Accounting mechanics basic records

•Download as PPT, PDF•

1 like•225 views

Accounting mechanics basic records

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Accounting mechanics basic records

Similar to Accounting mechanics basic records (20)

More from Aswin prakash i , Xantus Technologies

More from Aswin prakash i , Xantus Technologies (20)

Recently uploaded

Recently uploaded (20)

Accounting mechanics basic records

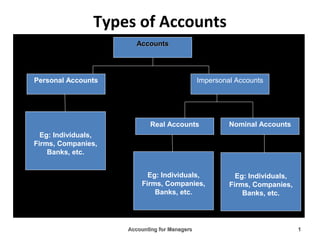

- 1. Types of Accounts Accounting for ManagersAccounting for Managers 11 Eg: Individuals, Firms, Companies, Banks, etc. Eg: Individuals, Firms, Companies, Banks, etc. Real Accounts Nominal Accounts Eg: Individuals, Firms, Companies, Banks, etc. Impersonal AccountsPersonal Accounts AccountsAccounts

- 2. Rules of Debit and Credit Accounting for ManagersAccounting for Managers 22 Rules of Debit and Credit Personal Accounts Nominal Accounts The Receiver All expenses and losses The Giver All incomes and gains Real Accounts What Comes in What goes out Debit Credit

- 3. Journal • The daily business transactions are recorded in a book called Journal. The journal is called ‘book of original entry.’ • All the transactions are first entered in the journal in the order of their occurrence. • Recording of entries in the journal is known as journalizing. Accounting for ManagersAccounting for Managers 33

- 4. Format of a Journal Accounting for ManagersAccounting for Managers 44 Date Particulars L.F. Debit Rs. Credit Rs.

- 5. Steps in Journalizing • Analyze the transaction and identify the two accounts that are being affected by the transaction. • Ascertain the nature of the accounts involved as real, personal or nominal. • Determine which rule of debit and credit is applicable for each of accounts involved. Accounting for ManagersAccounting for Managers 55

- 6. Steps in Journalizing • Ascertain the account to be debited and the account to be credited. • Write the name of the account to be debited along with the abbreviation “Dr” on the same line against the name of the account in particulars column and the amount to be debited in the debit amount column against the name of the account. Accounting for ManagersAccounting for Managers 66

- 7. From the following state the nature of the accounts and which are to be debited and credited 1. Mr A started business with cash 2. Purchased goods from x for cash 3. Sold goods for cash to Y 4. Purchased goods from X for credit 5. Sold goods to B on credit 6. Purchased furniture from ABC 7. Paid wages 8. Discount allowed by Goutam 9. Discount given by A 10. Cash paid into bank 11. Withdrew from bank for office use 12. Withdrew from bank for personal use Accounting for ManagersAccounting for Managers 77

- 8. Steps in Journalizing • Write the name of the account to be credited in the next line preceded by the word “To” at a few spaces towards the right in the particulars column, and the amount to be credited in the credit amount column against the name of the account. • Write Narration (a brief description of the transaction) within brackets in the next line in particulars column usually starting with being. Accounting for ManagersAccounting for Managers 88

- 9. Format of a Journal Accounting for ManagersAccounting for Managers 99 Date Particulars L.F. Debit Rs. Credit Rs. Year Mth/date ABC a/c Dr. To XYZ A/c (being……….brief narration) XXX XXX

- 10. Journalize the following 2010 Jan 1 Ahmed commenced business with Rs 75,00,000 3 Opened a current a/c in bank and deposited there Rs 30,00,000 5 Bought furniture Rs 10,00,000 7 Bought goods worth Rs 90,000 for cash 10 Bought goods from Bharath Rs 1,50,000 on account 12 Sold goods to Dayanand Rs 1,25,000 15 Cash sales 75,000 20 Paid to Bharath Rs 1,00,000 26 Withdrew from bank for office use Rs 25,000 28 Withdrew from bank for personal use Rs 30,000 30 Received a cheque from Dayanand Rs 1,00,000 31 Paid rent Rs 15,000 Accounting for ManagersAccounting for Managers 1010

- 11. • A compound journal entry is an accounting entry which effects more than two account heads. • A simple journal entry has one debit and one credit whereas a compound journal entries includes one or more debits and/or credits than a simple journal entry • Instead of recording numerous simple journal entries on a single day it is better to record journal entries as a compound entry because it saves time and keeps related debits and credits in one place. Accounting for ManagersAccounting for Managers 1111

- 12. Trade discount and cash discount 1. Trade discount is given with the aim to purchase at high quantity. Cash discount is given with the aim to get payment fastly and before payment date . 2. Trade discount is shown as deduction in Invoice. Cash Discount is not shown as deduction in Invoice. 3. There is no any accounting treatment for trade discount. There is accounting treatment for cash discount both in vendor and buyer’s day book. Accounting for ManagersAccounting for Managers 1212

- 13. 2010 March 1 Ahmed commenced business with Rs cash 3,00,000,stock 1,00,000 and buildings 4,00,000 and 75000 loan from his brother at 12% 5 Purchased furniture for Rs 1,20,000 from star furniture on credit 7 Bought goods worth Rs 60,000 from Amar 11 Sold goods to Akash Rs 40,000 12 Purchased goods worth Rs 50,000 at 20% trade discount from Hind ltd and paid half of the amount at 5% cash discount 14 Paid to Amar Rs 40,000 15 Sold goods to Mahesh worth Rs 30,000 at 5% trade discount 18 Deposited into bank Rs 45,000 21 Paid to Star furniture house Rs 1,15,000 in full settlement 25 Paid to Hind Ltd Rs 19,000 in full settlement out of which 10,000 was paid in cash and the balance by cheque 26 Mahesh returned good worth Rs 1,500 28 Mahesh paid a cheque of Rs 25,000 29 Received from Akash Rs 30,000 by cheque 30 Paid rent by cheque Rs 4000 31 Paid electricity bill Rs 1,400 31 Akash became insolvent and paid 50 p in a rupee 1313