p1-t33: p2-t1: p2-t2: p2-t3: p2-t4: p2-t5: p2-t6: p2-t7: p2-t8: p2-t9: p2- t10: p2-t11: p2-t12: p2-t13: p2-t14: p2-t15: p2-t16: p2-t17: p2- t18: p2-cb4: p2-cb5: p2-cb6: p2-cb7: p2-t23: p2-t24: p2-t25: p2- t26: p2-t27: p2-t28: p2-t29: p2-t30: p2-t31: p2-t32: p2-t33: p2- t34: p2-t35: p2-t36: p2-t37: p2-t38: p2-t39: p2-t40: p2-t41: p2- t42: p2-t43: p2-t44: p2-t45: p2-t46: p2-t47: p2-t48: p2-t49: p2- t50: p2-t51: p2-t52: p2-t53: p2-t54: p2-t55: p2-t56: p2-t57: p2- t58: p2-t59: p2-t60: p2-t61: p2-t62: p2-t63: p2-t64: p2-t65: p2- t66: p2-t67: p2-t68: p2-t69: p2-t70: p2-t71: p2-t72: p2-t73: p2- t74: p2-t75: p2-t76: p2-t77: p2-t78: p2-t79: p2-t80: p2-t81: p2- t82: p2-t83: p2-t84: p2-t85: p2-t86: p2-t87: p2-t88: p2-t89: p2- t90: p2-t91: p2-t92: p2-t93: p2-t94: Form 8606 Department of the Treasury Internal Revenue Service (99) Nondeductible IRAs

- 15. ▶ Information about Form 8606 and its separate instructions is at www.irs.gov/form8606. ▶ Attach to Form 1040, Form 1040A, or Form 1040NR. OMB No. 1545-0074 2013 Attachment Sequence No. 48 Name. If married, file a separate form for each spouse required to file Form 8606. See instructions. Your social security number Fill in Your Address Only If You Are Filing This Form by Itself and Not With Your Tax Return ▲ Home address (number and street, or P.O. box if mail is not delivered to your home) Apt. no. City, town or post office, state, and ZIP code. If you have a foreign address, also complete the spaces below (see instructions). Foreign country name Foreign province/state/county Foreign postal code Part I Nondeductible Contributions to Traditional IRAs and Distributions From Traditional, SEP, and SIMPLE IRAs Complete this part only if one or more of the following apply. • You made nondeductible contributions to a traditional IRA for 2013.

- 16. • You took distributions from a traditional, SEP, or SIMPLE IRA in 2013 and you made nondeductible contributions to a traditional IRA in 2013 or an earlier year. For this purpose, a distribution does not include a rollover, qualified charitable distributions, one-time distribution to fund an HSA, conversion, recharacterization, or return of certain contributions. • You converted part, but not all, of your traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013 (excluding any portion you recharacterized) and you made nondeductible contributions to a traditional IRA in 2013 or an earlier year. 1 Enter your nondeductible contributions to traditional IRAs for 2013, including those made for 2013 from January 1, 2014, through April 15, 2014 (see instructions) . . . . . . . . . . . . 1 2 Enter your total basis in traditional IRAs (see instructions) . . . . . . . . . . . . . . 2 3 Add lines 1 and 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 In 2013, did you take a distribution from traditional, SEP, or SIMPLE IRAs, or make a Roth IRA conversion? No ▶ Enter the amount from line 3 on line 14. Do not complete the rest of Part I. Yes ▶ Go to line 4. 4 Enter those contributions included on line 1 that were made from January 1, 2014, through April 15, 2014 4 5 Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . . . . . 5

- 17. 6 Enter the value of all your traditional, SEP, and SIMPLE IRAs as of December 31, 2013, plus any outstanding rollovers (see instructions) . . 6 7 Enter your distributions from traditional, SEP, and SIMPLE IRAs in 2013. Do not include rollovers, qualified charitable distributions, a one- time distribution to fund an HSA, conversions to a Roth IRA, certain returned contributions, or recharacterizations of traditional IRA contributions (see instructions) . . . . . . . . . . . . . . 7 8 Enter the net amount you converted from traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013. Do not include amounts converted that you later recharacterized (see instructions). Also enter this amount on line 16 . 8 9 Add lines 6, 7, and 8 . . . . . . . . 9 10

- 18. Divide line 5 by line 9. Enter the result as a decimal rounded to at least 3 places. If the result is 1.000 or more, enter “1.000” . . . . . . 10 × . 11 Multiply line 8 by line 10. This is the nontaxable portion of the amount you converted to Roth IRAs. Also enter this amount on line 17 . . . 11 12 Multiply line 7 by line 10. This is the nontaxable portion of your distributions that you did not convert to a Roth IRA . . . . . . . 12 13 Add lines 11 and 12. This is the nontaxable portion of all your distributions . . . . . . . . 13 14 Subtract line 13 from line 3. This is your total basis in traditional IRAs for 2013 and earlier years 14 15 Taxable amount. Subtract line 12 from line 7. If more than zero, also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b . . . . . . . . . . . . 15 Note. You may be subject to an additional 10% tax on the amount on line 15 if you were under age 59½ at the time of the distribution (see instructions).

- 19. For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 63966F Form 8606 (2013) Form 8606 (2013) Page 2 Part II 2013 Conversions From Traditional, SEP, or SIMPLE IRAs to Roth IRAs Complete this part if you converted part or all of your traditional, SEP, and SIMPLE IRAs to a Roth IRA in 2013 (excluding any portion you recharacterized). 16 If you completed Part I, enter the amount from line 8. Otherwise, enter the net amount you converted from traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013. Do not include amounts you later recharacterized back to traditional, SEP, or SIMPLE IRAs in 2013 or 2014 (see instructions) 16 17 If you completed Part I, enter the amount from line 11. Otherwise, enter your basis in the amount on line 16 (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . 17 18

- 20. Taxable amount. Subtract line 17 from line 16. Also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b . . . . . . . . . . . . . . . . . 18 Part III Distributions From Roth IRAs Complete this part only if you took a distribution from a Roth IRA in 2013. For this purpose, a distribution does not include a rollover, qualified charitable distributions, a one-time distribution to fund an HSA, recharacterization, or return of certain contributions (see instructions). 19 Enter your total nonqualified distributions from Roth IRAs in 2013, including any qualified first-time homebuyer distributions (see instructions) . . . . . . . . . . . . . . . . . . . 19 20 Qualified first-time homebuyer expenses (see instructions). Do not enter more than $10,000 . . 20 21 Subtract line 20 from line 19. If zero or less, enter -0- and skip lines 22 through 25 . . . . . . . 21 22 Enter your basis in Roth IRA contributions (see instructions) . . . . . . . . . . . . . 22 23 Subtract line 22 from line 21. If zero or less, enter -0- and skip lines 24 and 25. If more than zero, you may be subject to an additional tax (see instructions) . . . . . . . . . . . . . . 23 24

- 21. Enter your basis in conversions from traditional, SEP, and SIMPLE IRAs and rollovers from qualified retirement plans to a Roth IRA (see instructions) . . . . . . . . . . . . . . 24 25 Taxable amount. Subtract line 24 from line 23. If more than zero, also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b . . . . . . . . . . 25 Sign Here Only If You Are Filing This Form by Itself and Not With Your Tax Return Under penalties of perjury, I declare that I have examined this form, including accompanying attachments, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. ▲ Your signature ▲ Date Paid Preparer Use Only Print/Type preparer’s name Preparer’s signature Date Check

- 22. if self-employed PTIN Firm's name ▶ Firm's address ▶ Firm's EIN ▶ Phone no. Form 8606 (2013) Version A, Cycle 4 Internal Use Only Draft As Of June 4, 2013 2013 Form 8606 SE:W:CAR:MP Nondeductible IRAs Form 8606 Department of the Treasury Internal Revenue Service (99) Nondeductible IRAs ▶ Information about Form 8606 and its separate instructions is at www.irs.gov/form8606. ▶ Attach to Form 1040, Form 1040A, or Form 1040NR. OMB No. 1545-0074 2013 2013. Catalog number 63966F. Attachment Sequence No. 48 Attachment sequence number 48. For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Fill in Your Address Only If You Are Filing This Form by Itself

- 23. and Not With Your Tax Return ▲ Part I Nondeductible Contributions to Traditional IRAs and Distributions From Traditional, SEP, and SIMPLE IRAs Complete this part only if one or more of the following apply. • You made nondeductible contributions to a traditional IRA for 2013. • You took distributions from a traditional, SEP, or SIMPLE IRA in 2013 and you made nondeductible contributions to a traditional IRA in 2013 or an earlier year. For this purpose, a distribution does not include a rollover, qualified charitable distributions, one-time distribution to fund an HSA, conversion, recharacterization, or return of certain contributions. • You converted part, but not all, of your traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013 (excluding any portion you recharacterized) and you made nondeductible contributions to a traditional IRA in 2013 or an earlier year. 1 Enter your nondeductible contributions to traditional IRAs for 2013, including those made for 2013 from January 1, 2014, through April 15, 2014 (see instructions) 1 2 Enter your total basis in traditional IRAs (see instructions) 2 3 Add lines 1 and 2 3 In 2013, did you take a distribution from traditional, SEP, or SIMPLE IRAs, or make a Roth IRA conversion? No ▶ Enter the amount from line 3 on line 14. Do not complete the

- 24. rest of Part I. Yes ▶ Go to line 4. 4 Enter those contributions included on line 1 that were made from January 1, 2014, through April 15, 2014 4 5 Subtract line 4 from line 3 5 6 Enter the value of all your traditional, SEP, and SIMPLE IRAs as of December 31, 2013, plus any outstanding rollovers (see instructions) 6 7 Enter your distributions from traditional, SEP, and SIMPLE IRAs in 2013. Do not include rollovers, qualified charitable distributions, a one-time distribution to fund an HSA, conversions to a Roth IRA, certain returned contributions, or recharacterizations of traditional IRA contributions (see instructions) 7 8 Enter the net amount you converted from traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013. Do not include amounts converted that you later recharacterized (see instructions). Also enter this amount on line 16

- 25. 8 9 Add lines 6, 7, and 8 9 10 Divide line 5 by line 9. Enter the result as a decimal rounded to at least 3 places. If the result is 1.000 or more, enter “1.000” 10 11 Multiply line 8 by line 10. This is the nontaxable portion of the amount you converted to Roth IRAs. Also enter this amount on line 17 11 12 Multiply line 7 by line 10. This is the nontaxable portion of your distributions that you did not convert to a Roth IRA 12 13 Add lines 11 and 12. This is the nontaxable portion of all your distributions 13 14 Subtract line 13 from line 3. This is your total basis in traditional IRAs for 2013 and earlier years 14 15 Taxable amount. Subtract line 12 from line 7. If more than zero, also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b 15 Note. You may be subject to an additional 10% tax on the

- 26. amount on line 15 if you were under age 59½ at the time of the distribution (see instructions). For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 63966F Form 8606 (2013) Form 8606 (2013) Page 2 Part II 2013 Conversions From Traditional, SEP, or SIMPLE IRAs to Roth IRAs Complete this part if you converted part or all of your traditional, SEP, and SIMPLE IRAs to a Roth IRA in 2013 (excluding any portion you recharacterized). 16 If you completed Part I, enter the amount from line 8. Otherwise, enter the net amount you converted from traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2013. Do not include amounts you later recharacterized back to traditional, SEP, or SIMPLE IRAs in 2013 or 2014 (see instructions) 16 17 If you completed Part I, enter the amount from line 11. Otherwise, enter your basis in the amount on line 16 (see instructions) 17 18 Taxable amount. Subtract line 17 from line 16. Also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b 18 Part III

- 27. Distributions From Roth IRAs Complete this part only if you took a distribution from a Roth IRA in 2013. For this purpose, a distribution does not include a rollover, qualified charitable distributions, a one-time distribution to fund an HSA, recharacterization, or return of certain contributions (see instructions). 19 Enter your total nonqualified distributions from Roth IRAs in 2013, including any qualified first-time homebuyer distributions (see instructions) 19 20 Qualified first-time homebuyer expenses (see instructions). Do not enter more than $10,000 20 21 Subtract line 20 from line 19. If zero or less, enter -0- and skip lines 22 through 25 21 22 Enter your basis in Roth IRA contributions (see instructions) 22 23 Subtract line 22 from line 21. If zero or less, enter -0- and skip lines 24 and 25. If more than zero, you may be subject to an additional tax (see instructions) 23 24 Enter your basis in conversions from traditional, SEP, and SIMPLE IRAs and rollovers from qualified retirement plans to a Roth IRA (see instructions) Amount subject to tax in 2010. Check the box if you elect to

- 28. report the entire taxable amount in 2010 rather than reporting 1/2 of it in 2011 and 1/2 of it in 2012. Generally, you must check this box if you checked the box on line 19 (see page x of the instructions) 24 25 Taxable amount. Subtract line 24 from line 23. If more than zero, also include this amount on Form 1040, line 15b; Form 1040A, line 11b; or Form 1040NR, line 16b 25 Sign Here Only If You Are Filing This Form by Itself and Not With Your Tax Return Under penalties of perjury, I declare that I have examined this form, including accompanying attachments, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. ▲ Your signature ▲ Date Paid Preparer Use Only Preparer’s signature Date Check if self-employed Form 8606 (2013) f1_01_0_: f1_02_0_: f1_05_0_: f1_06_0_: f1_07_0_: f1_08_0_: f1_73_0_: f1_301_0_: f1_09_0_: f1_10_0_: f1_11_0_: f1_12_0_: f1_13_0_: f1_14_0_: f1_15_0_: f1_16_0_: f1_17_0_: f1_18_0_: f1_19_0_: f1_20_0_: f1_21_0_: f1_22_0_: f1_23_0_: f1_24_0_: f1_25_0_: f1_41_0_: f1_26_0_: f1_27_0_: f1_28_0_: f1_29_0_: f1_30_0_: f1_31_0_: f1_32_0_: f1_33_0_: f1_34_0_: f1_35: f1_36: f1_44_0_: f1_45_0_: f1_46_0_: f1_47_0_: f1_42_0_: f1_43_0_: f2_001: f2_002: f2_003: f2_004: f2_005: f2_006: f2_007: f2_008: f2_009: f2_010: f2_011: f2_012:

- 29. f2_013: f2_014: f2_061: c2_001: f2_062: f2_063: f2_065: f2_064: f2_066: SCHEDULE E (Form 1040) Department of the Treasury Internal Revenue Service (99) Supplemental Income and Loss (From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) ▶ Attach to Form 1040, 1040NR, or Form 1041. ▶ Information about Schedule E and its separate instructions is at www.irs.gov/schedulee. OMB No. 1545-0074 2013 Attachment Sequence No. 13 Name(s) shown on return Your social security number Part I Income or Loss From Rental Real Estate and Royalties Note. If you are in the business of renting personal property, use Schedule C or C-EZ (see instructions). If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40. A Did you make any payments in 2013 that would require you to file Form(s) 1099? (see instructions) Yes No

- 30. B If “Yes,” did you or will you file required Forms 1099? Yes No 1a Physical address of each property (street, city, state, ZIP code) A B C 1b Type of Property (from list below) A B C 2 For each rental real estate property listed above, report the number of fair rental and personal use days. Check the QJV box only if you meet the requirements to file as a qualified joint venture. See instructions. Fair Rental Days Personal Use Days QJV A B C Type of Property: 1 Single Family Residence 2 Multi-Family Residence

- 31. 3 Vacation/Short-Term Rental 4 Commercial 5 Land 6 Royalties 7 Self-Rental 8 Other (describe) Income: Properties: A B C 3 Rents received . . . . . . . . . . . . . 3 4 Royalties received . . . . . . . . . . . . 4 Expenses: 5 Advertising . . . . . . . . . . . . . . 5 6 Auto and travel (see instructions) . . . . . . . 6 7 Cleaning and maintenance . . . . . . . . . 7 8 Commissions. . . . . . . . . . . . . . 8 9 Insurance . . . . . . . . . . . . . . . 9 10 Legal and other professional fees . . . . . . . 10 11 Management fees . . . . . . . . . . . . 11 12 Mortgage interest paid to banks, etc. (see instructions) 12 13 Other interest. . . . . . . . . . . . . . 13 14 Repairs. . . . . . . . . . . . . . . . 14 15 Supplies . . . . . . . . . . . . . . . 15 16 Taxes . . . . . . . . . . . . . . . . 16 17 Utilities . . . . . . . . . . . . . . . . 17 18 Depreciation expense or depletion . . . . . . . 18 19 Other (list) ▶ 19 20 Total expenses. Add lines 5 through 19 . . . . . 20 21 Subtract line 20 from line 3 (rents) and/or 4 (royalties). If result is a (loss), see instructions to find out if you must

- 32. file Form 6198 . . . . . . . . . . . . . 21 22 Deductible rental real estate loss after limitation, if any, on Form 8582 (see instructions) . . . . . . . 22 ( ) ( ) ( ) 23a Total of all amounts reported on line 3 for all rental properties . . . . 23a b Total of all amounts reported on line 4 for all royalty properties . . . . 23b c Total of all amounts reported on line 12 for all properties . . . . . . 23c d Total of all amounts reported on line 18 for all properties . . . . . . 23d e Total of all amounts reported on line 20 for all properties . . . . . . 23e 24 Income. Add positive amounts shown on line 21. Do not include any losses . . . . . . . 24 25 Losses. Add royalty losses from line 21 and rental real estate losses from line 22. Enter total losses here 25 ( ) 26 Total rental real estate and royalty income or (loss). Combine lines 24 and 25. Enter the result here. If Parts II, III, IV, and line 40 on page 2 do not apply to you, also enter this amount on Form 1040, line 17, or Form 1040NR, line 18. Otherwise, include this amount in the total on line 41 on page 2 . . . . 26 For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11344L Schedule E (Form 1040) 2013 Schedule E (Form 1040) 2013 Attachment Sequence No. 13 Page 2 Name(s) shown on return. Do not enter name and social security

- 33. number if shown on other side. Your social security number Caution. The IRS compares amounts reported on your tax return with amounts shown on Schedule(s) K-1. Part II Income or Loss From Partnerships and S Corporations Note. If you report a loss from an at-risk activity for which any amount is not at risk, you must check the box in column (e) on line 28 and attach Form 6198. See instructions. 27 Are you reporting any loss not allowed in a prior year due to the at-risk, excess farm loss, or basis limitations, a prior year unallowed loss from a passive activity (if that loss was not reported on Form 8582), or unreimbursed partnership expenses? If you answered “Yes,” see instructions before completing this section. Yes No 28 (a) Name (b) Enter P for partnership; S for S corporation (c) Check if foreign partnership (d) Employer identification number (e) Check if any amount is

- 34. not at risk A B C D Passive Income and Loss Nonpassive Income and Loss (f) Passive loss allowed (attach Form 8582 if required) (g) Passive income from Schedule K–1 (h) Nonpassive loss from Schedule K–1 (i) Section 179 expense deduction from Form 4562 (j) Nonpassive income from Schedule K–1 29a Totals b Totals 30 Add columns (g) and (j) of line 29a . . . . . . . . . . . . . . . . . . . . . 30 31 Add columns (f), (h), and (i) of line 29b . . . . . . . . . . . . . . . . . . . 31 ( ) 32 Total partnership and S corporation income or (loss). Combine lines 30 and 31. Enter the result here and include in the total on line 41 below . . . . . . . . . . . . . . . 32

- 35. Part III Income or Loss From Estates and Trusts 33 (a) Name (b) Employer identification number A B Passive Income and Loss Nonpassive Income and Loss (c) Passive deduction or loss allowed (attach Form 8582 if required) (d) Passive income from Schedule K–1 (e) Deduction or loss from Schedule K–1 (f) Other income from Schedule K–1 34a Totals b Totals 35 Add columns (d) and (f) of line 34a . . . . . . . . . . . . . . . . . . . . . 35 36 Add columns (c) and (e) of line 34b . . . . . . . . . . . . . . . . . . . . 36 ( ) 37 Total estate and trust income or (loss). Combine lines 35 and 36. Enter the result here and include in the total on line 41 below . . . . . . . . . . . . . . . . . . . . 37 Part IV Income or Loss From Real Estate Mortgage Investment

- 36. Conduits (REMICs)—Residual Holder 38 (a) Name (b) Employer identification number (c) Excess inclusion from Schedules Q, line 2c (see instructions) (d) Taxable income (net loss) from Schedules Q, line 1b (e) Income from Schedules Q, line 3b 39 Combine columns (d) and (e) only. Enter the result here and include in the total on line 41 below 39 Part V Summary 40 Net farm rental income or (loss) from Form 4835. Also, complete line 42 below . . . . . . 40 41 Total income or (loss). Combine lines 26, 32, 37, 39, and 40. Enter the result here and on Form 1040, line 17, or Form 1040NR, line 18 ▶ 41 42 Reconciliation of farming and fishing income. Enter your gross farming and fishing income reported on Form 4835, line 7; Schedule K-1 (Form 1065), box 14, code B; Schedule K-1 (Form 1120S), box 17, code V; and Schedule K-1 (Form 1041), box 14, code F (see instructions) . . 42 43 Reconciliation for real estate professionals. If you were a real estate professional (see instructions), enter the net income or (loss) you reported

- 37. anywhere on Form 1040 or Form 1040NR from all rental real estate activities in which you materially participated under the passive activity loss rules . . 43 Schedule E (Form 1040) 2013 A B C D A B Version A, Cycle 7 Internal Use Only DRAFT AS OF September 12, 2013 2013 Form 1040 (Schedule E) SE:W:CAR:MP Supplemental Income and Loss SCHEDULE E (Form 1040) Department of the Treasury Internal Revenue Service (99) Supplemental Income and Loss (From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) ▶ Attach to Form 1040, 1040NR, or Form 1041. ▶ Information about Schedule E and its separate instructions is at www.irs.gov/schedulee. OMB No. 1545-0074

- 38. 2013 2013. Catalog number 11344L Attachment Sequence No. 13 Attachment Sequence Number 13. For Paperwork Reduction Act Notice, see your tax return instructions. Part I Income or Loss From Rental Real Estate and Royalties Note. If you are in the business of renting personal property, use Schedule C or C-EZ (see instructions). If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40. A Did you make any payments in 2013 that would require you to file Form(s) 1099? (see instructions) B If “Yes,” did you or will you file required Forms 1099? 1a Physical address of each property (street, city, state, ZIP code) A B C 1b Type of Property (from list below) A B C 2 For each rental real estate property listed above, report the number of fair rental and personal use days. Check the QJV box only if you meet the requirements to file as a qualified joint venture. See instructions. Fair Rental Days Personal Use Days QJV

- 39. A B C Type of Property: 1 Single Family Residence 2 Multi-Family Residence 3 Vacation/Short-Term Rental 4 Commercial 5 Land 6 Royalties 7 Self-Rental Income: Properties: A B C Income: Property A. Property A. Property B. Property B. Property C. Property C. 3 Rents received 3 4 Royalties received 4 Expenses: Expenses: Properties. A.

- 40. Properties. A. Properties. B. Properties. B. Properties. C. 5 Advertising 5 6 Auto and travel (see instructions) 6 7 Cleaning and maintenance 7 8 Commissions 8 9 Insurance 9 10 Legal and other professional fees 10 11 Management fees 11 12 Mortgage interest paid to banks, etc. (see instructions) 12 13 Other interest 13 14

- 41. Repairs 14 15 Supplies 15 16 Taxes 16 17 Utilities 17 18 Depreciation expense or depletion 18 19 19 20 Total expenses. Add lines 5 through 19 20 21 Subtract line 20 from line 3 (rents) and/or 4 (royalties). If result is a (loss), see instructions to find out if you must file Form 6198 21 22 Deductible rental real estate loss after limitation, if any, on Form 8582 (see instructions) 22 23 a Total of all amounts reported on line 3 for all rental properties 23a b Total of all amounts reported on line 4 for all royalty properties

- 42. 23b c Total of all amounts reported on line 12 for all properties 23c d Total of all amounts reported on line 18 for all properties 23d e Total of all amounts reported on line 20 for all properties 23e 24 Income. Add positive amounts shown on line 21. Do not include any losses 24 25 Losses. Add royalty losses from line 21 and rental real estate losses from line 22. Enter total losses here 25 26 Total rental real estate and royalty income or (loss). Combine lines 24 and 25. Enter the result here. If Parts II, III, IV, and line 40 on page 2 do not apply to you, also enter this amount on Form 1040, line 17, or Form 1040NR, line 18. Otherwise, include this amount in the total on line 41 on page 2 26 For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11344L Schedule E (Form 1040) 2013 Schedule E (Form 1040) 2013 Attachment Sequence No. 13 Page 2 Caution. The IRS compares amounts reported on your tax return with amounts shown on Schedule(s) K-1. Part II Income or Loss From Partnerships and S Corporations Note.

- 43. If you report a loss from an at-risk activity for which any amount is not at risk, you must check the box in column (e) on line 28 and attach Form 6198. See instructions. 27 Are you reporting any loss not allowed in a prior year due to the at-risk, excess farm loss, or basis limitations, a prior year unallowed loss from a passive activity (if that loss was not reported on Form 8582), or unreimbursed partnership expenses? If you answered “Yes,” see instructions before completing this section. 28 (a) Name (b) Enter P for partnership; S for S corporation (c) Check if foreign partnership (d) Employer identification number (e) Check if any amount is not at risk A B C D Passive Income and Loss Nonpassive Income and Loss (f) Passive loss allowed (attach Form 8582 if required) (g) Passive income from Schedule K–1 (h) Nonpassive loss from Schedule K–1 (i) Section 179 expense deduction from Form 4562 (j) Nonpassive income

- 44. from Schedule K–1 29 a Totals b Totals 30 Add columns (g) and (j) of line 29a 30 31 Add columns (f), (h), and (i) of line 29b 31 32 Total partnership and S corporation income or (loss). Combine lines 30 and 31. Enter the result here and include in the total on line 41 below 32 Part III Income or Loss From Estates and Trusts 33 (a) Name (b) Employer identification number A B Passive Income and Loss Nonpassive Income and Loss (c) Passive deduction or loss allowed (attach Form 8582 if required) (d) Passive income from Schedule K–1 (e) Deduction or loss from Schedule K–1 (f) Other income from Schedule K–1 34

- 45. a Totals b Totals 35 Add columns (d) and (f) of line 34a 35 36 Add columns (c) and (e) of line 34b 36 37 Total estate and trust income or (loss). Combine lines 35 and 36. Enter the result here and include in the total on line 41 below 37 Part IV Income or Loss From Real Estate Mortgage Investment Conduits (REMICs)—Residual Holder 38 (a) Name (b) Employer identification number (c) Excess inclusion from Schedules Q, line 2c (see instructions) (d) Taxable income (net loss) from Schedules Q, line 1b (e) Income from Schedules Q, line 3b 39 Combine columns (d) and (e) only. Enter the result here and include in the total on line 41 below 39 Part V Summary 40 Net farm rental income or (loss) from Form 4835. Also, complete line 42 below 40

- 46. 41 Total income or (loss). Combine lines 26, 32, 37, 39, and 40. Enter the result here and on Form 1040, line 17, or Form 1040NR, line 18 ▶ 41 42 Reconciliation of farming and fishing income. Enter your gross farming and fishing income reported on Form 4835, line 7; Schedule K-1 (Form 1065), box 14, code B; Schedule K-1 (Form 1120S), box 17, code V; and Schedule K-1 (Form 1041), box 14, code F (see instructions) 42 43 Reconciliation for real estate professionals. If you were a real estate professional (see instructions), enter the net income or (loss) you reported anywhere on Form 1040 or Form 1040NR from all rental real estate activities in which you materially participated under the passive activity loss rules 43 Schedule E (Form 1040) 2013 (f) Passive loss allowed (attach Form 8582 if required) (f) Passive loss allowed (attach Form 8582 if required) (g) Passive income from Schedule K–1 (g) Passive income from Schedule K–1 h) Nonpassive loss from Schedule K–1 h) Nonpassive loss from Schedule K–1 (i) Section 179 expense deduction from Form 4562 (i) Section 179 expense deduction from Form 4562

- 47. (j) Nonpassive income from Schedule K–1 (j) Nonpassive income from Schedule K–1 A B C D (c) Passive deduction or loss allowed (attach Form 8582 if required) (c) Passive deduction or loss allowed (attach Form 8582 if required) (d) Passive income from Schedule K–1 (d) Passive income from Schedule K–1 (e) Deduction or loss from Schedule K–1 (e) Deduction or loss from Schedule K–1 (f) Other income from Schedule K–1 (f) Other income from Schedule K–1 A B (a) Name (b) Employer identification number (c) Excess inclusion from Schedules Q, line 2c (see instructions) (c) Excess inclusion from Schedules Q, line 2c (see instructions) (d) Taxable income (net loss) from Schedules Q, line 1b (d) Taxable income (net loss) from Schedules Q, line 1b (e) Income from Schedules Q, line 3b

- 48. (e) Income from Schedules Q, line 3b p1-t1: p1-t2: c1_01: c1_03: p1-t5: p1-t7: p1-t9: p1-t52: p1-t72: p1-t92: p1-cb5: p1-cb6: c1_02_0_: p1-cb8: p1-cb9: p1-cb11: p1-cb12: p1-t515: p1-t11: p1-t12: p1-t13: p1-t14: p1-t15: p1- t16: p1-t25: p1-t26: p1-t27: p1-t28: p1-t29: p1-t30: p1-t516: p1- t517: p1-t518: p1-t519: p1-t600: p1-t32: p1-t33: p1-t34: p1-t35: p1-t36: p1-t601: p1-t38: p1-t39: p1-t40: p1-t41: p1-t42: p1- t602: p1-t44: p1-t45: p1-t46: p1-t47: p1-t48: p1-t603: p1-t50: p1-t51: p1-t53: p1-t54: p1-t604: p1-t56: p1-t57: p1-t58: p1-t59: p1-t60: p1-t605: p1-t62: p1-t63: p1-t64: p1-t65: p1-t66: p1- t606: p1-t68: p1-t69: p1-t70: p1-t71: p1-t607: p1-t74: p1-t77: p1-t78: p1-t79: p1-t80: p1-t608: p1-t82: p1-t83: p1-t84: p1-t85: p1-t86: p1-t609: p1-t88: p1-t89: p1-t90: p1-t91: p1-t610: p1- t94: p1-t95: p1-t96: p1-t97: p1-t98: p1-t611: p1-t100: p1-t101: p1-t102: p1-t103: p1-t104: p1-t612: p1-t106: p1-t150: p1-t151: p1-t152: p1-t153: p1-t613: p1-t155: p1-t107: p1-t510: p1-t109: p1-t110: p1-t111: p1-t614: p1-t113: p1-t158: p1-t159: p1-t160: p1-t161: p1-t615: p1-t163: p1-t164: p1-t165: p1-t166: p1-t167: p1-t616: p1-t169: p1-t170: p1-t171: p1-t172: p1-t173: p1-t617: p1-t175: p1-t505: p1-t504: p1-t176: p1-t177: p1-t508: p1-t509: p1-t511: p1-t512: p1-t513: p1-t507: p1-t506: p1-t178: p1-t179: p1-t180: p1-t181: p2-t2: p2-cb1: p2-t5: p2-t6: p2-cb3: p2-t7: p2-cb4: p2-t8: p2-t9: p2-cb7: p2-t10: p2-cb6: p2-t11: p2-t12: p2-cb5: p2-t13: p2-cb8: p2-t14: p2-t15: p2-cb9: p2-t16: p2- cb10: p2-t57: p2-t58: p2-t59: p2-t60: p2-t61: p2-t62: p2-t63: p2-t64: p2-t65: p2-t66: p2-t67: p2-t68: p2-t69: p2-t70: p2-t71: p2-t72: p2-t73: p2-t74: p2-t75: p2-t76: p2-t93: p2-t94: p2-t95: p2-t96: p2-t97: p2-t98: p2-t99: p2-t100: p2-t101: p2-t102: p2- t103: p2-t104: p2-t105: p2-t106: p2-t115: p2-t116: p2-t117: p2- t118: p2-t119: p2-t120: p2-t121: p2-t122: p2-t123: p2-t124: p2- t17: p2-t18: p2-t19: p2-t20: p2-t21: p2-t22: p2-t23: p2-t24: p2- t25: p2-t26: p2-t27: p2-t28: p2-t29: p2-t30: p2-t31: p2-t32: p2- t33: p2-t34: p2-t35: p2-t36: p2-t37: p2-t38: p2-t39: p2-t40: p2- t41: p2-t42: p2-t43: p2-t44: p2-t45: p2-t46: p2-t47: p2-t48: p2- t49: p2-t50: p2-t51: p2-t52: p2-t53: p2-t54: p2-t55: p2-t56: p2-

- 49. t77: p2-t78: p2-t79: p2-t80: p2-t81: p2-t82: p2-t83: p2-t84: p2- t85: p2-t86: p2-t87: p2-t88: p2-t89: p2-t90: p2-t91: p2-t92: p2- t107: p2-t108: p2-t109: p2-t110: p2-t111: p2-t112: p2-t113: p2- t114: See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. SCHEDULE D (Form 1040) Department of the Treasury Internal Revenue Service (99) Capital Gains and Losses ▶ Attach to Form 1040 or Form 1040NR. ▶ Information about Schedule D and its separate instructions is at www.irs.gov/scheduled. ▶ Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10. OMB No. 1545-0074 2013 Attachment Sequence No. 12

- 50. Name(s) shown on return Your social security number Part I Short-Term Capital Gains and Losses—Assets Held One Year or Less (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part I, line 2, column (g) (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) 1a Totals for all short-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 1b .

- 51. 1b Totals for all transactions reported on Form(s) 8949 with Box A checked . . . . . . . . . . . . . 2 Totals for all transactions reported on Form(s) 8949 with Box B checked . . . . . . . . . . . . . 3 Totals for all transactions reported on Form(s) 8949 with Box C checked . . . . . . . . . . . . . 4 Short-term gain from Form 6252 and short-term gain or (loss) from Forms 4684, 6781, and 8824 . 4 5 Net short-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 6 Short-term capital loss carryover. Enter the amount, if any, from line 8 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 6 ( ) 7 Net short-term capital gain or (loss). Combine lines 1a through 6 in column (h). If you have any long- term capital gains or losses, go to Part II below. Otherwise, go

- 52. to Part III on the back . . . . . 7 Part II Long-Term Capital Gains and Losses—Assets Held More Than One Year (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part II, line 2, column (g) (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) 8a Totals for all long-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 8b .

- 53. 8b Totals for all transactions reported on Form(s) 8949 with Box D checked . . . . . . . . . . . . . 9 Totals for all transactions reported on Form(s) 8949 with Box E checked . . . . . . . . . . . . . 10 Totals for all transactions reported on Form(s) 8949 with Box F checked . . . . . . . . . . . . . . 11 Gain from Form 4797, Part I; long-term gain from Forms 2439 and 6252; and long-term gain or (loss) from Forms 4684, 6781, and 8824 . . . . . . . . . . . . . . . . . . . . . . 11 12 Net long-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 12 13 Capital gain distributions. See the instructions . . . . . . . . . . . . . . . . . . 13 14 Long-term capital loss carryover. Enter the amount, if any, from line 13 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 14 ( )

- 54. 15 Net long-term capital gain or (loss). Combine lines 8a through 14 in column (h). Then go to Part III on the back . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11338H Schedule D (Form 1040) 2013 Schedule D (Form 1040) 2013 Page 2 Part III Summary 16 Combine lines 7 and 15 and enter the result . . . . . . . . . . . . . . . . . . 16 • If line 16 is a gain, enter the amount from line 16 on Form 1040, line 13, or Form 1040NR, line 14. Then go to line 17 below. • If line 16 is a loss, skip lines 17 through 20 below. Then go to line 21. Also be sure to complete line 22. • If line 16 is zero, skip lines 17 through 21 below and enter -0- on Form 1040, line 13, or Form 1040NR, line 14. Then go to line 22. 17 Are lines 15 and 16 both gains? Yes. Go to line 18. No. Skip lines 18 through 21, and go to line 22. 18 Enter the amount, if any, from line 7 of the 28% Rate Gain

- 55. Worksheet in the instructions . . ▶ 18 19 Enter the amount, if any, from line 18 of the Unrecaptured Section 1250 Gain Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ 19 20 Are lines 18 and 19 both zero or blank? Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Form 1040, line 44 (or in the instructions for Form 1040NR, line 42). Do not complete lines 21 and 22 below. No. Complete the Schedule D Tax Worksheet in the instructions. Do not complete lines 21 and 22 below. 21 If line 16 is a loss, enter here and on Form 1040, line 13, or Form 1040NR, line 14, the smaller of: • The loss on line 16 or • ($3,000), or if married filing separately, ($1,500) } . . . . . . . . . . . . . . . 21 ( ) Note. When figuring which amount is smaller, treat both amounts as positive numbers. 22 Do you have qualified dividends on Form 1040, line 9b, or Form 1040NR, line 10b? Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Form 1040, line 44 (or in the instructions for Form 1040NR, line 42).

- 56. No. Complete the rest of Form 1040 or Form 1040NR. Schedule D (Form 1040) 2013 Version A, Cycle 5 Internal Use Only DRAFT AS OF October 17, 2013 2013 Form 1040 (Schedule D) SE:W:CAR:MP Capital Gains and Losses See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. SCHEDULE D (Form 1040) Department of the Treasury Internal Revenue Service (99) Capital Gains and Losses ▶ Attach to Form 1040 or Form 1040NR. ▶ Information about Schedule D and its separate instructions is at www.irs.gov/scheduled. ▶ Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10. OMB No. 1545-0074 2013 2013. Catalog Number 11338H. Attachment Sequence No. 12 Attachment Sequence number 12. For Paperwork Reduction Act

- 57. Notice, see your tax return instructions. Part I Short-Term Capital Gains and Losses—Assets Held One Year or Less (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part I, line 2, column (g) (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) 1a Totals for all short-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 1b Line 1a. Item 1. (b) 1b Totals for all transactions reported on Form(s) 8949 with Box A checked Line 1b. Item 2. (b). 2 Totals for all transactions reported on Form(s) 8949 with Box B checked Line 1. Item 2. (b). 3 Totals for all transactions reported on Form(s) 8949 with Box

- 58. C checked Line 1. Item 3. (b). 4 Short-term gain from Form 6252 and short-term gain or (loss) from Forms 4684, 6781, and 8824 4 5 Net short-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 5 6 Short-term capital loss carryover. Enter the amount, if any, from line 8 of your Capital Loss Carryover Worksheet in the instructions 6 ( ) 7 Net short-term capital gain or (loss). Combine lines 1a through 6 in column (h). If you have any long-term capital gains or losses, go to Part II below. Otherwise, go to Part III on the back 7 Part II Long-Term Capital Gains and Losses—Assets Held More Than One Year (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part II, line 2, column

- 59. (g) (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) 8a Totals for all long-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 8b Line 8a. Item 1. (b). 8b Totals for all transactions reported on Form(s) 8949 with Box D checked Line 1. Item 2. (b). Totals for all transactions reported on Form(s) 8949 with Box D checked. 9 Totals for all transactions reported on Form(s) 8949 with Box E checked Line 1. Item 2. (b). Totals for all transactions reported on Form(s) 8949 with Box E checked. 10 Totals for all transactions reported on Form(s) 8949 with Box F checked Line 1. Item 3. (b). Totals for all transactions reported on Form(s) 8949 with Box F checked. 11 Gain from Form 4797, Part I; long-term gain from Forms 2439 and 6252; and long-term gain or (loss) from Forms 4684, 6781, and 8824 11 12 Net long-term gain or (loss) from partnerships, S corporations,

- 60. estates, and trusts from Schedule(s) K-1 12 13 Capital gain distributions. See the instructions 13 14 Long-term capital loss carryover. Enter the amount, if any, from line 13 of your Capital Loss Carryover Worksheet in the instructions 14 ( ) 15 Net long-term capital gain or (loss). Combine lines 8a through 14 in column (h). Then go to Part III on the back 15 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11338H Schedule D (Form 1040) 2013 Schedule D (Form 1040) 2013 Page 2 Part III Summary 16 Combine lines 7 and 15 and enter the result 16 • If line 16 is a gain, enter the amount from line 16 on Form 1040, line 13, or Form 1040NR, line 14. Then go to line 17 below. • If line 16 is a loss, skip lines 17 through 20 below. Then go to line 21. Also be sure to complete line 22. • If line 16 is zero, skip lines 17 through 21 below and enter -0- on Form 1040, line 13, or Form 1040NR, line 14. Then go to line 22.

- 61. 17 Are lines 15 and 16 both gains? Yes. Go to line 18. No. Skip lines 18 through 21, and go to line 22. 18 Enter the amount, if any, from line 7 of the 28% Rate Gain Worksheet in the instructions ▶ 18 19 Enter the amount, if any, from line 18 of the Unrecaptured Section 1250 Gain Worksheet in the instructions ▶ 19 20 Are lines 18 and 19 both zero or blank? Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Form 1040, line 44 (or in the instructions for Form 1040NR, line 42). Do not complete lines 21 and 22 below. No. Complete the Schedule D Tax Worksheet in the instructions. Do not complete lines 21 and 22 below. 21 If line 16 is a loss, enter here and on Form 1040, line 13, or Form 1040NR, line 14, the smaller of: • The loss on line 16 or • ($3,000), or if married filing separately, ($1,500) } 21 ( ) Note. When figuring which amount is smaller, treat both amounts as positive numbers. 22 Do you have qualified dividends on Form 1040, line 9b, or Form 1040NR, line 10b? Yes. Complete the Qualified Dividends and Capital Gain Tax

- 62. Worksheet in the instructions for Form 1040, line 44 (or in the instructions for Form 1040NR, line 42). No. Complete the rest of Form 1040 or Form 1040NR. Schedule D (Form 1040) 2013 f1_001: f1_002: f1_003: f1_004: f1_005: f1_006: : f1_007: f1_008: f1_009: f1_010: f1_011: f1_012: f1_013: f1_014: f1_015: f1_016: f1_017: f1_018: f1_019: f1_020: f1_021: f1_022: f1_023: f1_024: f1_025: f1_026: f1_027: f1_028: f1_029: f1_030: f1_031: f1_032: f1_033: f1_034: f1_035: f2_001: c2_01_0_: f2_002: f2_003: c2_02_0_: f2_005: c2_03_0_: SCHEDULE C (Form 1040) Department of the Treasury Internal Revenue Service (99) Profit or Loss From Business (Sole Proprietorship) ▶ For information on Schedule C and its instructions, go to www.irs.gov/schedulec. ▶ Attach to Form 1040, 1040NR, or 1041; partnerships generally must file Form 1065. OMB No. 1545-0074 2013 Attachment Sequence No. 09 Name of proprietor Social security number (SSN)

- 63. A Principal business or profession, including product or service (see instructions) B Enter code from instructions ▶ C Business name. If no separate business name, leave blank. D Employer ID number (EIN), (see instr.) E Business address (including suite or room no.) ▶ City, town or post office, state, and ZIP code F Accounting method: (1) Cash (2) Accrual (3) Other (specify) ▶ G Did you “materially participate” in the operation of this business during 2013? If “No,” see instructions for limit on losses . Yes No H If you started or acquired this business during 2013, check here . . . . . . . . . . . . . . . . . ▶ I Did you make any payments in 2013 that would require you to file Form(s) 1099? (see instructions) . . . . . . . . Yes No J If "Yes," did you or will you file required Forms 1099? . . . . . . . . . . . . . . . . . . . . . Yes No Part I Income 1 Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on Form W-2 and the “Statutory employee” box on that form was checked . . . . . . . . . ▶ 1 2 Returns and allowances . . . . . . . . . . . . . . . . . . . . . . . . . 2

- 64. 3 Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . 3 4 Cost of goods sold (from line 42) . . . . . . . . . . . . . . . . . . . . . . 4 5 Gross profit. Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . 5 6 Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . 6 7 Gross income. Add lines 5 and 6 . . . . . . . . . . . . . . . . . . . . . ▶ 7 Part II Expenses Enter expenses for business use of your home only on line 30. 8 Advertising . . . . . 8 9 Car and truck expenses (see instructions) . . . . . 9 10 Commissions and fees . 10 11 Contract labor (see instructions) 11 12 Depletion . . . . . 12 13 Depreciation and section 179 expense deduction (not included in Part III) (see instructions) . . . . . 13

- 65. 14 Employee benefit programs (other than on line 19) . . 14 15 Insurance (other than health) 15 16 Interest: a Mortgage (paid to banks, etc.) 16a b Other . . . . . . 16b 17 Legal and professional services 17 18 Office expense (see instructions) 18 19 Pension and profit-sharing plans . 19 20 Rent or lease (see instructions): a Vehicles, machinery, and equipment 20a b Other business property . . . 20b 21 Repairs and maintenance . . . 21 22 Supplies (not included in Part III) . 22 23 Taxes and licenses . . . . . 23 24 Travel, meals, and entertainment: a Travel . . . . . . . . . 24a

- 66. b Deductible meals and entertainment (see instructions) . 24b 25 Utilities . . . . . . . . 25 26 Wages (less employment credits) . 26 27 a Other expenses (from line 48) . . 27a b Reserved for future use . . . 27b 28 Total expenses before expenses for business use of home. Add lines 8 through 27a . . . . . . ▶ 28 29 Tentative profit or (loss). Subtract line 28 from line 7 . . . . . . . . . . . . . . . . . 29 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method (see instructions). Simplified method filers only: enter the total square footage of: (a) your home: and (b) the part of your home used for business: . Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30 . . . . . . . . . 30 31 Net profit or (loss). Subtract line 30 from line 29. • If a profit, enter on both Form 1040, line 12 (or Form 1040NR, line 13) and on Schedule SE, line 2.

- 67. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. • If a loss, you must go to line 32. } 31 32 If you have a loss, check the box that describes your investment in this activity (see instructions). • If you checked 32a, enter the loss on both Form 1040, line 12, (or Form 1040NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see the line 31 instructions). Estates and trusts, enter on Form 1041, line 3. • If you checked 32b, you must attach Form 6198. Your loss may be limited. } 32a All investment is at risk. 32b Some investment is not at risk. For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11334P Schedule C (Form 1040) 2013 Schedule C (Form 1040) 2013 Page 2 Part III Cost of Goods Sold (see instructions) 33 Method(s) used to value closing inventory: a Cost b Lower of cost or market c Other (attach explanation) 34

- 68. Was there any change in determining quantities, costs, or valuations between opening and closing inventory? If “Yes,” attach explanation . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No 35 Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . 35 36 Purchases less cost of items withdrawn for personal use . . . . . . . . . . . . . . 36 37 Cost of labor. Do not include any amounts paid to yourself . . . . . . . . . . . . . . 37 38 Materials and supplies . . . . . . . . . . . . . . . . . . . . . . . . 38 39 Other costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 40 Add lines 35 through 39 . . . . . . . . . . . . . . . . . . . . . . . . 40 41 Inventory at end of year . . . . . . . . . . . . . . . . . . . . . . . . 41 42 Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 . . . . . . 42 Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562. 43 When did you place your vehicle in service for business purposes? (month, day, year) ▶ / /

- 69. 44 Of the total number of miles you drove your vehicle during 2013, enter the number of miles you used your vehicle for: a Business b Commuting (see instructions) c Other 45 Was your vehicle available for personal use during off-duty hours? . . . . . . . . . . . . . . . Yes No 46 Do you (or your spouse) have another vehicle available for personal use?. . . . . . . . . . . . . . Yes No 47a Do you have evidence to support your deduction? . . . . . . . . . . . . . . . . . . . . Yes No b If “Yes,” is the evidence written? . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Part V Other Expenses. List below business expenses not included on lines 8–26 or line 30. 48 Total other expenses. Enter here and on line 27a . . . . . . . . . . . . . . . . 48 Schedule C (Form 1040) 2013 Version A, Cycle 4 Internal Use Only DRAFT AS OF September 12, 2013 2013 Form 1040 (Schedule C) SE:W:CAR:MP Profit or Loss From Business (Sole Proprietorship) SCHEDULE C (Form 1040) Department of the Treasury Internal Revenue Service (99) Profit or Loss From Business

- 70. (Sole Proprietorship) ▶ For information on Schedule C and its instructions, go to www.irs.gov/schedulec. ▶ Attach to Form 1040, 1040NR, or 1041; partnerships generally must file Form 1065. OMB No. 1545-0074 2013 2013. Catalog number 11334P. Attachment Sequence No. 09 Attachment Sequence number 09. For Paperwork Reduction Act Notice, see the separate instructions. B Enter code from instructions E F Accounting method: (1) (2) (3) G Did you “materially participate” in the operation of this business during 2013? If “No,” see instructions for limit on losses H If you started or acquired this business during 2013, check here ▶ I Did you make any payments in 2013 that would require you to file Form(s) 1099? (see instructions) J If "Yes," did you or will you file required Forms 1099? Part I Income 1 Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on Form W-2 and the

- 71. “Statutory employee” box on that form was checked ▶ 1 2 Returns and allowances 2 3 Subtract line 2 from line 1 3 4 Cost of goods sold (from line 42) 4 5 Gross profit. Subtract line 4 from line 3 5 6 Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) 6 7 Gross income. Add lines 5 and 6 ▶ 7 Part II Expenses Enter expenses for business use of your home only on line 30. 8 Advertising 8 9 Car and truck expenses (see instructions) 9 10 Commissions and fees 10 11

- 72. Contract labor (see instructions) 11 12 Depletion 12 13 Depreciation and section 179 expense deduction (not included in Part III) (see instructions) 13 14 Employee benefit programs (other than on line 19) 14 15 Insurance (other than health) 15 16 Interest: a Mortgage (paid to banks, etc.) 16a b Other 16b 17 Legal and professional services 17 18 Office expense (see instructions) 18 19 Pension and profit-sharing plans 19

- 73. 20 Rent or lease (see instructions): a Vehicles, machinery, and equipment 20a b Other business property 20b 21 Repairs and maintenance 21 22 Supplies (not included in Part III) 22 23 Taxes and licenses 23 24 Travel, meals, and entertainment: a Travel 24a b Deductible meals and entertainment (see instructions) 24b 25 Utilities 25 26 Wages (less employment credits) 26 27 a Other expenses (from line 48)

- 74. 27a b Reserved for future use 27b 28 Total expenses before expenses for business use of home. Add lines 8 through 27a ▶ 28 29 Tentative profit or (loss). Subtract line 28 from line 7 29 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method (see instructions). . Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30 30 31 Net profit or (loss). Subtract line 30 from line 29. • If a profit, enter on both Form 1040, line 12 (or Form 1040NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. • If a loss, you must go to line 32. } 31 32 If you have a loss, check the box that describes your investment in this activity (see instructions). • If you checked 32a, enter the loss on both Form 1040, line 12, (or Form 1040NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see the line 31 instructions). Estates and trusts, enter on Form 1041, line 3. • If you checked 32b, you must attach Form 6198. Your loss

- 75. may be limited. } 32a 32b For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11334P Schedule C (Form 1040) 2013 Schedule C (Form 1040) 2013 Page 2 Part III Cost of Goods Sold (see instructions) 33 Method(s) used to value closing inventory: a b c 34 Was there any change in determining quantities, costs, or valuations between opening and closing inventory? If “Yes,” attach explanation 35 Inventory at beginning of year. If different from last year’s closing inventory, attach explanation 35 36 Purchases less cost of items withdrawn for personal use 36 37 Cost of labor. Do not include any amounts paid to yourself 37 38

- 76. Materials and supplies 38 39 Other costs 39 40 Add lines 35 through 39 40 41 Inventory at end of year 41 42 Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 42 Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562. 43 When did you place your vehicle in service for business purposes? (month, day, year) 44 Of the total number of miles you drove your vehicle during 2013, enter the number of miles you used your vehicle for: a 45 Was your vehicle available for personal use during off-duty hours? 46 Do you (or your spouse) have another vehicle available for personal use? 47 a Do you have evidence to support your deduction?

- 77. b If “Yes,” is the evidence written? Part V Other Expenses. List below business expenses not included on lines 8–26 or line 30. 48 Total other expenses. Enter here and on line 27a 48 Schedule C (Form 1040) 2013 f1_001: f1_002: f1_003: f1_004: f1_005: f1_006: f1_007: f1_008: c1_01: Offf1_009: c1_04: c1_05: 0c1_06: c1_07: c1_08_0_: f1_010: f1_011: f1_018: f1_019: f1_020: f1_021: f1_022: f1_023: f1_024: f1_025: f1_026: f1_027: f1_028: f1_029: f1_030: f1_031: f1_032: f1_033: f1_034: f1_035: f1_036: f1_037: f1_038: f1_039: f1_040: f1_041: f1_042: f1_043: f1_044: f1_045: f1_046: f1_047: f1_048: f1_049: f1_050: f1_051: f1_052: f1_053: f1_054: f1_055: f1_056: f1_057: f1_058: f1_059: f1_060: f1_061: f1_062: f1_063: f1_064: f1_065: f1_066: f1_067: f1_068: f1_069: f1_070: f1_071: f1_072: f1_073: f1_074: f1_075: f1_084: f1_085: f1_076: f1_077: f1_078: f1_079: f1_100: f1_101: f1_080: f1_081: f1_082: f1_083: c1_08: 0c2_01: c2_02: c2_03: c2_04: f2_001: f2_002: f2_003: f2_004: f2_005: f2_006: f2_007: f2_008: f2_009: f2_010: f2_011: f2_012: f2_013: f2_014: f2_015: f2_016: f2_017: f2_018: f2_019: f2_020: f2_021: f2_022: c2_05: c2_06: c2_07: c2_08: f2_023: f2_024: f2_025: f2_026: f2_027: f2_028: f2_029: f2_030: f2_031: f2_032: f2_033: f2_034: f2_035: f2_036: f2_037: f2_038: f2_039: f2_040: f2_041: f2_042: f2_043: f2_044: f2_045: f2_046: f2_047: f2_048: f2_049: f2_050: f2_051: SCHEDULE B (Form 1040A or 1040)

- 78. Department of the Treasury Internal Revenue Service (99) Interest and Ordinary Dividends ▶ Attach to Form 1040A or 1040. ▶ Information about Schedule B (Form 1040A or 1040) and its instructions is at www.irs.gov/scheduleb. OMB No. 1545-0074 2013 Attachment Sequence No. 08 Name(s) shown on return Your social security number Part I Interest (See instructions on back and the instructions for Form 1040A, or Form 1040, line 8a.) Note. If you received a Form 1099-INT, Form 1099-OID, or substitute statement from a brokerage firm, list the firm’s

- 79. name as the payer and enter the total interest shown on that form. 1 List name of payer. If any interest is from a seller-financed mortgage and the buyer used the property as a personal residence, see instructions on back and list this interest first. Also, show that buyer’s social security number and address ▶ 1 Amount 2 Add the amounts on line 1 . . . . . . . . . . . . . . . . . . 2 3 Excludable interest on series EE and I U.S. savings bonds issued after 1989. Attach Form 8815 . . . . . . . . . . . . . . . . . . . . . 3 4 Subtract line 3 from line 2. Enter the result here and on Form 1040A, or Form 1040, line 8a . . . . . . . . . . . . . . . . . . . . . . ▶ 4

- 80. Note. If line 4 is over $1,500, you must complete Part III. Amount Part II Ordinary Dividends (See instructions on back and the instructions for Form 1040A, or Form 1040, line 9a.) Note. If you received a Form 1099-DIV or substitute statement from a brokerage firm, list the firm’s name as the payer and enter the ordinary dividends shown on that form. 5 List name of payer ▶ 5 6 Add the amounts on line 5. Enter the total here and on Form 1040A, or Form

- 81. 1040, line 9a . . . . . . . . . . . . . . . . . . . . . . ▶ 6 Note. If line 6 is over $1,500, you must complete Part III. Part III Foreign Accounts and Trusts (See instructions on back.) You must complete this part if you (a) had over $1,500 of taxable interest or ordinary dividends; (b) had a foreign account; or (c) received a distribution from, or were a grantor of, or a transferor to, a foreign trust. Yes No 7a At any time during 2013, did you have a financial interest in or signature authority over a financial account (such as a bank account, securities account, or brokerage account) located in a foreign country? See instructions . . . . . . . . . . . . . . . . . . . . . . . . If “Yes,” are you required to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR), formerly TD F 90-22.1, to report that financial interest or signature authority? See FinCEN Form 114 and its instructions for filing requirements and exceptions to those requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . b If you are required to file FinCEN Form 114, enter the name of the foreign country where the financial account is located ▶ 8 During 2013, did you receive a distribution from, or were you the grantor of, or transferor to, a

- 82. foreign trust? If “Yes,” you may have to file Form 3520. See instructions on back . . . . . . For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 17146N Schedule B (Form 1040A or 1040) 2013 Schedule B (Form 1040A or 1040) 2013 Page 2 General Instructions Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information about developments related to Schedule B (Form 1040A or 1040) and its instructions, such as legislation enacted after they were published, go to www.irs.gov/scheduleb. Purpose of Form Use Schedule B if any of the following applies. • You had over $1,500 of taxable interest or ordinary dividends. • You received interest from a seller-financed mortgage and the buyer used the property as a personal residence. • You have accrued interest from a bond. • You are reporting original issue discount (OID) in an amount less than the amount shown on Form 1099-OID.

- 83. • You are reducing your interest income on a bond by the amount of amortizable bond premium. • You are claiming the exclusion of interest from series EE or I U.S. savings bonds issued after 1989. • You received interest or ordinary dividends as a nominee. • You had a financial interest in, or signature authority over, a financial account in a foreign country or you received a distribution from, or were a grantor of, or transferor to, a foreign trust. Part III of the schedule has questions about foreign accounts and trusts. Specific Instructions TIP You can list more than one payer on each entry space for lines 1 and 5, but be sure to clearly show the amount paid next to the payer's name. Add the separate amounts paid by the payers listed on an entry space and enter the total in the “Amount” column. If you still need more space, attach separate statements that are the same size as the printed schedule. Use the same format as lines 1 and 5, but show your totals on Schedule B. Be sure to put your name and social security number (SSN) on the statements and attach them at the end of your return. Part I. Interest Line 1. Report on line 1 all of your taxable interest.

- 84. Taxable interest should be shown on your Forms 1099-INT, Forms 1099-OID, or substitute statements. Include interest from series EE, H, HH, and I U.S. savings bonds. List each payer’s name and show the amount. Do not report on this line any tax-exempt interest from box 8 or box 9 of Form 1099-INT. Instead, report the amount from box 8 on line 8b of Form 1040A or 1040. If an amount is shown in box 9 of Form 1099-INT, you generally must report it on line 12 of Form 6251. See the Instructions for Form 6251 for more details. Seller-financed mortgages. If you sold your home or other property and the buyer used the property as a personal residence, list first any interest the buyer paid you on a mortgage or other form of seller financing. Be sure to show the buyer’s name, address, and SSN. You must also let the buyer know your SSN. If you do not show the buyer’s name, address, and SSN, or let the buyer know your SSN, you may have to pay a $50 penalty. Nominees. If you received a Form 1099-INT that includes interest you received as a nominee (that is, in your name, but the interest actually belongs to someone else), report the total on line 1. Do this even if you later distributed some or all of this income to others. Under your last entry on line 1, put a subtotal of all interest listed on line 1. Below this subtotal, enter "Nominee Distribution" and show the total interest you received as a nominee. Subtract this amount from the subtotal and enter the result on line 2. TIP If you received interest as a nominee, you must give the actual owner a Form

- 85. 1099-INT unless the owner is your spouse. You must also file a Form 1096 and a Form 1099-INT with the IRS. For more details, see the General Instructions for Certain Information Returns and the Instructions for Forms 1099-INT and 1099-OID. Accrued interest. When you buy bonds between interest payment dates and pay accrued interest to the seller, this interest is taxable to the seller. If you received a Form 1099 for interest as a purchaser of a bond with accrued interest, follow the rules earlier under Nominees to see how to report the accrued interest. But identify the amount to be subtracted as “Accrued Interest.” Original issue discount (OID). If you are reporting OID in an amount less than the amount shown on Form 1099-OID, follow the rules earlier under Nominees to see how to report the OID. But identify the amount to be subtracted as “OID Adjustment.” Amortizable bond premium. If you are reducing your interest income on a bond by the amount of amortizable bond premium, follow the rules earlier under Nominees to see how to report the interest. But identify the amount to be subtracted as “ABP Adjustment.” Line 3. If, during 2013, you cashed series EE or I U.S. savings bonds issued after 1989 and you paid qualified higher education expenses for yourself, your spouse, or your dependents, you may be able to exclude part or all of the interest on those bonds. See Form 8815 for details.