1. The CSU Widget Factory has been experiencing an increase in bac

Economist.4section.20100220

1.

2. Print edition

Politics in America printed lighting

What's gone Printed circuit

wrong in

Washington? private-sector space flight

American politics Moon dreams

seems unusually

bogged down at climate change

present. Blame Green.view: Copenhagen accounting

Barack Obama more than the system

Feb 18th 2010 polar ice shelves

Breaking waves

Leaders computer displays

Hands off

Nigeria's new president

Be focused, be bold the internet

Tech.view: World Wide Wait

Greece and the euro

Leant on recruitment

Science correspondent's job

Competition policy

Prosecutor, judge and jury more recruitment

The Richard Casement internship

Rethinking economics

Radical thoughts on 19th Street

Business&Finance

america's economy

A modest proposal

business in china

Power cut

a european monetary fund?

Economics focus: Disciplinary measures

the euro area’s crisis

Let the Greeks ruin themselves

sovereign-debt worries

Domino theory

competition policy in europe

Unchained watchdog

business and social responsibility

Business.view column: Unlikely heroes

a special report on financial risk

The gods strike back

Science&Technology

printed body parts

Making a bit of me

http://cafe.naver.com/economist365 Page 2 of 59

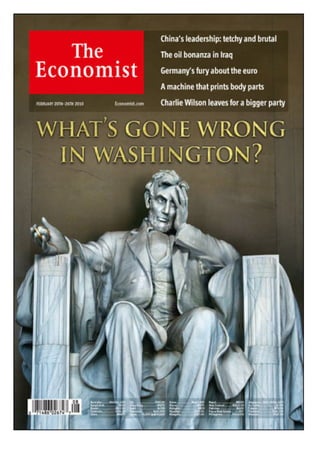

3. Politics in America

What's gone wrong in Washington?

Feb 18th 2010

From The Economist print edition

American politics seems unusually bogged down at present. Blame Barack

Obama more than the system

Derek Bacon

THIS week Evan Bayh, a senator from Indiana who nearly became Barack Obama’s

vice-president, said he was retiring from the Senate, blaming the inability of

Congress to get things done. Cynics think Mr Bayh was also worried about being

beaten in November (though he was ahead in the polls). Yet the idea that America’s

democracy is broken, unable to fix the country’s problems and condemned to

impotent partisan warfare, has gained a lot of support lately (see article).

Certainly the system looks dysfunctional. Although a Democratic president is in the

White House and Democrats control both House and Senate, Mr Obama has been

unable to enact health-care reform, a Democratic goal for many decades. His cap-

and-trade bill to reduce carbon emissions has passed the House but languishes in the

Senate. Now a bill to boost job-creation is stuck there as well. Nor is it just a

question of a governing party failing to get its way. Washington seems incapable of

fixing America’s deeper problems. Democrats and Republicans may disagree about

climate change and health, but nobody thinks that America can ignore the federal

4. deficit, already 10% of GDP and with a generation of baby-boomers just about to

retire. Yet an attempt to set up a bipartisan deficit-reduction commission has recently

collapsed—again.

This, argue the critics, is what happens when a mere 41 senators (in a 100-strong

chamber) can filibuster a bill to death; when states like Wyoming (population:

500,000) have the same clout in the Senate as California (37m), so that senators

representing less than 11% of the population can block bills; when, thanks to

gerrymandering, many congressional seats are immune from competitive elections;

when hateful bloggers and talk-radio hosts shoot down any hint of compromise;

when a tide of lobbying cash corrupts everything. And this dysfunctionality matters

far beyond America’s shores. A few years ago only Chinese bureaucrats dared

suggest that Beijing’s autocratic system of government was superior. Nowadays

there is no shortage of leaders from emerging countries, or even prominent American

businesspeople, who privately sing the praises of a system that can make decisions

swiftly.

It’s alright, Abe

We disagree. Washington has its faults, some of which could easily be fixed. But

much of the current fuss forgets the purpose of American government; and it lets

current politicians (Mr Obama in particular) off the hook.

To begin with, the critics exaggerate their case. It is simply not true to say that

nothing can get through Congress. Look at the current financial crisis. The huge TARP

bill, which set up a fund to save America’s banks, passed, even though it came at the

end of George Bush’s presidency. The stimulus bill, a $787 billion two-year package,

made it through within a month of Mr Obama taking office. The Democrats have also

passed a long list of lesser bills, from investments in green technology to making it

easier for women to sue for sex discrimination.

A criticism with more weight is that American government is good at solving acute

problems (like averting a Depression) but less good at confronting chronic ones (like

the burden of entitlements). Yet even this can be overstated. Mr Bush failed to

reform pensions, but he did push through No Child Left Behind, the biggest change to

schools for a generation. Bill Clinton reformed welfare. The system, in other words,

can work, even if it does not always do so. (That is hardly unusual anywhere: for all

its speed in authorising power stations, China has hardly made a success of health

care lately.) On the biggest worry of all, the budget, it may well take a crisis to force

action, but Americans have wrestled down huge deficits before.

America’s political structure was designed to make legislation at the federal level

difficult, not easy. Its founders believed that a country the size of America is best

governed locally, not nationally. True to this picture, several states have pushed

forward with health-care reform. The Senate, much ridiculed for antique practices

like the filibuster and the cloture vote, was expressly designed as a “cooling”

chamber, where bills might indeed die unless they commanded broad support.

Broad support from the voters is something that both the health bill and the cap-and-

trade bill clearly lack. Democrats could have a health bill tomorrow if the House

6. Nigeria's new president

Be focused, be bold

Feb 18th 2010

From The Economist print edition

Goodluck Jonathan probably has only a short time in office. He could still

make a difference

AFP

ACCORDING to his spokesman, the man who has just become the acting president of

Africa’s most populous country, Goodluck Jonathan, has vowed to “secure Nigeria’s

path to greatness and guarantee our place among the great nations of the world in

the shortest possible time.” That would be a tall order even for a freshly elected

leader with a thumping majority and two terms in office. In fact, the spokesman’s

desperate hyperbole reveals the truth of the matter: Mr Jonathan is taking over the

leadership of one of the world’s least governable countries in the least promising

circumstances.

Some doubt the constitutionality of his succession to Umaru Yar’Adua, who

supposedly still lies gravely ill in a Saudi hospital. And as the presidency rotates

between a northern Muslim and a southern Christian, to satisfy both sides of Nigeria’s

ethnic-religious divide, so Mr Jonathan, a southerner, probably has only a little more

than a year in office before being replaced in the next election. To many of Nigeria’s

ambitious politicians, he is more lame duck than Goodluck.

Given these constraints, Mr Jonathan could be forgiven, perhaps, for just keeping his

head down and the seat warm for his successor. His lacklustre record as vice-

8. Greece and the euro

Leant on

Feb 18th 2010

From The Economist print edition

The euro zone’s rescue plan for Greece is flawed

ON FEBRUARY 15th Greeks celebrated Clean Monday, the start of Orthodox Lent, by

flocking out of towns and cities to eat shellfish and fly kites. For a country in the

throes of an economic crisis, a national holiday to listen to the bouzouki smacks of

self-indulgence. But then Greeks and other members of the euro zone are perhaps

allowing themselves to believe that, after an awful, bickering month, things are

looking up. Fortified by a couple of European Union summits, plus a more ambitious

Greek pledge to cut the deficit and a euro-zone counterpledge to stand behind the

country, the market for Greek government debt looks stable.

But for how long? The bond market’s assault has indeed abated, but only the most

carried-away kite-flying oyster-eater could believe that this crisis is over for good. At

some point in the next few months, during which Greece has to raise at least €20

billion ($27 billion) in the bond markets, its finances are likely to be tested again.

Greece’s plans to restructure its economy lack credibility, the euro zone’s promised

rescue is vague and the whole confection threatens to be needlessly expensive.

European leaders bought time this week. They should use it to devise something

better.

The problem is that European leaders seem to like their handiwork. The euro zone’s

chieftains promised “determined and co-ordinated action” should the euro come

under threat. There was no detail, but that was intentional. Details would be harder

than generalities for member states to agree on and they would give speculators a

target. Details would also draw the anger of voters at a time when European

solidarity is in short supply. Almost seven out of ten French voters say they now

9. regret the loss of the franc. Germans wonder why a 67-year-old worker from Aachen

must cough up so that an Athenian can retire early at 54 (see article). As its part of

the deal, Greece has to get its deficit below 3% of GDP by the end of 2012, including

a four-percentage-point cut this year. If by mid-March Greece is falling behind, the

euro zone can ask for further cuts. To German ears that sounds like reassuringly

harsh punishment for Greece’s fiddled accounts and profligacy.

Between extremes, uncomfortable reality lies

What is more, the fix appears to have seen off the two extremes that dismay

Europe’s leaders. One is the Eurosceptic fantasy that Greece’s travails herald the

breaking apart of the euro. That will not happen if Greece has support. The other is a

push towards further European integration—which, after the poison spread by the

Lisbon treaty, finally ratified last year, is firmly off the menu (see Charlemagne).

True, Greece will be watched closely, but if compliance counted as federalism, then

the IMF, which has overseen countless such programmes, would long ago have

brought about world government.

The trouble is that the euro-zone plan also has some grave weaknesses. The first is

that its vagueness may come to be seen as a symptom of how hard it would be to

carry out—that, say, domestic objections in France or Germany could thwart it. If so,

investors in Greek bonds may come to doubt the credibility of the rescue promise.

You can see why George Papandreou, the Greek prime minister, asked for more

precision.

The second weakness is that Greece may not be able to restructure fast enough. That

is not only because of the scale of the task. In just a few months Mr Papandreou’s

Socialist government is seeking to overturn decades of tax evasion and easy

government money. The finance minister has already seen his own staff go on

strike—and his ministry’s job is to force the programme through. There is a limit to

what Greeks will tolerate, but nobody knows where it lies. That is why the euro zone

has said it will call on the experts at the IMF to help ensure that Greece stays on

course. However Greece is a full member of the EU and the euro zone. For as long as

the main judgments are in Brussels, it will be hard to convince investors that the

Greek programme is immune from backroom favours.

Some economists favour setting up a European Monetary Fund (see article). We

would rather give the IMF overall charge, even if in Brussels this is seen as a

humiliation and in Athens the fund is viewed as an arm of the American government.

The IMF would lend credibility to Greece’s restructuring and lower the cost of

emergency borrowing: euro-zone countries would have to lend to Greece at punitive

interest rates, to deter future spendthrifts, but the fund can lend its own cash at low

rates. A credible IMF programme would also mean bond-market investors would

charge the Greeks less too. And the less it has to pay, the more restructuring Greece

can get done. The euro zone may be too proud to go to the IMF, but as any Lenten

penitent should know, pride comes before a fall.

11. Competition policy

Prosecutor, judge and jury

Feb 18th 2010

From The Economist print edition

Enforcement of competition law in Europe is unjust and must change

Illustration by David Simonds

EUROPE’S trustbusters have plenty to boast about. Over several decades the

European Commission’s competition directorate has evolved into perhaps the most

important regulator of its kind in the world. It has been rigorous in the development

of antitrust theory and an energetic enforcer of the law. While antitrust policy across

the Atlantic has veered between the activism of the Clinton administration and the

relative laissez-faire of the Bush years, it has shown consistency. More than any

other body it has upheld the principles of the single market, often incurring the wrath

of powerful member states. Yet despite its fine record, there are deep flaws in the

way the directorate operates. The priority of the new competition commissioner,

Joaquín Almunia, must be to address them.

The problems are not new, but they have been given fresh salience by the fallout

from the European Union’s case against Intel (see article). Last May the commission

fined the chipmaker a record €1.06 billion ($1.5 billion) under Article 82 (now 102) of

the European treaty, which forbids dominant firms from abusing their power. The

specific complaint against Intel, brought by its smaller rival, AMD, was that it had

bribed PC-makers to buy its own processors.

12. The sheer size of the fine had an element of grandstanding about it. But a much

bigger worry was that the commission’s trustbusters may have ignored evidence that

could have weakened their case and made Intel’s conduct look less sinister. The EU’s

ombudsman found that in the course of the commission’s investigation, it had failed

to keep a record of a meeting with a senior executive from Dell, one of Intel’s biggest

customers. Critics, whose concerns have increased with the ferocity of the sanctions

imposed, say that by acting simultaneously as investigator, prosecutor, jury and

sentencing judge, the commission is denying defendant firms the basic right to be

heard by an impartial tribunal. They are right.

The rules under which the competition directorate operates, which date back nearly

half a century, are grossly inadequate for the hugely enhanced role it plays today.

There are three main objections. The first is the conflicted role of the case teams.

These are appointed when the competition directorate decides to investigate a

complaint about abusive behaviour from a business rival, an accusation of collusion

or a merger with potentially anti-competitive consequences. The case teams

investigate, propose a verdict and argue for a particular penalty. From the outset, the

process is polluted by a prosecutorial bias. The second objection is that the accused

company is denied a fair hearing. Although it gets the chance to put forward its side

of the argument, it does so only to the case team, not to a neutral judge or hearing

officer. As things stand, the role of the hearing officer is purely procedural. The third

objection is that the final decision on culpability is taken on a vote by 27 politically

appointed commissioners, only one of whom may have attended the defendant’s

hearing.

A fair hearing, please

In no other area of law would it be thought acceptable for the outcome of such

important cases to be determined by a bunch of politicians. In America the antitrust

division of the Department of Justice has to make its arguments in open court, while

even the quasi-judicial commissioners of the Federal Trade Commission appoint a

judge to preside over hearings and publish findings. The process is long-winded and

expensive but it is an intrinsically fairer way to establish the facts.

Even if Mr Almunia procrastinates, change is coming. Europe’s Charter of

Fundamental Rights will finally be ratified next year. It is highly probable that

antitrust appeals to the European Court of Human Rights (based on the unfairness of

a process that levies huge fines but falls far short of the standards expected of the

criminal law) will succeed. Realistically, amending the treaty to remove the

commission’s role as the enforcer of competition law is a non-starter. A more modest

change would, however, improve things greatly and bring European practice closer to

America’s without importing all its excesses. That is to give the hearing officer the

power to make a factual and legal determination based on a proper examination of

the evidence; the 27 commissioners would then have to accept or reject this. The

system would still be far from perfect, but it would be a good deal more just.

14. Rethinking economics

Radical thoughts on 19th Street

Feb 18th 2010

From The Economist print edition

A higher inflation target for central banks would be a bad idea

EVEN in economics, the guardians of orthodoxy are not given to capricious changes

of mind. So when economists at the IMF question received wisdom and the fund’s

established views twice in a week, it is no small matter. Two new papers have done

exactly that. The first reversal, on inflation targets, makes less sense than the

second, on capital controls.

The initial firecracker came on February 12th, with an analysis of the lessons of the

financial crisis for macroeconomic policy, led by Olivier Blanchard, the IMF’s chief

economist. The report called for several bold innovations. The most radical of these is

that central banks should raise their inflation targets—perhaps to 4% from the

standard 2% or so.

The logic is seductive. Because inflation and interest rates were low when the crisis

hit, central banks had little room to cut rates to cushion the economic blow. Once

their policy rates were down to almost zero, the world’s big central banks had to turn

to untested tools, such as quantitative easing. Politicians had to boost enfeebled

monetary policy by loosening their budgets generously. Had inflation and interest

rates been higher, policymakers would have had more room to cut rates. That gain,

Mr Blanchard argues, might outweigh the small distortions from modestly higher

inflation, especially if countries reformed their tax systems to make them inflation-

neutral.

Were central banks starting from scratch, such a cost-benefit analysis would indeed

be the right way to set an inflation target. Even then, Mr Blanchard might be wrong.

He may be understating the costs of higher inflation. Many studies suggest that

17. Economics focus

Disciplinary measures

Feb 18th 2010

From The Economist print edition

In a guest article, Daniel Gros of the Centre for European Policy Studies

(pictured left) and Thomas Mayer of Deutsche Bank argue the case for a

European Monetary Fund

CEPS/Deutsche Bank

THE difficulties facing Greece and other European borrowers expose two big failures

of discipline at the heart of the euro zone. The first is a failure to encourage member

governments to maintain control of their finances. The second, and more overlooked,

is a failure to allow for an orderly sovereign default. To address these issues, we

propose a new euro-area institution, which we dub the European Monetary Fund

(EMF). Although the EMF could not be set up overnight, it is not too late to do so.

Past experience (with Argentina, for instance) suggests that the road to eventual

sovereign insolvency is a long one.

The EMF could be run along similar governance lines to the IMF, by having a

professional staff remote from direct political influence and a board with

representatives from euro-area countries. Just as the existing fund does, the EMF

would conduct regular and broad economic surveillance of member countries. But its

main role would be to design, monitor and fund assistance programmes for euro-area

countries in difficulties, just as the IMF does on a global scale.

Guilt payments

18. For its initial funding the EMF should be given authority to borrow in the markets with

the full and joint backing of all its member countries. Going forward, however, a

simple funding mechanism would also limit the moral hazard that potentially results

from the creation of the fund. Only those countries in breach of set limits on

governments’ debt stocks and annual deficits would have to contribute, giving them

an incentive to keep their finances in order. (Basing contributions on market

indicators of default risk does not seem appropriate since the existence of the EMF

would itself depress credit-default-swap spreads and yield differentials among the

members.)

Countries could, for instance, be charged an annual contribution of 1% of their

“excess debt”, the difference between their actual level of public debt and the limit of

60% of GDP agreed on as one of the Maastricht criteria for euro entry. A similar

charge could be levied on governments’ excess deficits, the amount exceeding the

Maastricht limit of 3% of GDP. Under these parameters the EMF would have

accumulated about €120 billion ($163 billion) over the past decade, enough to cover

the likely costs of rescuing Greece. These levies are not so big that they make it

impossible for offenders to get to grips with their finances. Under this scheme the

Greek contribution to an EMF would have been 0.65% of GDP in 2009.

Any member country could call on the funds of the EMF up to the amount it has

deposited in the past (including interest), provided its fiscal-adjustment programme

has been approved by the Eurogroup of euro-area finance ministers. Any call on EMF

funds above this amount would be possible only if the country agreed to a tailor-

made adjustment programme supervised jointly by the European Commission and

the Eurogroup, and on condition that the EMF ranked ahead of all other creditors.

The EMF’s other job would be to deal with the aftermath of a sudden withdrawal of

market funding from a euro-zone government. The strongest negotiating asset of a

big debtor is always that default cannot be contemplated because it would bring

down the financial system. Few now doubt that euro-area countries would step in and

pick up the bill were Greece’s deficit-reduction programme to fail. To eliminate the

moral hazard this presumption creates, among profligate governments and reckless

investors alike, it is crucial to create mechanisms that minimise the disruptions

caused by a default.

One simple answer is to draw on the successful experience of the Brady bonds that

were used to deal with the impaired debt of Latin American countries in the 1980s. A

default creates ripple effects throughout the financial system because all debt

instruments of a defaulting country become, at least temporarily, worthless and

illiquid. If a euro-area country loses access to market financing, the EMF could step in

and offer all holders of debt issued by the defaulting country an exchange against

new bonds issued by the EMF. The fund would require creditors to take a uniform

“haircut”, or loss, on their existing debt in order to protect taxpayers. The EMF could,

for example, tie its guarantees to the 60%-of-GDP Maastricht limit on debt, so that

creditors of a country with a debt stock of 120% of GDP would face a 50% haircut.

The losses to financial institutions would be limited and certain, reducing the risk of

contagion. The EMF would only exchange debt instruments that had been registered

with it beforehand. That would provide a strong incentive for transparency, because

20. Germany and the euro

Let the Greeks ruin themselves

Feb 18th 2010 | BERLIN

From The Economist print edition

Germany has Europe’s deepest pockets, but it does not want to pay to save

troubled euro-zone economies

Illustration by Peter Schrank

LESS than a year before the euro became the currency of 11 European countries in

January 1999, a declaration signed by 155 German-speaking economists called for an

“orderly”—ie, long—delay. The prospective euro members, they said, had not yet

reduced their debt and deficits to suit a workable monetary union; some were using

“creative accounting” to get there, and a casual attitude towards deficits would

undermine confidence in the euro’s stability.

Now the prediction is coming true, says Wim Kösters, of the Ruhr University in

Bochum and one of the original signatories. Greece, which joined the euro two years

after its inception, has concealed the dodgy state of its finances. Now it is under

attack from speculators. A default could spread panic to other deficit-plagued

economies, including those of Spain and Portugal, with scary consequences for

21. Europe’s already shaky banking system. But if Greece’s partners bail it out, defying

the euro’s founding treaty, the currency will suffer. Either way, the euro is in trouble.

This dilemma is felt especially keenly in Germany. It was a wrench to surrender the

Deutschmark, symbol of post-war recovery and economic success. On the eve of

monetary union 55% of Germans were against it, making their nation the euro zone’s

most reluctant founders. When a “rescue” is mentioned, all eyes fix on Germany,

Europe’s biggest economy and most creditworthy borrower. Germans fear that a

rescue of Greece would, in effect, extend their welfare state to the Mediterranean.

Greece’s travails put Angela Merkel, the chancellor, in an uncomfortable position.

German taxpayers are in no mood to save what they see as profligate Greeks, having

already pledged €500 billion ($682 billion) to shore up their own banks and billions

more for companies. The liberal Free Democratic Party (FDP), the junior partner in

her coalition government, is against a rescue, as are many politicians from her own

Christian Democratic Union (CDU). The Young Entrepreneurs’ Association declared

that it would be “fatal” for Germany to foot the bill for Greece’s “budget chaos”.

A domestic row over welfare makes charity for foreigners a still more awkward

subject. This month the constitutional court ruled that the government had erred in

setting benefits for the main welfare programme, called Hartz IV. It has until the end

of the year to come up with a new formula, which may cost more money. Guido

Westerwelle, the FDP leader, lamented the “late Roman decadence” of a society that

treats welfare beneficiaries more generously than workers. His outburst, in turn,

annoyed Ms Merkel. “I can’t explain to someone on Hartz IV that we can’t give him a

single cent more but that a Greek gets to retire at 63”, said Michael Fuchs, a CDU

leader in the Bundestag.

On February 11th Mrs Merkel joined other European leaders in offering Greece vague

support, while demanding concrete plans to slash its budget deficit. Since the

summit, the demands have become more concrete and talk of aid even more vague.

On February 15th finance ministers from the 16 euro-zone countries told Greece to

take additional steps to cut its budget deficit by four percentage points of GDP to

8.7% this year. A harsh austerity plan, they hope, will be enough to deter

speculators—and to reassure their voters at home that Greece is not getting off

lightly. The model is Ireland, whose brutal spending cuts restored market confidence

without aid from its European neighbours.

A bail-out, Mrs Merkel fears, would break the bargain Germany struck in accepting

the euro: that the single currency’s members would never jeopardise its stability nor

ask Germans to pay for anyone else’s mismanagement. That said, the currency union

was hardly an act of martyrdom by Germany. In the past decade its firms have

modernised and their workers have accepted miserly pay rises, boosting their

competitiveness. In a euro-less Europe, its trading partners could have erased some

of that advantage by devaluing their currencies. Instead, many of Europe’s weaker

economies failed to reform and Germany accumulated gratifyingly large current-

account surpluses. Nor has the crisis been entirely bad news. The euro has weakened

by about 10% against the dollar since the beginning of 2010. Under the

circumstances, that was not a harbinger of inflation but a welcome tonic for European

exports—especially German ones.

23. Sovereign-debt theories

Domino theory

Feb 18th 2010 | WASHINGTON, DC

From The Economist print edition

Assessing the risk that Greece’s woes herald something far worse

Satoshi Kambayashi

HOW far is it from Athens to America and which countries lie on the way? That may

sound like an esoteric geography question, but it is being asked by investors as

Greece’s debt crisis creates global jitters about the safety of sovereign debt. So far

Portugal, Ireland and Spain, the other high-deficit countries on the periphery of the

euro zone, are thought to be next in line. In most big rich economies, yields have

been stable and well below their long-term average (see chart).

But nerves are fraying elsewhere. The cost of insuring against sovereign default has

risen in 47 of the 50 countries for which these instruments exist. Dubai’s sovereign

credit-default-swap spreads soared to their highest level in a year this week, amid

concern about the terms of a debt restructuring by a state-owned conglomerate.

There is increasingly shrill commentary arguing that Greece is the start of a far

24. bigger problem. “A Greek crisis is coming to America”, blared the headline on a

recent Financial Times article by Niall Ferguson, a financial historian.

The stakes are high. A sudden loss of confidence in all sovereign debt, and especially

in American Treasuries, the world’s benchmark “risk-free” asset, would have

calamitous consequences in a still-fragile recovery. Equally, an exaggerated fear of

sovereign risk could prompt governments into premature fiscal austerity, which

might itself push the world economy back into recession.

Neither the shrill nor the sanguine arguments can be dismissed out of hand. Fiscal

pessimists point both to past experience and to the arithmetic of public debt for

evidence that sovereign-debt crises could spread far beyond Greece. The lesson of

history, as documented in a magisterial study of financial crises by Carmen Reinhart

and Ken Rogoff, is that public debt tends to soar after financial crises, rising by an

average of 86% in real terms. Sovereign defaults have often followed.

The arithmetic argument for pessimism is equally compelling. Virtually no rich

country has a “sustainable” debt position, in the narrow sense that none is running a

tight enough budget or is growing quickly enough to stop its debt burden from rising.

The worst offenders on this count are the euro area’s peripheral economies, as well

as Britain and America.

Greece stands out for the size of its debt stock, the scale of its budget deficit and the

grimness of its growth prospects given high domestic costs and an inability to

devalue. Worries about where growth will come from are the main reason why fears

have, so far, focused on the other weak members of the euro zone (although Spain

attracted decent demand for a 15-year bond sale on February 17th).

America and Britain, having their own currencies, are in a different position. But they

are not immune to concerns about growth and debt dynamics. On February 18th

Britain reported a deficit for January, a month of surplus since records began in

1993. Pessimists also fret about the sheer scale of America’s public borrowing and,

25. especially, China’s role in funding it. News that foreign demand for Treasuries fell

sharply in December and that Beijing was a big seller has fanned their concerns.

Nonsense, says the sanguine camp, whose members include Paul Krugman, a

prominent New York Times columnist. In their view, those who fear a sudden rise in

sovereign risk, particularly for America, misunderstand the reasons for the build-up

of sovereign debt and underestimate the role of Treasuries as a safe haven.

Sovereign-bond yields are low because private demand for capital is weak. And it is

likely to stay that way as Anglo-Saxon households rebuild their savings and firms

hold back from investing.

On this view, America and Britain are better compared to Japan than to Greece.

Japan’s public debt—almost 200% of GDP on a gross basis—has risen steadily in the

two decades since its asset bubble burst. It is far higher than in any Anglo-Saxon

economies. Despite several downgrades, Japan has not had a debt crisis.

It is true that Japan, as a big creditor nation, can tap into ample savings at home,

whereas America relies more on foreign investors. But the breadth of the financial

crisis across the rich world, and hence the surfeit of savings relative to investment,

means this distinction can be overdone. What is more, investors still flee to, not

from, American assets when they worry about risk. The dollar has risen by 4.8%

against the euro since the start of the year. Existing investors in American debt, such

as China, have no incentive to drive down its value with a fire sale of their holdings.

If Greece’s plight shows that investor sentiment can change quickly and Japan’s

history shows that it need not, where do other sovereigns stand? So far low yields

have vindicated the sanguine view for all but those on the very edge of the euro

zone. But there are three reasons to believe that could change.

The first lies in the strength of emerging markets. A gradual reorientation of their

economies towards domestic spending will slowly reduce the global supply of savings,

even if rich-country growth remains weak. Other things being equal, that ought to

push up the cost of capital. At the same time rapid growth means most emerging

economies’ sovereign-debt ratios, already much lower than those in the rich world,

will fall. True, rich countries can point to a far superior payment record. Over the

past 50 years sovereign defaults have been confined to the emerging world. But the

definition of what is a “safe” borrower could shift, benefiting Brazil, say, and hurting

America and Britain.

Second, the debt problems in big rich economies go well beyond the temporary

effects of the crisis. It is thanks to an ageing population and soaring health and

pension costs that America’s debt ratio will still be rising in a decade. Investors have

long shrugged off this structural deterioration. Insouciance seems less likely when

the starting point is much higher debt.

Third, the rise in interest rates that should naturally accompany an economic

recovery and increased investment demand might itself spawn a higher risk premium

on sovereign debt, especially in America. The average maturity on federal debt is less

than five years, so higher yields translate relatively quickly into bigger interest

payments, worsening the fiscal position. Richard Berner of Morgan Stanley expects

ten-year bond yields to reach 5.5% by December, up from 3.7% now.

27. Antitrust in the European Union

Unchained watchdog

Feb 18th 2010

From The Economist print edition

Businesses think Europe’s trustbusters should be kept on a tighter leash

Illustration by David Simonds

IT WAS probably with some relief that Joaquín Almunia took up his post as the

European Union’s competition commissioner earlier this month. One of his main tasks

in his previous job, as commissioner for monetary affairs, was to police the public

finances of the countries that use the euro. But he lacked any means to sanction the

fiscally lax, such as Greece. That left a mess that his successor is now struggling to

clean up.

In his new job Mr Almunia may have the opposite problem: too much power. He has

the authority to block mergers, to force companies to sell assets and to fine heavily

firms judged to have thwarted fair competition. There is only limited redress for

businesses that feel they have been punished unfairly. All this has prompted a

growing fuss about how his agency treats companies it accuses of taking part in

28. cartels or of trying to maintain monopolies by freezing out smaller rivals. The

commission, competition lawyers complain, acts as prosecutor, judge and jury.

Cases often start with a complaint, which is taken up by a “case team”. After a long

investigation the commission issues a “statement of objections”—an indictment, in

effect. Companies are then entitled to a hearing at which they can dispute the

charges. If the commission feels its case still stands up, it finds against the firm and

determines a penalty.

The previous commissioner, Neelie Kroes, boasted about the fines she raised from

miscreants, including Microsoft and Intel. Penalties have often been big enough to

dent profits, even at mammoth corporations. Companies argue, reasonably, that

there should be legal safeguards to match the punishments they face. They would

prefer a court-like process in which they could question witnesses and introduce

evidence. The issue has already stirred the Brussels bureaucracy. Before Mr

Almunia’s feet were under the desk, the commission had circulated draft proposals on

ways to tighten up its procedures when investigating cartels and anti-competitive

practices.

The soul-searching is part of the fallout from the EU’s case against Intel. The

commission fined the chipmaker a record €1.06 billion ($1.5 billion) last May for

using loyalty discounts to stop its main rival, AMD, from challenging its dominance. It

soon emerged that the trustbusters had failed to keep a record of a meeting with an

executive from Dell, a big computer-maker. For some, this oversight only confirmed

suspicions that commission staff overlook potentially exculpatory evidence.

Moreover, trustbusters are as much settlers of disputes between rival firms as

guardians of vibrant competition, and that dual role may encourage meretricious

cases. Companies are well aware that a plausible complaint to the commission can be

a way of tying rivals up in costly litigation. The EU’s trustbusters routinely proclaim

that they aim to protect competition not competitors. Yet big technology firms

acknowledge that antitrust lawsuits have become just another weapon in the battle

for markets.

Establishing the facts in such cases is far from straightforward. Loyalty discounts, for

example, can benefit consumers in that they pave the way for lower prices, but can

also make it hard for competitors to survive, which can lead to higher prices in the

long run. Judgments may turn on motive, and there are fears that prosecutors

convinced of their case may miss evidence at odds with it.

Companies complain that by the time hearings take place case teams are wedded to

their version of events, even if they hear a convincing defence. It rankles that the

commissioner, who in effect decides cases, does not always attend hearings. There is

no cross-examination of witnesses. No independent arbiter judges the merits of

opposing arguments. “It’s just a bunch of lawyers showing PowerPoint slides,” says

one firm’s legal counsel. Companies have the right to appeal against the

commission’s rulings but that can take two or three years. The courts do not retry

cases or hear new evidence. They merely assess whether a verdict was plausible, and

defer to the commission’s reasoning on anything “complex”.

Cartel cases may be more clear-cut but the calls for better safeguards are just as

loud. The EU’s trustbusters rely on amnesties to crack price-fixing rings: the first

30. Business.view

Unlikely heroes

Feb 16th 2010

From Economist.com

Can hedge funds save the world? One pundit thinks so

“HEDGE funds are fundamentally evil and there is no way to view them in any other

light. You’re a great guy, but let’s not be ridiculous!” This was the response that Jed

Emerson received from several erstwhile supporters when he circulated a draft paper

claiming that, in at least some circumstances, the activities of hedge funds could be

good for society and even for the planet.

Many people might struggle with the idea of hedge funds being a force for good,

regarding them as obsessively focused on short-term financial gain regardless of the

environmental or social consequences. And Mr Emerson makes an unlikely defender

of them, since he is as green in tooth and claw as a capitalist can be. Having first

worked organising projects for the homeless, then as one of the first “venture

philanthropists”, he made his name with a series of academic papers on what he calls

blended value—the notion that the performance of a business should be judged not

just by its profitability, but also by its impact on society and the environment.

After a stint in the philanthropic arm of Al Gore’s environmentalist money-

management firm, Generation Investment Management, in the summer of 2008 he

started working for a fund of hedge funds. This triggered a period of soul-searching

that ultimately produced his controversial new paper, “Beyond Good Versus Evil:

Hedge Fund Investing, Capital Markets and the Sustainability Challenge.”

In the financial

crisis, supposedly

risky “socially

tinged”

investments did

reasonably well

Soon after Mr Emerson entered the hedge-fund world, it collapsed spectacularly in

the financial crisis. But he noticed that supposedly risky “socially tinged”

investments, such as those in microfinance bonds, performed reasonably well,

turning in positive returns as many hedge funds lost a large chunk of their value.

31. “The financial world as defined by traditional measures of risk and return was rolled

on its head,” he says. This prompted Mr Emerson to start probing hedge funds’

investment practices, and he was surprised to discover how similar they often were

to those of a socially and environmentally driven movement known as sustainable

finance. “Not the same, mind you, but quite similar nonetheless,” he says. According

to the paper, such sustainable investing accounts for around $2.7 trillion of the $25

trillion invested in America’s capital markets. The total invested in hedge funds of

every variety in early 2009 was about $1.3 trillion.

Mr Emerson’s paper focuses only on that part of the hedge fund-world which employs

fundamental long/short strategies, which means researching the long-term prospects

of a company and either holding its shares or shorting them accordingly. He does not

explore, for example, macro strategies (which bet on, say, movements in exchange

rates), let alone “black box” trading strategies that plough through masses of data,

seeking patterns that can be exploited.

Trading according to rigorous fundamental research can often mirror sustainable

investing, which seeks to profit by taking into account social and environmental

factors, he says. Fundamental hedge funds are far more likely than other investors to

try to identify a firm’s off-balance-sheet exposures, of which a growing proportion

may be “environmental or social liabilities present in a market or company but not

explicitly accounted for in traditional numeric valuation or mainstream investor

analysis”. These types of hedge fund also tend to make relatively little use of

leverage, so they are less easily convicted than some of their hedge-fund peers of

recklessly gambling with other people’s money. Nor do they try to profit by “creating

market distortions within the very markets they are investing in”.

Even short-selling

could be socially

useful

The most interesting section of Mr Emerson’s paper is entitled “Shorting as a Social

Act?”. It has become fashionable even among mainstream capitalists to condemn the

hedge funds that, for example, shorted the shares of banks in the run up to the

meltdown in the markets in 2008. There are two sides to this coin, he points out,

since shorting can also act as a “canary in a coal mine” to warn the wider market of

impending problems and the potential for decreased future performance. Shorting

can also help stop market bubbles forming. Used judiciously, to reward attentive

investors and alert the broader market to ill-understood risks that a company faces,

shorting may indeed be seen as a positive social act, he says.

You can take the man out of the movement, but you can’t take the movement out of

the man: Mr Emerson now sees the potential for a powerful coalition of hedgies (who

short, but only rarely engage in shareholder activism) and investors with a yen for

sustainability, such as pension funds (which may press for better management or

33. The gods strike back

Feb 11th 2010

From The Economist print edition

Financial risk got ahead of the world’s ability to manage it. Matthew

Valencia (interviewed here) asks if it can be tamed again

Illustration by Tim Marrs

“THE revolutionary idea that defines the boundary between modern times and the

past is the mastery of risk: the notion that the future is more than a whim of the

gods and that men and women are not passive before nature.” So wrote Peter

Bernstein in his seminal history of risk, “Against the Gods”, published in 1996. And so

it seemed, to all but a few Cassandras, for much of the decade that followed. Finance

enjoyed a golden period, with low interest rates, low volatility and high returns. Risk

seemed to have been reduced to a permanently lower level.

This purported new paradigm hinged, in large part, on three closely linked

developments: the huge growth of derivatives; the decomposition and distribution of

credit risk through securitisation; and the formidable combination of mathematics

and computing power in risk management that had its roots in academic work of the

mid-20th century. It blossomed in the 1990s at firms such as Bankers Trust and

JPMorgan, which developed “value-at-risk” (VAR), a way for banks to calculate how

much they could expect to lose when things got really rough.

34. Suddenly it seemed possible for any financial risk to be measured to five decimal

places, and for expected returns to be adjusted accordingly. Banks hired hordes of

PhD-wielding “quants” to fine-tune ever more complex risk models. The belief took

hold that, even as profits were being boosted by larger balance sheets and greater

leverage (borrowing), risk was being capped by a technological shift.

There was something self-serving about this. The more that risk could be calibrated,

the greater the opportunity to turn debt into securities that could be sold or held in

trading books, with lower capital charges than regular loans. Regulators accepted

this, arguing that the “great moderation” had subdued macroeconomic dangers and

that securitisation had chopped up individual firms’ risks into manageable lumps. This

faith in the new, technology-driven order was reflected in the Basel 2 bank-capital

rules, which relied heavily on the banks’ internal models.

There were bumps along the way, such as the near-collapse of Long-Term Capital

Management (LTCM), a hedge fund, and the dotcom bust, but each time markets

recovered relatively quickly. Banks grew cocky. But that sense of security was

destroyed by the meltdown of 2007-09, which as much as anything was a crisis of

modern metrics-based risk management. The idea that markets can be left to police

themselves turned out to be the world’s most expensive mistake, requiring $15

trillion in capital injections and other forms of support. “It has cost a lot to learn how

little we really knew,” says a senior central banker. Another lesson was that

managing risk is as much about judgment as about numbers. Trying ever harder to

capture risk in mathematical formulae can be counterproductive if such a degree of

accuracy is intrinsically unattainable.

For now, the hubris of spurious precision has given way to humility. It turns out that

in financial markets “black swans”, or extreme events, occur much more often than

the usual probability models suggest. Worse, finance is becoming more fragile: these

days blow-ups are twice as frequent as they were before the first world war,

according to Barry Eichengreen of the University of California at Berkeley and Michael

Bordo of Rutgers University. Benoit Mandelbrot, the father of fractal theory and a

pioneer in the study of market swings, argues that finance is prone to a “wild”

randomness not usually seen in nature. In markets, “rare big changes can be more

significant than the sum of many small changes,” he says. If financial markets

followed the normal bell-shaped distribution curve, in which meltdowns are very rare,

the stockmarket crash of 1987, the interest-rate turmoil of 1992 and the 2008 crash

would each be expected only once in the lifetime of the universe.

This is changing the way many financial firms think about risk, says Greg Case, chief

executive of Aon, an insurance broker. Before the crisis they were looking at things

like pandemics, cyber-security and terrorism as possible causes of black swans. Now

they are turning to risks from within the system, and how they can become amplified

in combination.

Cheap as chips, and just as bad for you

It would, though, be simplistic to blame the crisis solely, or even mainly, on sloppy

risk managers or wild-eyed quants. Cheap money led to the wholesale underpricing

35. of risk; America ran negative real interest rates in 2002-05, even though consumer-

price inflation was quiescent. Plenty of economists disagree with the recent assertion

by Ben Bernanke, chairman of the Federal Reserve, that the crisis had more to do

with lax regulation of mortgage products than loose monetary policy.

Equally damaging were policies to promote home ownership in America using Fannie

Mae and Freddie Mac, the country’s two mortgage giants. They led the duo to binge

on securities backed by shoddily underwritten loans.

In the absence of strict limits, higher leverage followed naturally from low interest

rates. The debt of America’s financial firms ballooned relative to the overall economy

(see chart 1). At the peak of the madness, the median large bank had borrowings of

37 times its equity, meaning it could be wiped out by a loss of just 2-3% of its

assets. Borrowed money allowed investors to fake “alpha”, or above-market returns,

says Benn Steil of the Council on Foreign Relations.

The agony was compounded by the proliferation of short-term debt to support illiquid

long-term assets, much of it issued beneath the regulatory radar in highly leveraged

“shadow” banks, such as structured investment vehicles. When markets froze,

sponsoring entities, usually banks, felt morally obliged to absorb their losses.

“Reputation risk was shown to have a very real financial price,” says Doug Roeder of

the Office of the Comptroller of the Currency, an American regulator.

Everywhere you looked, moreover, incentives were misaligned. Firms deemed “too

big to fail” nestled under implicit guarantees. Sensitivity to risk was dulled by the

“Greenspan put”, a belief that America’s Federal Reserve would ride to the rescue

with lower rates and liquidity support if needed. Scrutiny of borrowers was delegated

to rating agencies, who were paid by the debt-issuers. Some products were so

complex, and the chains from borrower to end-investor so long, that thorough due

diligence was impossible. A proper understanding of a typical collateralised debt

obligation (CDO), a structured bundle of debt securities, would have required reading

30,000 pages of documentation.

36. Fees for securitisers were paid largely upfront, increasing the temptation to originate,

flog and forget. The problems with bankers’ pay went much wider, meaning that it

was much better to be an employee than a shareholder (or, eventually, a taxpayer

picking up the bail-out tab). The role of top executives’ pay has been overblown. Top

brass at Lehman Brothers and American International Group (AIG) suffered massive

losses when share prices tumbled. A recent study found that banks where chief

executives had more of their wealth tied up in the firm performed worse, not better,

than those with apparently less strong incentives. One explanation is that they took

risks they thought were in shareholders’ best interests, but were proved wrong.

Motives lower down the chain were more suspect. It was too easy for traders to cash

in on short-term gains and skirt responsibility for any time-bombs they had set

ticking.

Asymmetries wreaked havoc in the vast over-the-counter derivatives market, too,

where even large dealing firms lacked the information to determine the

consequences of others failing. Losses on contracts linked to Lehman turned out to

be modest, but nobody knew that when it collapsed in September 2008, causing

panic. Likewise, it was hard to gauge the exposures to “tail” risks built up by sellers

of swaps on CDOs such as AIG and bond insurers. These were essentially put options,

with limited upside and a low but real probability of catastrophic losses.

Another factor in the build-up of excessive risk was what Andy Haldane, head of

financial stability at the Bank of England, has described as “disaster myopia”. Like

drivers who slow down after seeing a crash but soon speed up again, investors

exercise greater caution after a disaster, but these days it takes less than a decade

to make them reckless again. Not having seen a debt-market crash since 1998,

investors piled into ever riskier securities in 2003-07 to maintain yield at a time of

low interest rates. Risk-management models reinforced this myopia by relying too

heavily on recent data samples with a narrow distribution of outcomes, especially in

subprime mortgages.

A further hazard was summed up by the assertion in 2007 by Chuck Prince, then

Citigroup’s boss, that “as long as the music is playing, you’ve got to get up and

dance.” Performance is usually judged relative to rivals or to an industry benchmark,

encouraging banks to mimic each other’s risk-taking, even if in the long run it

benefits no one. In mortgages, bad lenders drove out good ones, keeping up with

aggressive competitors for fear of losing market share. A few held back, but it was

not easy: when JPMorgan sacrificed five percentage points of return on equity in the

short run, it was lambasted by shareholders who wanted it to “catch up” with zippier-

looking rivals.

An overarching worry is that the complexity of today’s global financial network makes

occasional catastrophic failure inevitable. For example, the market for credit

derivatives galloped far ahead of its supporting infrastructure. Only now are serious

moves being made to push these contracts through central clearing-houses which

ensure that trades are properly collateralised and guarantee their completion if one

party defaults.

37. Network overload

The push to allocate capital ever more efficiently over the past 20 years created what

Till Guldimann, the father of VAR and vice-chairman of SunGard, a technology firm,

calls “capitalism on steroids”. Banks got to depend on the modelling of prices in

esoteric markets to gauge risks and became adept at gaming the rules. As a result,

capital was not being spread around as efficiently as everyone believed.

Big banks had also grown increasingly interdependent through the boom in

derivatives, computer-driven equities trading and so on. Another bond was cross-

ownership: at the start of the crisis, financial firms held big dollops of each other’s

common and hybrid equity. Such tight coupling of components increases the danger

of “non-linear” outcomes, where a small change has a big impact. “Financial markets

are not only vulnerable to black swans but have become the perfect breeding ground

for them,” says Mr Guldimann. In such a network a firm’s troubles can have an

exaggerated effect on the perceived riskiness of its trading partners. When Lehman’s

credit-default spreads rose to distressed levels, AIG’s jumped by twice what would

have been expected on its own, according to the International Monetary Fund.

Mr Haldane has suggested that these knife-edge dynamics were caused not only by

complexity but also—paradoxically—by homogeneity. Banks, insurers, hedge funds

and others bought smorgasbords of debt securities to try to reduce risk through

diversification, but the ingredients were similar: leveraged loans, American

mortgages and the like. From the individual firm’s perspective this looked sensible.

But for the system as a whole it put everyone’s eggs in the same few baskets, as

reflected in their returns (see chart 2).

Efforts are now under way to deal with these risks. The Financial Stability Board, an

international group of regulators, is trying to co-ordinate global reforms in areas such

as capital, liquidity and mechanisms for rescuing or dismantling troubled banks. Its

biggest challenge will be to make the system more resilient to the failure of giants.

39. Printing body parts

Making a bit of me

Feb 18th 2010

From The Economist print edition

A machine that prints organs is coming to market

Illustration by David Simonds

THE great hope of transplant surgeons is that they will, one day, be able to order

replacement body parts on demand. At the moment, a patient may wait months,

sometimes years, for an organ from a suitable donor. During that time his condition

may worsen. He may even die. The ability to make organs as they are needed would

not only relieve suffering but also save lives. And that possibility may be closer with

the arrival of the first commercial 3D bio-printer for manufacturing human tissue and

organs.

The new machine, which costs around $200,000, has been developed by Organovo, a

company in San Diego that specialises in regenerative medicine, and Invetech, an

engineering and automation firm in Melbourne, Australia. One of Organovo’s

founders, Gabor Forgacs of the University of Missouri, developed the prototype on

which the new 3D bio-printer is based. The first production models will soon be

40. delivered to research groups which, like Dr Forgacs’s, are studying ways to produce

tissue and organs for repair and replacement. At present much of this work is done

by hand or by adapting existing instruments and devices.

To start with, only simple tissues, such as skin, muscle and short stretches of blood

vessels, will be made, says Keith Murphy, Organovo’s chief executive, and these will

be for research purposes. Mr Murphy says, however, that the company expects that

within five years, once clinical trials are complete, the printers will produce blood

vessels for use as grafts in bypass surgery. With more research it should be possible

to produce bigger, more complex body parts. Because the machines have the ability

to make branched tubes, the technology could, for example, be used to create the

networks of blood vessels needed to sustain larger printed organs, like kidneys, livers

and hearts.

Printing history

Organovo’s 3D bio-printer works in a similar way to some rapid-prototyping machines

used in industry to make parts and mechanically functioning models. These work like

inkjet printers, but with a third dimension. Such printers deposit droplets of polymer

which fuse together to form a structure. With each pass of the printing heads, the

base on which the object is being made moves down a notch. In this way, little by

little, the object takes shape. Voids in the structure and complex shapes are

supported by printing a “scaffold” of water-soluble material. Once the object is

complete, the scaffold is washed away.

Researchers have found that something similar can be done with biological materials.

When small clusters of cells are placed next to each other they flow together, fuse

and organise themselves. Various techniques are being explored to condition the cells

to mature into functioning body parts—for example, “exercising” incipient muscles

using small machines.

Though printing organs is new, growing them from scratch on scaffolds has already

been done successfully. In 2006 Anthony Atala and his colleagues at the Wake Forest

Institute for Regenerative Medicine in North Carolina made new bladders for seven

patients. These are still working.

Dr Atala’s process starts by taking a tiny sample of tissue from the patient’s own

bladder (so that the organ that is grown from it will not be rejected by his immune

system). From this he extracts precursor cells that can go on to form the muscle on

the outside of the bladder and the specialised cells within it. When more of these

cells have been cultured in the laboratory, they are painted onto a biodegradable

bladder-shaped scaffold which is warmed to body temperature. The cells then mature

and multiply. Six to eight weeks later, the bladder is ready to be put into the patient.

The advantage of using a bioprinter is that it eliminates the need for a scaffold, so Dr

Atala, too, is experimenting with inkjet technology. The Organovo machine uses stem

cells extracted from adult bone marrow and fat as the precursors. These cells can be

coaxed into differentiating into many other types of cells by the application of

appropriate growth factors. The cells are formed into droplets 100-500 microns in

42. Lighting

Printed circuit

Feb 18th 2010

From The Economist print edition

A way to turn out lighting by the metre

Alamy

You’re history!

THE printing of body parts (see article) will probably remain a bespoke industry for

ever. Printed lighting, though, might be mass produced. That, at least, is the promise

of a technology being developed in Sweden by Ludvig Edman of Umea University and

Nathaniel Robinson of Linkoping. Dr Edman and Dr Robinson have taken a promising

technique called the organic light-emitting diode, or OLED, and tweaked it in an

ingenious way. The result is a sheet similar to wallpaper that can illuminate itself at

the flick of a switch.

An OLED is a layer of semiconducting polymer sandwiched between two conductive

layers that act as electrodes. When a current is passed between these electrodes, the

polymer gives off light. The light is created by electrons released from one electrode

layer falling into positively charged “holes” that have been generated by the

polymer’s interaction with the other layer. These holes are gaps in the polymer’s

electronic structure where an electron ought to be, but isn’t.

44. Private-sector space flight

Moon dreams

Feb 18th 2010

From The Economist print edition

The Americans may still go to the moon before the Chinese

AP

Can you direct me to reception, please?

WHEN America’s space agency, NASA, announced its spending plans in February,

some people worried that its cancellation of the Constellation moon programme had

ended any hopes of Americans returning to the Earth’s rocky satellite. The next

footprints on the lunar regolith were therefore thought likely to be Chinese. Now,

though, the private sector is arguing that the new spending plan actually makes it

more likely America will return to the moon.

The new plan encourages firms to compete to provide transport to low Earth orbit

(LEO). The budget proposes $6 billion over five years to spur the development of

commercial crew and cargo services to the international space station. This money

will be spent on “man-rating” existing rockets, such as Boeing’s Atlas V, and on

developing new spacecraft that could be launched on many different rockets. The

point of all this activity is to create healthy private-sector competition for transport to

the space station—and in doing so to drive down the cost of getting into space.

45. Eric Anderson, the boss of a space-travel company called Space Adventures, is

optimistic about the changes. They will, he says, build “railroads into space”. Space

Adventures has already sent seven people to the space station, using Russian

rockets. It would certainly benefit from a new generation of cheap launchers.

Another potential beneficiary—and advocate of private-sector transport—is Robert

Bigelow, a wealthy entrepreneur who founded a hotel chain called Budget Suites of

America. Mr Bigelow has so far spent $180m of his own money on space

development—probably more than any other individual in history. He has been

developing so-called expandable space habitats, a technology he bought from NASA

a number of years ago.

These habitats, which are folded up for launch and then inflated in space, were

designed as interplanetary vehicles for a trip to Mars, but they are also likely to be

useful general-purpose accommodation. The company already has two scaled-down

versions in orbit.

Mr Bigelow is preparing to build a space station that will offer cheap access to space

to other governments—something he believes will generate a lot of interest. The

current plan is to launch the first full-scale habitat (called Sundancer) in 2014.

Further modules will be added to this over the course of a year, and the result will be

a space station with more usable volume than the existing international one. Mr

Bigelow’s price is just under $23m per astronaut. That is about half what Russia

charges for a trip to the international station, a price that is likely to go up after the

space shuttle retires later this year. He says he will be able to offer this price by bulk-

buying launches on newly man-rated rockets. Since most of the cost of space travel

is the launch, the price might come down even more if the private sector can lower

the costs of getting into orbit.

The ultimate aim of all his investment, Mr Bigelow says, is to get to the moon. LEO is

merely his proving ground. He says that if the technology does work in orbit, the

habitats will be ideal for building bases on the moon. To go there, however, he will

have to prove that the expandable habitat does indeed work, and also generate

substantial returns on his investment in LEO, to provide the necessary cash.

If all goes well, the next target will be L1, the point 85% of the way to the moon

where the gravitational pulls of moon and Earth balance. “It’s a terrific dumping off

point,” he says. “We could transport a completed lunar base [to L1] and put it down

on the lunar surface intact.”

There are others with lunar ambitions, too. Some 20 teams are competing for the

Google Lunar X Prize, a purse of $30m that will be given to the first private mission

which lands a robot on the moon, travels across the surface and sends pictures back

to Earth. Space Adventures, meanwhile, is in discussions with almost a dozen

potential clients about a circumlunar mission, costing $100m a head.

The original Apollo project was mainly a race to prove the superiority of American

capitalism over Soviet communism. Capitalism won—but at the cost of creating, in

NASA, one of the largest bureaucracies in American history. If the United States is to

return to the moon, it needs to do so in a way that is demonstrably superior to the

first trip—for example, being led by business rather than government. Engaging in

47. Polar ice shelves

Breaking waves

Feb 18th 2010

From The Economist print edition

The coup de grace that shatters ice shelves is administered by ocean waves

IN 2008 part of the Wilkins ice shelf on the edge of the Antarctic peninsular suddenly

disintegrated. It was seen by some as a portend. If other, larger shelves—huge ice

sheets that have slipped off the land but are not floating freely on the sea—were to

break up in a similar way, their non-floating ice (which is not subject to Archimedes’s

principle that it displaces its own weight of water) would be converted into floating

ice (which is), and the sea level would rise.

The Wilkins shelf may or may not have been the victim, ultimately, of climate

change. Regardless of what weakened it, though, it was not rising temperatures that

caused the sudden break up. Peter Bromirski of the Scripps Institution of

Oceanography in San Diego thinks he knows what did: a little-studied phenomenon

called infragravity waves.

Ocean waves come in several varieties. Normal swells, known technically as gravity

waves, are created by wind pushing the surface of the sea up and gravity then

pulling it down, causing it to bounce. Gravity waves have a frequency of about once

every 30 seconds. When such swells hit the coast, however, part of their energy is

transformed into vibrations that have periods ranging from 50 to 350 seconds. These

are infragravity waves, so called because they are sub-harmonics of the original

gravity waves.

Most infragravity waves hug the coast. A few, though, break free—and such open-

ocean waves are powerful and can travel great distances. Some generated off the

coast of South America, for example, make it all the way to Antarctica.

Long-term monitoring of the vibrations induced by ocean waves in Antarctic ice

shelves is a recent phenomenon. In the past the seismometers required to do so

have not been robust enough to survive such brutal conditions. Dr Bromirski,

however, knew of a study that had deployed seismometers successfully on the Ross

ice shelf, and he was able to reanalyse the data from it.

The original analysis had detected storm-driven swell shaking the ice. Dr Bromirski’s

work showed a second signal. Waves with longer periods were also shaking the Ross

shelf—indeed, they were inducing a much larger response than the storm waves

were. Dr Bromirski and his colleagues report in Geophysical Research Letters that the

movements caused by infragravity waves were three times larger than those induced

by the swell. Moreover, although floating sea ice damped the swell, reducing its

49. Green.view

Copenhagen accounting

Feb 16th 2010

From Economist.com

What countries are currently offering on climate

SINCE the fractious negotiations that produced a last-minute “accord” at the

Copenhagen climate-change meeting last year, those in and out of government who

concern themselves with climate policy have been in a state of some befuddlement.

They wonder what it all means, how to build on it and whom to blame for its

perceived deficiencies and the troublesome circumstances of its birth. Despite this

the accord has already achieved a couple of the aims its framers intended. Neither is,

of itself, earth-shattering, far less Earth-saving. But they are worth noting, not least

for what they reveal about where climate diplomacy should be focusing.

The accord provided a way for countries to make public, if non-binding, commitments

on climate change. By the early February deadline that was set for this, some 90 of

them had done so. In the weeks since, various stalwarts of the climate-wonkery

circuit have been working out what those commitments might mean. That process is

made complex by the fact that countries can express their intentions in different

ways, and that many have provided two or more levels of commitment: a low one

that they say they will pursue regardless, and one or more higher ones that they will

try for if enough other countries are also going high.

AFP

The unsurprising bottom line of the various analyses is that even if you add up all the

high commitments, you do not get a package that keeps average warming below

50. 2°C. In an analysis provided by the Climate Scoreboard run by the Sustainability

Institute, a research group based in Vermont, adding up the more ambitious

commitments and extrapolating to 2100 gives a 90% probability that global

temperatures would be between 1.7 and 4.7°C above the pre-industrial baseline.

Given that range, the chances of being in the part below 2°C are slim. A 50-50

chance of staying the right side of two degrees would require cuts something like half

as large again.

Insufficient as they are, those high commitments remain pretty much the same as

the positions with which negotiators arrived in Copenhagen. As such, they represent

one of the accord’s modest successes. One of its purposes was to square away those

offers in the face of a total collapse of the conference: to provide a ratchet that, while

not offering progress, limited backsliding.

Another of the accord’s purposes was to provide a way for the world to move beyond

the besetting problem of the Kyoto protocol. That protocol requires developed

countries that have ratified it to reduce their emissions while imposing no such

strictures on the rest of the world, and politicians from the rich world who are critical

of Kyoto make much of this iniquity. They may be surprised, then, to learn that the

bulk of the commitments to reduced emissions in the Copenhagen accord come from

developing countries.

The effect is most striking if you look at the “low-abatement” figures—the sum of

what countries say they will do regardless of other countries’ actions. Before

Copenhagen, according to an analysis by the European Climate Foundation (ECF), a

not-for-profit organisation devoted to climate policy, these commitments added up to

an annual reduction of 3.6 billion tonnes of carbon dioxide, compared with business

as usual, by 2020. In the commitments under the accord that figure has risen to 5.0

billion tonnes, of which developing-country commitments account for 4.2 billion

tonnes. The developing world has increased its commitment by two-thirds since

Copenhagen. The developed world has cut its by about a quarter, from 1.1 billion

tonnes to 800m tonnes.

The developed-country change reflects alterations in professed policy by Russia,

Canada and a few others. The developing-country change comes mostly from the

growth and firming up of the commitments on deforestation made by Indonesia and

Brazil. One of the underappreciated aspects of Copenhagen was progress on the

question of what can be done about deforestation, which currently accounts for a bit

less than 20% of global emissions. Reducing deforestation is a comparatively cheap

way of reducing emissions, with other benefits to boot. The scope for going farther

than the current commitments, using various sorts of finance, remains high.

In increasing the amount of abatement from the 5 billion tonnes of those opening