1. 4. Tax Due Diligence (KPMG) – Main concerns

1

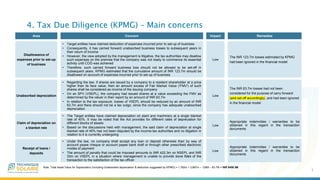

Area Concern Remedies

Disallowance of

expenses prior to set-up

of business

• Target entities have claimed deduction of expenses incurred prior to set-up of business

• Consequently, it has carried forward unabsorbed business losses to subsequent years in

their return of income

• However, the view adopted by the management is litigative, the tax authorities may disallow

such expenses on the premise that the company was not ready to commence its essential

activity until COD was achieved

• Therefore, such carried forward business loss should not be allowed to be set-off in

subsequent years. KPMG estimated that the cumulative amount of INR 123.7m should be

disallowed on account of expenses incurred prior to set-up of business

The INR 123.7m losses estimated by KPMG

had been ignored in the financial model

Impact

Low

Unabsorbed depreciation

• Regarding the law, if shares are issued by a company to a resident shareholder at a price

higher than its face value, then an amount excess of Fair Market Value ('FMV') of such

shares shall be considered as income of the issuing company

• On an SPV (VSEPL), the company had issued shares at a value exceeding the FMV as

determined by the valuer in their report by an amount of INR 63.7m

• In relation to the tax exposure, losses of VSEPL should be reduced by an amount of INR

63.7m and there should not be a tax outgo, since the company has adequate unabsorbed

depreciation

The INR 63.7m losses had not been

considered for the purpose of carry forward

(and set off accordingly), and had been ignored

in the financial model

Low

Claim of depreciation on

a blanket rate

• The Target entities have claimed depreciation on plant and machinery at a single blanket

rate of 40%. It may be noted that the Act provides for different rates of depreciation for

different blocks of assets

• Based on the discussions held with management, the said claim of depreciation at single

blanket rate of 40% has not been disputed by the income-tax authorities and no litigation in

relation to it is currently undergoing

Appropriate indemnities / warranties to be

obtained in this regard in the transaction

documents

Low

Receipt of loans /

deposits

• Under the law, no company shall accept any loan or deposit otherwise than by way of

account payee cheque or account payee bank draft or through other prescribed electronic

modes of payment

• The amount of penalty that could be imposed amounts to INR 422.3m on NSEPL and INR

33m on VSEPL in a situation where management is unable to provide bona fides of the

transaction to the satisfaction of the tax officer

Appropriate indemnities / warranties to be

obtained in this regard in the transaction

documents

Low

Note: Total Asset Value for Depreciation (including Unabsorbed depreciation & deduction suggested by KPMG) = 1,782m + 3,867m – 126M – 63.7M = INR 5459.3M