Downloaded 10 times

![Contact Information: Brian David Butler Miami Campus Facilitator International Economics & Trade (Prof. Grosse) Email: [email_address] Cell: 786-457-0984 Blog: http://blog.globotrends.com/ Wiki: http://kookyplan.pbwiki.com/brianbutler Connect professionally: http://www.linkedin.com/in/briandbutler http://www.linkedin.com/e/gis/69362 Connect personally: http://www.facebook.com/people/Brian_Butler/293500110](https://image.slidesharecdn.com/brianpresentation01-090530163216-phpapp02/75/Brian-Butler-TBird-int-l-finance-class-01-1-2048.jpg)

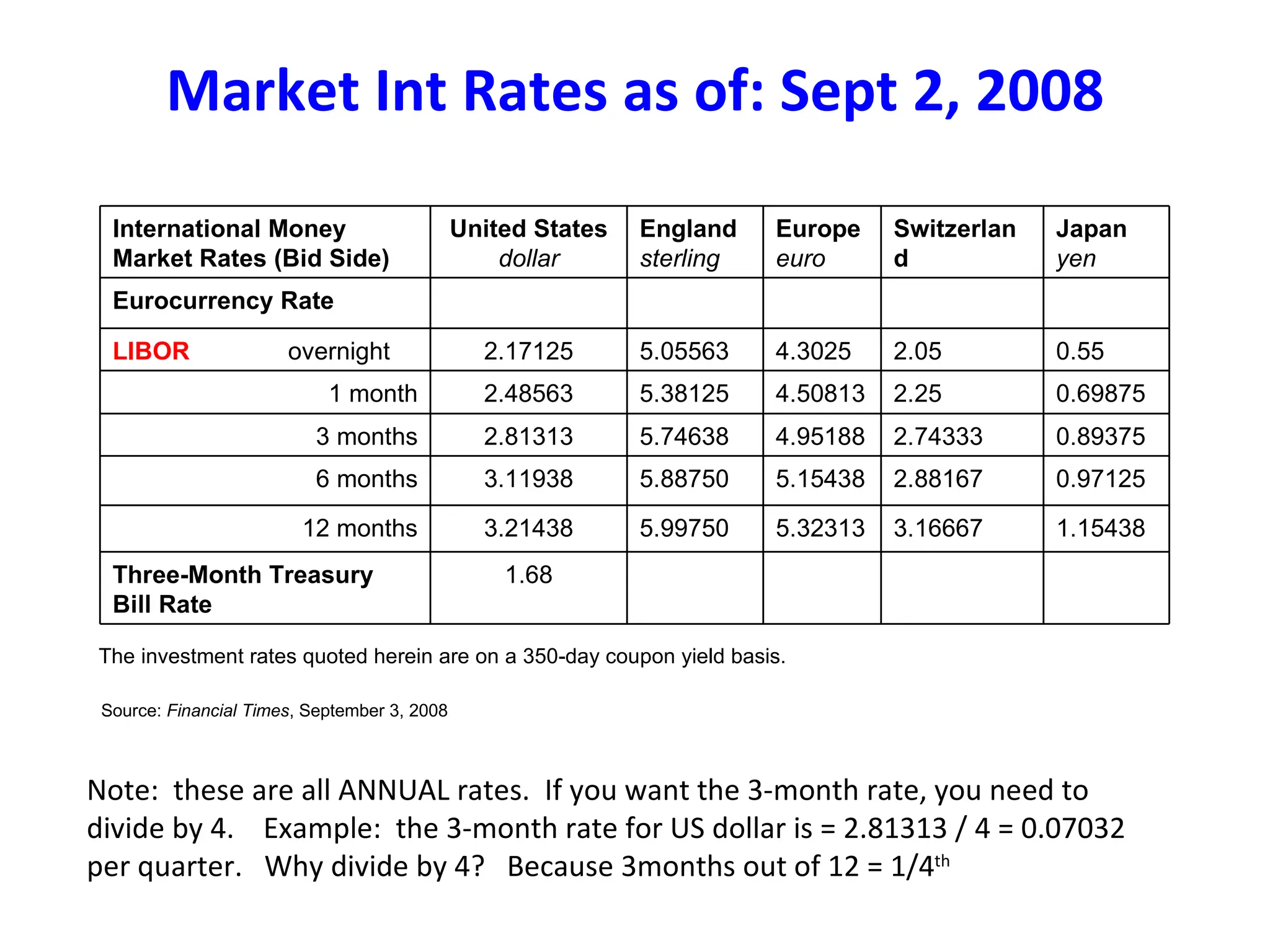

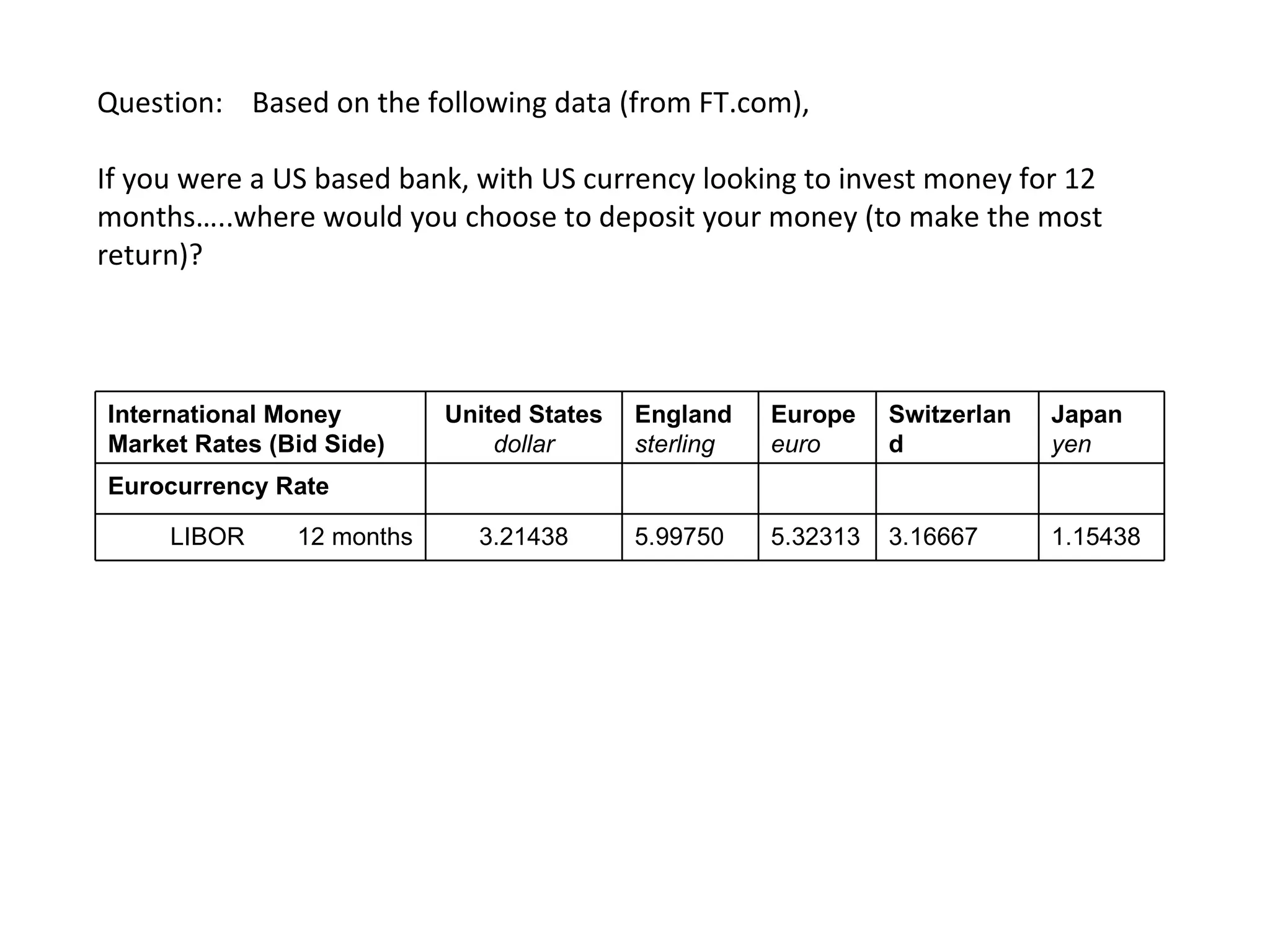

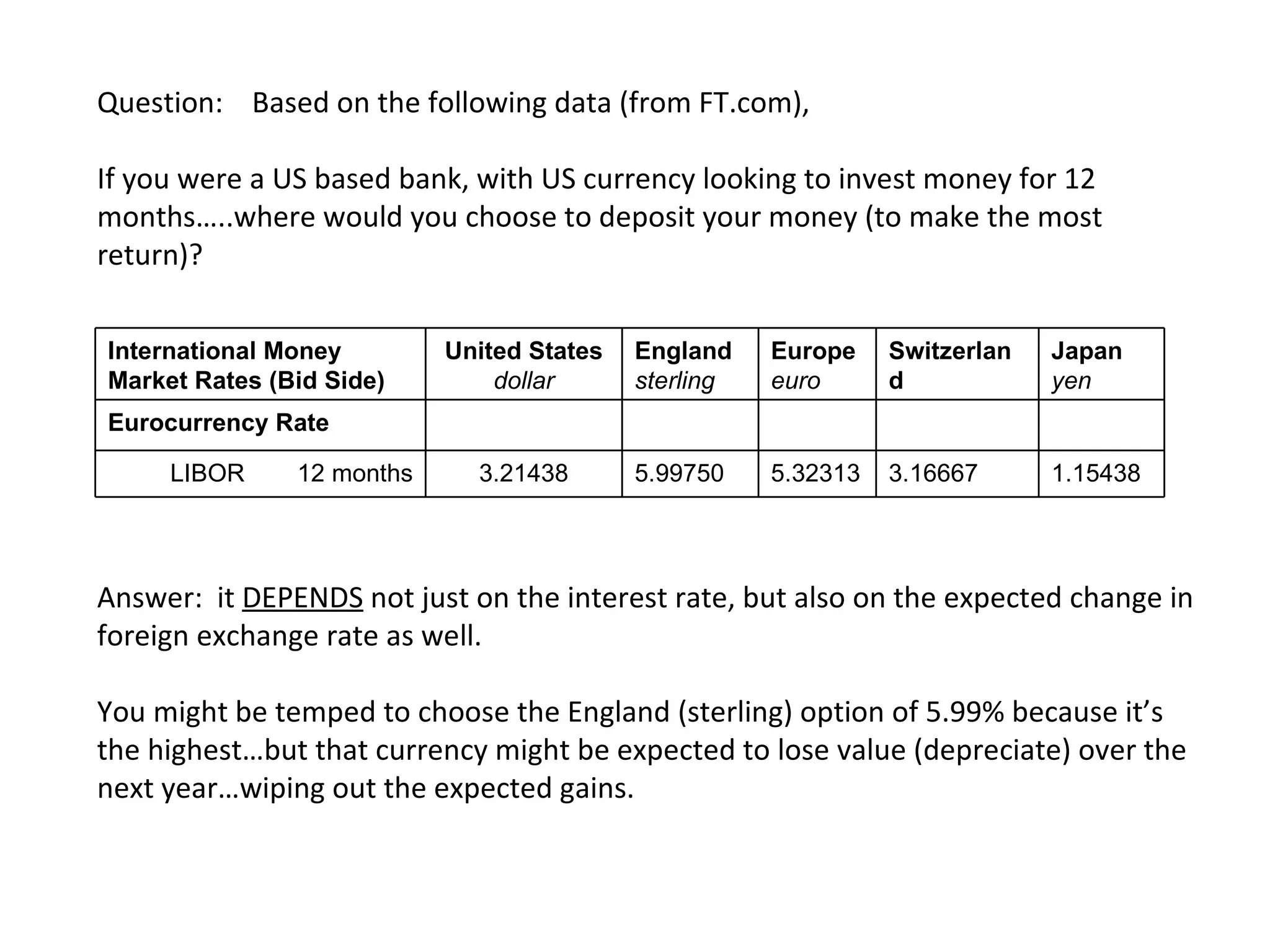

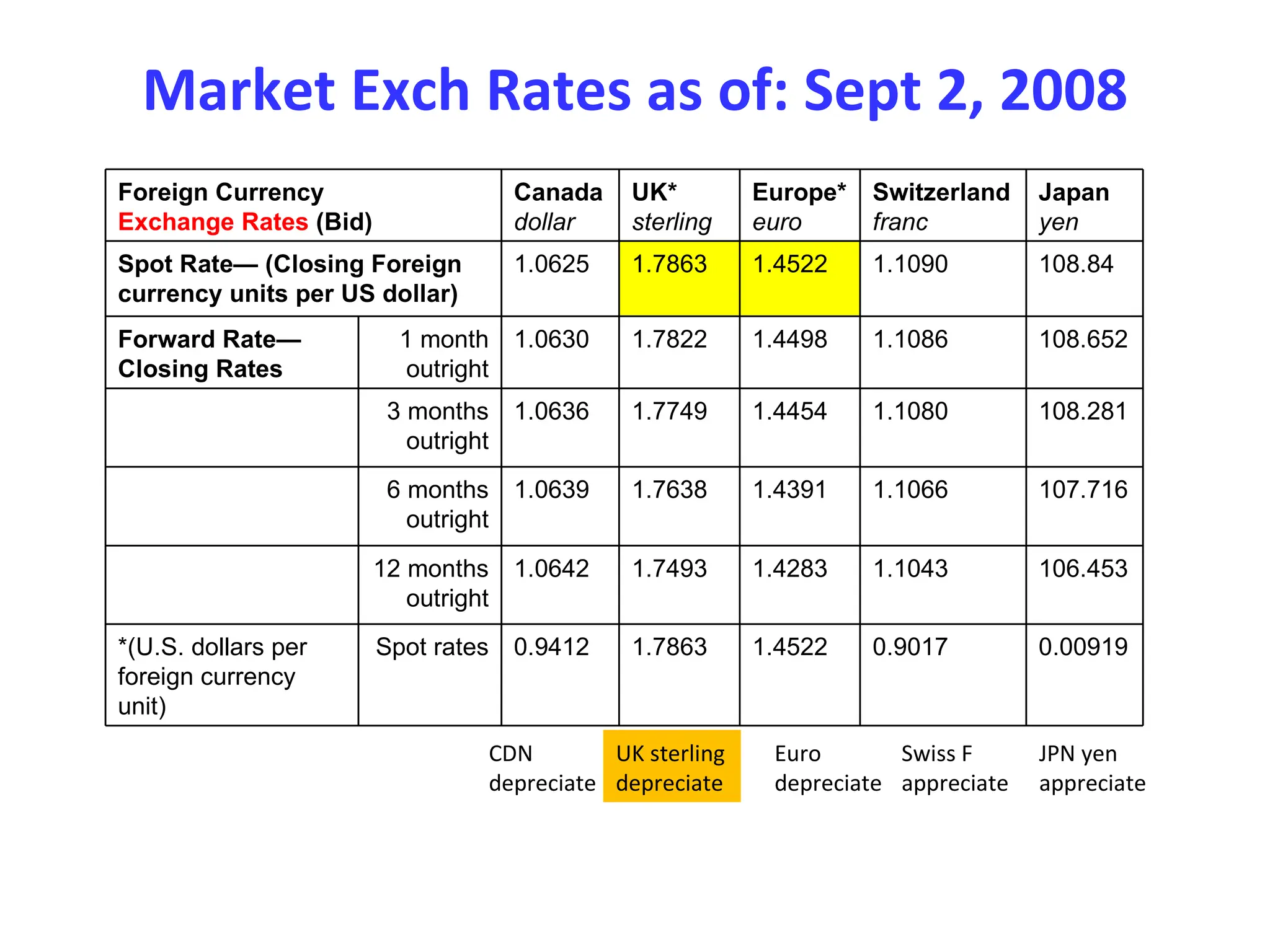

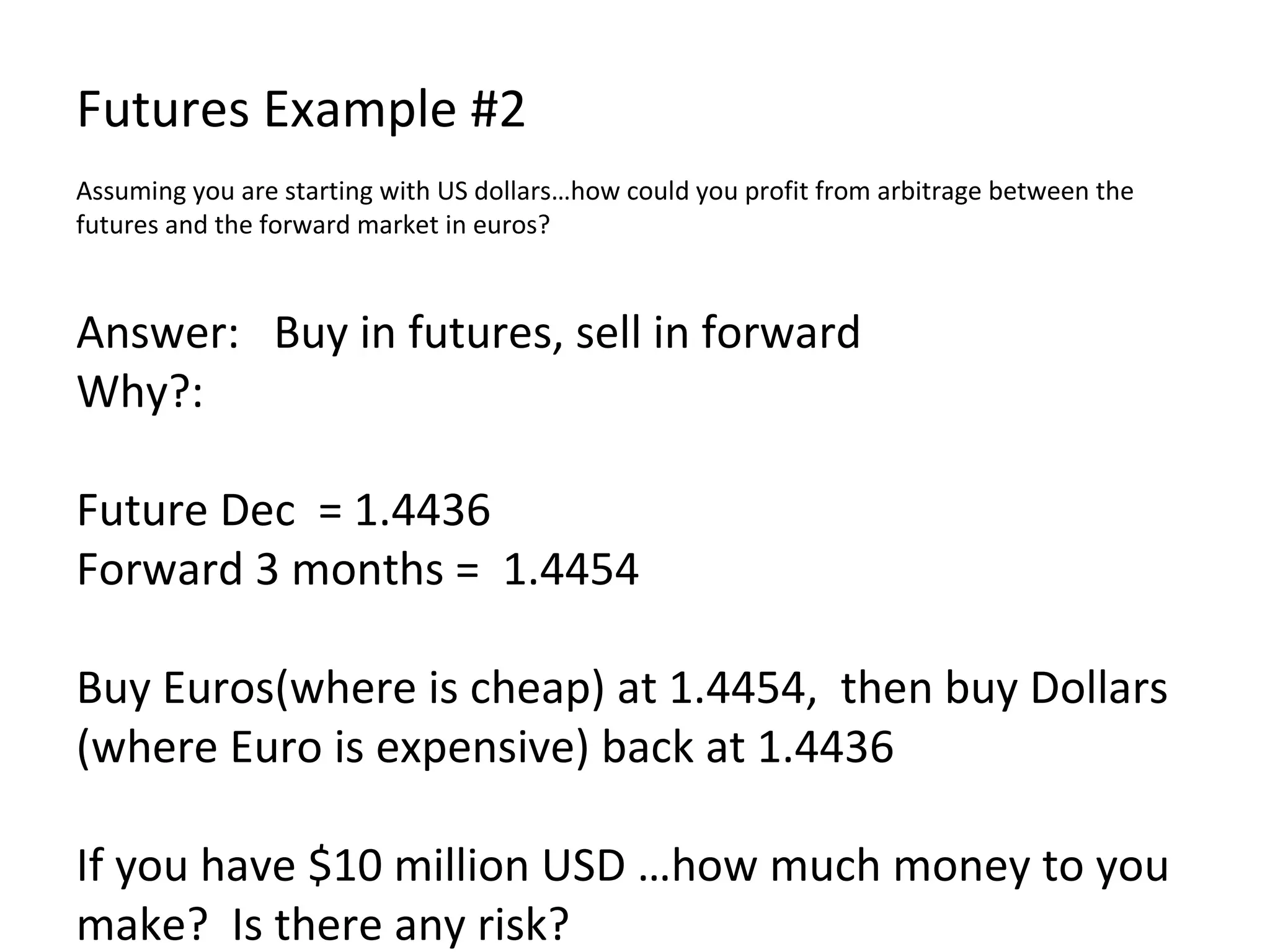

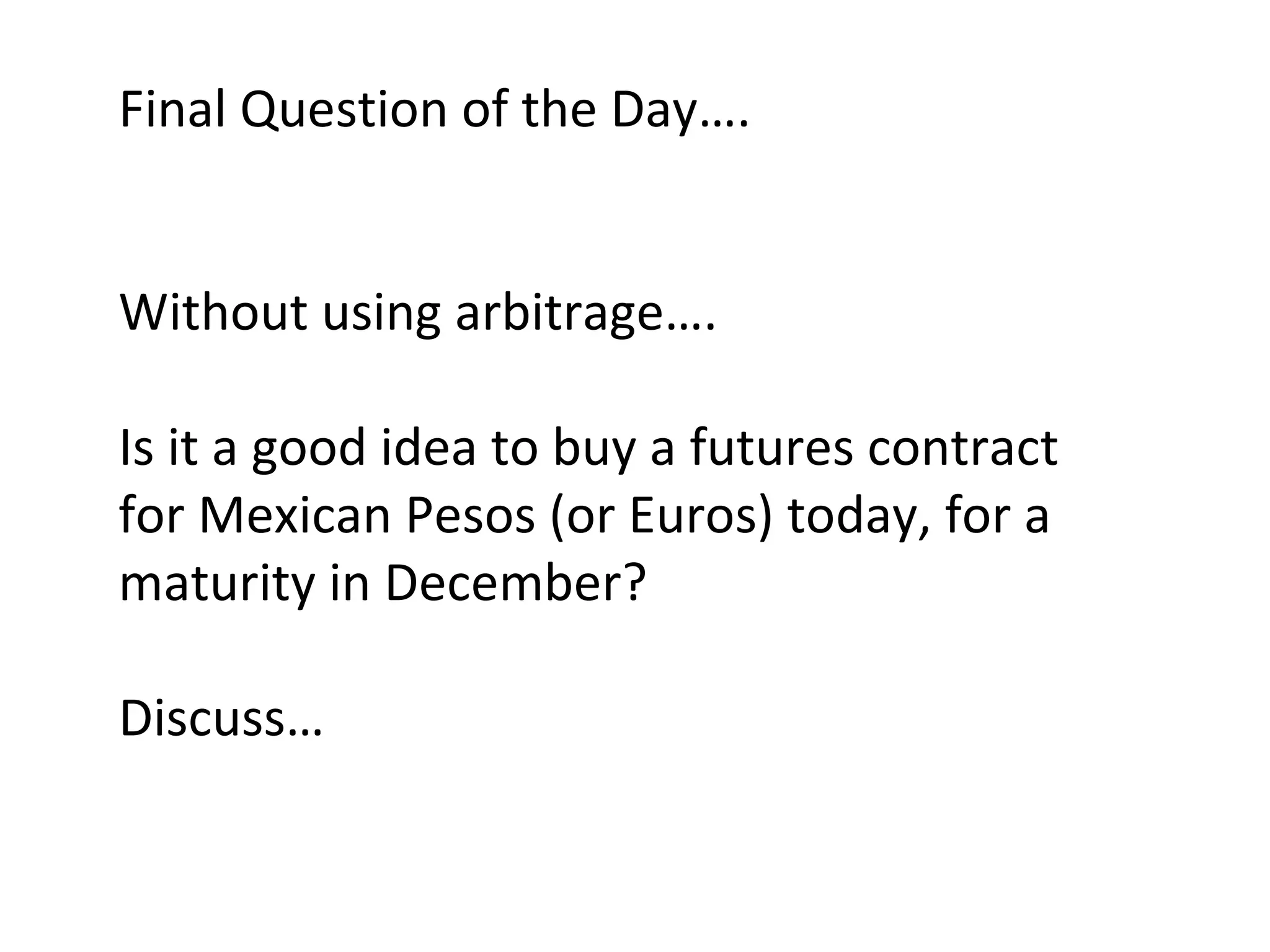

Series of lectures from Brian Butler, given during fall 2008 session at Thunderbird Global MBA, Miami campus: This lecture 01: learn to read FX and interest rate tables & how to make arbitrage decisions to maximize profits or minimize costs