Recommended

Recommended

More Related Content

Similar to worksheetEnter all amounts as positive numbers. The worksheet is .docx

Similar to worksheetEnter all amounts as positive numbers. The worksheet is .docx (20)

More from ambersalomon88660

More from ambersalomon88660 (20)

Recently uploaded

Recently uploaded (20)

worksheetEnter all amounts as positive numbers. The worksheet is .docx

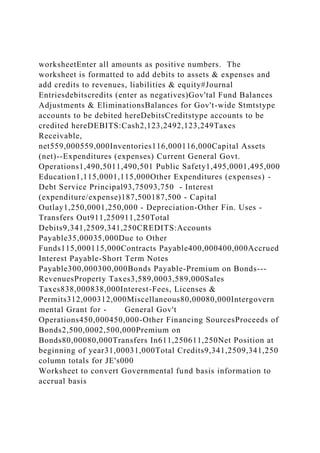

- 1. worksheetEnter all amounts as positive numbers. The worksheet is formatted to add debits to assets & expenses and add credits to revenues, liabilities & equity#Journal Entriesdebitscredits (enter as negatives)Gov'tal Fund Balances Adjustments & EliminationsBalances for Gov't-wide Stmtstype accounts to be debited hereDebitsCreditstype accounts to be credited hereDEBITS:Cash2,123,2492,123,249Taxes Receivable, net559,000559,000Inventories116,000116,000Capital Assets (net)--Expenditures (expenses) Current General Govt. Operations1,490,5011,490,501 Public Safety1,495,0001,495,000 Education1,115,0001,115,000Other Expenditures (expenses) - Debt Service Principal93,75093,750 - Interest (expenditure/expense)187,500187,500 - Capital Outlay1,250,0001,250,000 - Depreciation-Other Fin. Uses - Transfers Out911,250911,250Total Debits9,341,2509,341,250CREDITS:Accounts Payable35,00035,000Due to Other Funds115,000115,000Contracts Payable400,000400,000Accrued Interest Payable-Short Term Notes Payable300,000300,000Bonds Payable-Premium on Bonds--- RevenuesProperty Taxes3,589,0003,589,000Sales Taxes838,000838,000Interest-Fees, Licenses & Permits312,000312,000Miscellaneous80,00080,000Intergovern mental Grant for - General Gov't Operations450,000450,000-Other Financing SourcesProceeds of Bonds2,500,0002,500,000Premium on Bonds80,00080,000Transfers In611,250611,250Net Position at beginning of year31,00031,000Total Credits9,341,2509,341,250 column totals for JE's000 Worksheet to convert Governmental fund basis information to accrual basis

- 2. ActivityProgram RevenuesNet (Expense) Revenue and Change in Net PositionExpensesCharges for ServicesOperational Grants and ContributionsCapital Grants and ContributionsGovernmental ActivitiesBusiness-Type ActivitiesTotalFunctions/ProgramsGovernmental Activities: General Government$ -$ - Public Safety-- Education-- Interest-- Depreciation-- Total Governmental Activities----- -Business Type Activities Water and Sewer-- Total Government$ -$ -$ -$ -$ -$ --General RevenuesTaxes: Property Taxes- Sales Taxes- Fees, Licenses and Permits- Transfers -Enter transfers out as negative and transfers in as positive amounts Total General Revenues---Change in Net Position---Net Position, Beginning--Net Position, Ending$ -$ -$ - PROVINCE OF EUROPA STATEMENT OF ACTIVITIES GOVERNMENT-WIDE BASIS FOR THE YEAR ENDED DECEMBER 31, 2091 Net positionGovernmental ActivitiesBusiness-Type ActivitiesTotalAssetsCash$ -Accounts Receivable (Net)-Taxes Receivable (Net)-Internal Balances Current-Enter payables to other funds as negative, receivables as positve amountsInventories-Capital Assets, Net of Accumulated Depreciation- Total Assets$ -$ -$ - LiabilitiesAccounts Payable-Contracts Payable-Accrued Interest Payable-Short Term Notes Payable-General Obligation Bonds Payable-Premium on Bonds Sold- Total Liabilities--- Net PositionNet Investment in Capital Assets---Unrestricted--- Total Net Position$ -$ -$ - PROVINCE OF EUROPA STATEMENT OF NET POSITION AS OF DECEMBER 31, 2091 Enterprise fundJournal EntriesdebitscreditsDUE FROM3Feb. 1Cash300,000 CASH OTHER FUNDS

- 3. SUPPLIESACCOUNTS RECEIVABLETransfer in - capital contribution300,000bb-bb-bb-bb-To record contribution from GF----ALLOWANCE FORUNCOLLECTIBLE ACCTSBUILDINGS & STRUCTEQUIPMENTGEOTHERMAL GENERATORS- bbbb450,000bb150,000bb650,000450,000150,000650,000- ACCUMULATED DEPRACCUMULATED DEPRACCUMULATED DEPRBUILDINGS & STRUCTEQUIP & MACHINERYGEOTHERMAL GENERATORSbbbbbb--- ACCOUNTS PAYABLECONTRACTS PAYABLEINTEREST PAYABLEST NOTE PAYABLE-bb-bb-bbbb----BONDS PAYABLENET POSITION OPERATING REVENUE: OPERATING EXPENSES1,250,000bbbbCHARGES FOR SERVICES SALARIES EXPENSE1,250,000---OPERATING EXPENSESOPERATING EXPENSES NONOPERATING EXPENSESTRANSFER IN - SUPPLIES EXPENSEDEPRECIATION EXPENSE INTERESTCAPITAL CONTRIBUTIONS----T. Debits1,250,000T. Credits1,250,000- &"Arial Rounded MT Bold,Regular"&16ENTERPRISE FUND - GENERAL LEDGER ActivityBusiness-Type Activities: Enterprise Funds - Electricity and WaterOperating Revenues Charges for Services Total Current Assets- Operating Expenses Salaries Supplies Depreciation Total Operating ExpensesNoncurrent Assets-Operting Income- Nonoperating Revenues (Expenses) Interest ExpenseExpenses entered as negative amountsIncome before Contributions-Capital ContibutionsChange in Net Position-Net Position, January 1, 2091-Net Position, December 31, 2091$ - PROVINCE OF EUROPA STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET POSITION PROPRIETARY FUNDS FOR THE YEAR ENDED DECEMBER 31, 2091

- 4. Balance SheetBusiness-Type Activities: Enterprise Funds - Electricity and WaterAssetsCurrent AssetsCashCustomer Accounts Receivable (gross) Less: Allowance Uncollectible AccountsDue from General FundInventories Total Current Assets-Noncurrent AssetsBuildings and Structures Less: Accumulated DepreciationEquipment and Machinery Less: Accumulated DepreciationGeothermal Generators Less: Accumulated Depreciation Total Noncurrent Assets- Total Assets$ -LiabilitiesCurrent LiabilitiesAccounts PayableContracts Payable Interest PayableShort Term Note Payable Total Current Liabilities-Noncurrent LiabilitiesRevenue Bonds Payable Total Noncurrent Liabilities- Total Liabilities-Net PositionNet Investment in Capital Assets-Unrestricted- Total Net Position$ - PROVINCE OF EUROPA STATEMENT OF NET POSITION PROPRIETARY FUNDS AS OF DECEMBER 31, 2091 Cash FlowBusiness-Type Activities: Enterprise Funds - Electricity and WaterCash Flows from Operating Activities Cash Received from Customers Cash Paid for Supplies Cash Paid to EmployeesNet Cash Provided by Operating Activities- Cash Flows from Non-Capital Related Financing Activities Borrowing for OperationsNet Cash Provided by Non-Capital Related Financing Activities-Cash Flows from Capital Related Financing Activities Acquisition of Capital Assets Contributed Capital from General FundNet Cash Used in Capital Related Financing Activities- Cash Flows from Investing ActivitiesNet Cash Provided from Investing Activities-Net Increase in Cash- Cash and Cash Equivalents, January 1, 2091-Cash and Cash Equivalents, December 31, 2091$ -Reconciliation of Operating Income to Net Cash Provided by Operating Activities Operating IncomeAdjustments to Reconcile Operating Income to Net Cash

- 5. Provided by Operating Actitities Depreciation (Increase) Decrease in Customer Accounts Receivable- net (Increase)Decrease in Interfund Receivables (Increase) Decrease in Inventories Increase (Decrease) in Accounts PayableNet Cash Provided by Operating Activities$ -Noncash Investing, Capital and Non-capital Related Financing Activities Acquisition of building through contracts payable PROVINCE OF EUROPA STATEMENT OF CASH FLOWS PROPRIETARY FUNDS FOR THE YEAR ENDED DECEMBER 31, 2091 General Fund#dateJournal Entriesdebitscredits CASH1Jan. 1Encumbrances11,806bb18,000ALLOWANCE FOR Budgetary Fund Balance Reserve for Encumbrances11,806TAXES RECEIVABLEUNCOLLECTIBLE TAXES SUPPLIESadditional debit accountTo re-establish outstanding encumbrances bb--bbbb13,000--13,000-18,000 SHORT-TERM DUE TO (total)additional credit accountACCOUNTS PAYABLE NOTE PAYABLEOTHER FUNDSFUND BALANCE-bb-bb-bb31,000bb----31,000FEES, LICENSES &INTERGOVERNMENTALEDUCATION PROGRAM RESERVE FOR ENCUMBRANCESPROPERTY TAX REVENUESALES TAX REVENUEPERMITS REVENUE REVENUESFEE REVENUE-----GENERAL GOVERNMENTPUBLIC SAFETYEDUCATIONOTHER FINANCINGOTHER FINANCING USES EXPENDITURESEXPENDITURESEXPENDITURES SOURCESTRANSFERS OUT-----BUDGETARY ACCOUNTSESTIMATED OTHER BUDGETARYESTIMATED REVENUESAPPROPRIATIONSFINANCING USESFUND BALANCE---- BUDGETARY FUND BALANCEENCUMBRANCES RESERVE FOR

- 6. ENCUMBRANCES-bb111,80611,806111,80611,806T. Debits42,806T. Credits42,806- &"Arial Rounded MT Bold,Regular"&18General Fund - General Ledger Debt Service#dateJournal EntriesdebitscreditsDEBT SERVICE FUND GENERAL LEDGERtype accounts to be debited heretype accounts to be credited here CASHFUND BALANCEbb--bb--OTHER FINANCING SOURCES EXPENDITURESEXPENDITURES TRANSFERS INBOND PRINCIPALBOND INTEREST---T. Debits-T. Credits- Capital Projects#dateJournal EntriesdebitscreditsCAPITAL PROJECTS FUND GENERAL LEDGERtype accounts to be debited heretype accounts to be credited hereDUE FROM OTHER CASH FUNDSCONTRACTS PAYABLEbb- bb--bb--- (Beginning) CAPITALOTHER FINANCING USESFUND BALANCEEXPENDITURESTRANSFERS OUT- bb---OTHER FINANCING SOURCESOTHER FINANCING SOURCESOTHER FINANCING SOURCES TRANSFERS INPROCEEDS OF BONDSPREMIUM ON BONDS--- BUDGETARY ACCOUNTS BUDGETARY FUND BALANCE RESERVE FOR ENCUMBRANCESENCUMBRANCES-bb--T. Debits-T. Credits- Account Groups#dateJournal EntriesdebitscreditsGENERAL FIXED ASSET ACCOUNT GROUPtype accounts to be debited heretype accounts to be credited hereCONSTRUCTIONBUILDINGS & STRUCTEQUIPMENT IN PROCESSbb1,395,000bb480,000bb-1,395,000480,000- ACCUMULATED DEPRACCUMULATED DEPRINVESTMENT INBUILDINGS & STRUCTEQUIP & MACHINERYGEN. FIXED ASSETSbbbb1,875,000bb-- 1,875,000GENERAL LONG-TERM DEBT ACCOUNT GROUPAMOUNT TO BEPROVIDED FOR DEBTBOND PREMIUMBONDS PAYABLEbb1,875,000bb1,875,000bb1,875,000-1,875,000T.

- 7. Debits3,750,000T. Credits3,750,000 Activity StatementGeneralDebt ServiceCapital ProjectsTotal Governmental FundsRevenuesProperty Taxes$ -Sales Taxes- Fees, Licenses and Permits-Intergovernmental Revenues- Education Program Fee Revenues- Total Revenues---- ExpendituresCurrent: General Government Operations- Public Safety- Education-Capital Outlay-Debt Service- Principal- Interest- Total Expenditures----Excess (Deficiency) of Revenues Over Expenditures----Other Financing Sources (Uses)-Proceeds of Bonds-Premium on Bonds Sold-Transfers In-Transfers Out-Enter transfers out as negative and transfers in as positive amounts Total Other Financing Sources (Uses)----Net Change in Fund Balance----Fund Balance, January 1, 2091---Fund Balance, December 31, 2091$ -$ -$ -$ - PROVINCE OF EUROPA GOVERNMENTAL FUNDS STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE FOR THE YEAR ENDED DECEMBER 31, 2091 Balance SheetGeneralDebt ServiceCapital ProjectsTotal Governmental FundsAssetsCash$ -Taxes Reveivable - Gross - Less: Allowance uncollectibles taxes-Supplies Inventory- Total Assets$ -$ -$ -$ -Liabilities and Fund EquityLiabilitiesAccounts Payable$ -Contracts Payable-Short Term Notes Payable-Due to Other funds- Total Liabilities----Fund BalancesNonspendable - supplies-Committed - contractual obligations-Assigned for:- Debt Service- Capital Acquisitions-Unassigned- Total Fund Balance---- Total Liabilities and Fund Equity$ -$ - $ -$ - PROVICE OF EUROPA GOVERNMENTAL FUNDS BALANCE SHEET AS OF DECEMBER 31, 2091

- 8. Budget Budgeted AmountsOriginalFinalActual Amounts (Budgetary Basis)Variance with Final BudgetRevenuesProperty Taxes$ -Sales Taxes-Fees, Licenses and Permits- Intergovernmental Revenues-Education Program Fee Revenues- Total Revenues----ExpendituresCurrent year Expenditures & Encumbrances: General Government Operations- Public Safety- Education-- Total Expenditures----Excess (Deficiency) of Revenues Over Expenditures----Other Financing Sources (Uses)-Transfers Out- Total Other Financing Sources (Uses)----Net Change in Fund Balance$ -$ -$ -$ - Reconciliation:Excess of 2090 Reserved for Encumbrances over Related Actual Expenditure in 2091Reserve for encumbrances, December 31, 2091Unassigned Fund Balance, January 1, 2091Total fund balance less encumbrances at 12/31/2090Total fund balance, December 31, 2091$ - PROVINCE OF EUROPA STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE - BUDGET AND ACTUAL GENERAL FUND FOR THE YEAR ENDED DECEMBER 31, 2091 GOVERNMENTAL ACCOUNTING PRACTICE SET Part A due: Part B due: Introduction The date is December 31, 2091. You have just risen from a three month cryogenic sleep during which you traveled from Earth to Europa, the only inhabited moon of Jupiter. Europa has been colonized since the early 2060's. To encourage development the United Earth Council (roughly equivalent to a

- 9. federal government for the planet Earth) gave land grants to colonists willing to leave Earth and settle this new world. The Council also built a series of water purification and power generating plants. These plants utilize the natural geothermal resources of Europa to generate electrical power. Most of the inhabitants are engaged in the operation of the quarter million acre farms which span the temperate zones on either side of the equator. The labor is performed by robots through a centralized computer under the direction of the owner/farmer and family members. Harvests are transported by freighter to Earth. It is lonely, although profitable life with an average of 10 harvests per Earth year. All banking is performed on Earth through electronic funds transfers. A substantial business sector has developed, servicing the farming operations. After several decades of hard work the inhabitants of Europa are beginning to enjoy the rewards of their labors and are seeking some of the services which can only be provided by a local centralized government. They naturally sought to establish this government on Europa and petitioned the United Earth Council for admission to the Council as a member province (roughly equivalent to the 20th century state governments). Province status was granted by a vote of the Council and the citizens of Europa acted quickly to organize their new government, which officially began operations on January 1, 2091. One of the tasks facing the new government was to hire qualified people to carry on the day to day business of the government. You represent one of these people, having been highly trained in the subtleties of governmental accounting. Ownership of public facilities which were constructed by the United Earth Council (Buildings, roads & the electrical power utility) was transferred to the new province as of midnight on 12‑31‑2090. In return, the Province issued long‑term bonds

- 10. payable which provide for interest and principle payments to the United Earth Council over the next 20 years. Having no qualified governmental accountants on Europa, the province administrator has simply made notes summarizing the transactions which have occurred since the beginning of operations. Your task is to establish a fund accounting system, prepare summary journal entries recording all transactions, and prepare the year end 12‑31‑2091 financial statements for the Province. ** Report: Your completed projects should include (in this order): Part A: 1. Cover sheet with names of group members 2. Fund-basis financial statements, including a Budget Comparison Statement for the General Fund. 3. Ledgers (t-accounts) with journal entries for each fund and account group Part B: 1. Cover sheet with names of group members 2. Government-wide Financial Statements 3. Worksheets and journal entries for the governmental activities portion of the Government-wide financial statements Check figures: General fund cash:

- 11. $ 143,249 General fund unassigned fund balance 85,229 Governmental funds: Total fund balance 1,948,249 Enterprise fund cash: 69,500 Enterprise fund net position: 54,183 A set of Excel templates (Excel) are available for your use. Please turn in the printed copy of each worksheet. PROVINCE OF EUROPA Transaction list for the year ended December 31, 2091 Account Structure: Because the Province has a limited number of revenue sources, revenue control accounts are not used. Rather, General Fund revenues are directly recorded into the following accounts (property taxes, sales taxes, fees licenses and permits, program fees, and intergovernmental grants) Similarly, expenditures are recorded directly into the following accounts: (general government operations, public safety, education, capital outlay,

- 12. and debt service: principal and interest). The Province established the Bureau of Electricity and Water to operate as an enterprise fund. The enterprise fund reports expenses by object category using the following account titles: (salaries, supplies, depreciation, and interest). There are no fiduciary, special revenue, permanent, or internal service funds. The government uses account groups to record general fixed assets and general long-term debt. Beginning Balances: 1. At 12-31-2090, the remaining cash and supplies on hand in the government offices were transferred to the new Province government. The opening trial balance for the Province for 1-1- 2091 was as follows: GENERAL FUND trial balance Jan. 1, 2091 debitscredits Cash 18,000 Fund Balance: Supplies 13,000 Assigned (Reserved for encumbrances ) 11,806 _______ Unassigned

- 13. 19,194 31,000 31,000 The supplies were office supplies for general government operations. The reserve for encumbrances relates to a purchase order placed in December of 2090 for engineering services (see item # 7,below). The Province honors outstanding encumbrances from previous years and the encumbrance should be re-established for 2091. For purposes of the Budgetary Comparison Statement, amounts are charged to the budget in the year they are initially encumbered, regardless of when the expenditure is incurred. 2. On December 31, 2090, the United Earth Council (U.E.C.) transferred the fixed assets which have been constructed with U.E.C. funds. The Province Council assigned custody of these assets to the general Province government and the Bureau of Electricity and Water as follows: Useful Salvage Government Bureau Life Value Buildings, roads, and other structures $1,395,000 $ 450,000 10 $ 0 Equipment 480,000 150,000 5 0

- 14. Geothermal Generators 0 650,000 5 0 Total $1,875,000 $1,250,000 ========== ========== In return for these assets, the Province government issued $1,875,000, 10 percent general obligation serial bonds. Principal payments of $93,750 and interest payments on the bonds are to be paid at the end of each year starting on December 31, 2091. Similarly, the Bureau of Electricity and Water issued (at face value) $1,250,000, 10 percent long-term revenue bonds in exchange for the capital assets listed above. The bonds call for annual interest payments on January 1 and mature on January 1, 2101. Since these events occurred on the last day of 2090, they represent beginning balances for 2091. Current Year Transactions: 3. The government of the Europa Province established the Bureau of Electricity and Water. The Bureau of Electricity and Water is in charge of providing the power and water for residents and the Province government. On January 1, 2091, the Province government agreed to contribute $300,000 for establishment of the Bureau of Electricity and Water, and transferred cash on February 1, 2091. 4. On January 1, 2091, The Province Council approved budgets for 2091 as follows:

- 15. Budget Items Province Government (General Fund) Capital Additions Bureau of Electricity and Water Revenue and other financing sources Property Taxes Sales Taxes Fees, Licenses and Permits Charges for Services (Bureau) Program Fees: Education Intergovernmental grants Transfer from General Fund Proceeds from Bond Issues $3,720,000 750,000 250,000 70,000 470,000 $ 250,000 2,500,000 $3,250,000

- 16. 300,000 1,250,000 Budget continued on next page Expenditures/expenses and other financing uses: General government operations Public Safety Education Operating expenses (Bureau) Capital Outlays Transfers to other funds 1,500,000 1,400,000 1,250,000 850,000 2,750,000 3,000,000 1,875,000 5. On January 10, 2091, a cash grant of $450,000 was received from the United Earth Council for operation of the Province. The grant provisions stipulate the funds are to be used for general operations of the government. 6. On January 31, 2091, $3,700,000 in property taxes were

- 17. levied. Of this, $111,000 (3% of property taxes) is estimated to be uncollectible. The remaining tax bills are expected to be collected within 60 days following the end of the fiscal year. During 2091, $3,030,000 was collected and $104,000 are identified as uncollectible and written off. 7. On January 5, 2091 the engineering report ordered in December of the previous year (see item 1 above) was received along with an invoice for of $ 11,501. The invoice was immediately paid. The engineering report was for general government operations. 8. During 2091, the Province government placed orders amounting to $940,000 for supplies. All the supplies ordered were received during the year with an invoice price of $935,000 (there are no outstanding encumbrances for supplies). $900,000 was paid during the year. The supplies were distributed by major functions of government as follows: General Public Operation Safety Education Total Order placed $ 390,000 $ 400,000 $ 150,000 $ 940,000 Invoice prices 395,000 400,000 140,000 935,000 The government uses the consumption method of recording supplies – (i.e. expenditure is determined by the amount of supplies used – not purchased – during a period).

- 18. 9. During 2091 the Bureau of Electricity and Water placed orders amounting to $1,200,000 for supplies. The supplies were received with an invoice price of $1,100,000. Of this $1,045,000 was paid before year end. 10. The Province Council approved the construction of a new school building at an estimated cost of $2,750,000. The issuance of $2,500,000 in general obligation long-term bonds was authorized to finance the cost of construction. In addition, the Province government agreed to provide $250,000 for the construction project. 11. On March 31, 2091, the Province government transferred $250,000 to the school building capital project. 12. On April 1, 2091, $2,500,000 in 10 percent general obligation long-term bonds were issued for $2,580,000. The premium of $80,000 was reserved for redemption of the bonds while the principal was set aside for construction of the school. The bonds call for annual interest payments on March 31, and mature on April 1, 2111. 13. On June 1, 2091, the school building contract was awarded to the lowest bidder for $2,600,000, including planning and architect's fees. 14. On November 30, 2091, the progress billings of $1,250,000 for the school building were received from the contractor and $ 850,000 was paid on December 31, 2091. The remaining balance is expected to be paid in January, 2092. Liabilities resulting from capital additions are recorded in “Contracts Payable”, (rather than Accounts Payable). 15. The Board of the Bureau of Electricity and Water approved the construction of an office building at an estimated cost of

- 19. $880,000. 16. On July 1, 2091, the office building contract was signed in the amount of $865,000, including planning and architect's fees. 17. On October 30, 2091, construction was completed and $632,500 was paid on the contract. The remaining portion ($ 232,500) will be paid following final inspection on January 15, 2092. Liabilities resulting from capital additions are recorded in “Contracts Payable”, (rather than Accounts Payable) 18. At the end of November, ground transportation units were ordered for the public safety department at an estimated cost of $167,020. The units have not been delivered as of December 31, 2091. 19. During 2091, the Province government received the following cash collections: Sales taxes $ 838,000 Permits, fees & licenses 312,000 Program Fees: Education 80,000

- 20. $1,230,000 ========= 20. Salaries and wages of $4,150,000 were incurred and paid by the Province government and the Bureau of Electricity and Water during 2091. Salaries and wages are classified by governmental functions as follows: Incurred & Paid General operation $ 837,000

- 21. Public safety 775,000 Education 725,000 Bureau of Electricity Water 1,813,000 Total $ 4,150,000 ============ 21. During 2091, the Bureau of Electricity and Water billed the Province government and the residents for electricity and water services in the amounts of $920,000 and $2,120,000 respectively. The Bureau estimated that 2% of the gross revenue from the residents will be uncollectible. During 2091, $805,000 and $1,805,000 of the bills sent to the Province government and the residents, respectively, are collected.

- 22. $18,500 of the bills sent to the residents are identified as uncollectible and written off. The electricity and water services provided to the Province government were charged by government functions as follows: General operation $ 350,000 Public safety 320,000 Education 250,000 22. $281,250 was removed from general government funds and set aside for payments on outstanding general obligation serial bonds. 23. On December 31, 2091, the Province government made principal payment of $93,750 and annual interest of $187,500 on the general obligation serial bonds. 24. As of December 31, 2091, physical inventories of supplies on hand report the following: General operation

- 23. $ 116,000 Public safety 0 Education 0 Bureau of Electricity Water 14,000 25. On December 31, 2091, the Bureau of Electricity and Water accrued annual interest on the 10% bonds ($1,250,000 face value) described in item # 2. 26. The Province government and the Bureau of Electricity and Water recorded depreciation for 2091 using the straight-line method. The new office building is estimated to have zero salvage value and 10-year useful life and is depreciated on a monthly basis, beginning with the month (November) it was placed in service. 27. On December 31, 2091 the Bureau of Electricity and Water borrowed $650,000 on a 90 day note payable to cover a temporary cash shortfall. 28. On December 31, 2091, $300,000 was borrowed on a 60 day note payable to cover a temporary cash shortfall in general government operations. 29. The bond premium is amortized using the straight-line basis over 20 years. (9 months of amortization is recognized in

- 24. 2091). 30. For purposes of classifying fund balances in the governmental funds, assume: · Supplies are the only nonspendable resource, · The outstanding encumbrances in the capital project fund are classified as Committed by contractual obligation, · The outstanding encumbrances in the General Fund are classified as Assigned for capital asset acquisitions · The residual balances of the debt service and capital projects funds are classified as assigned. 31. Prepare closing entries, where appropriate Entries required for Government-wide financial statements. A review of the governmental type transactions for the year suggests the following worksheet journal entries are necessary for preparation of the Government-wide Statements: 1. The fixed assets and debt acquired in Transaction 2 should be entered in the beginning balances column on the worksheet. 2. Capital expenditures should be eliminated. 3. Depreciation expense should be recorded. 4. Bond proceeds should be eliminated. 5. The premium on the 20 year bonds in Transaction 12 should be amortized using the straight line method (9 months).

- 25. 6. Nine months of interest should be accrued on the bonds in transaction 12. 7. Interfund transfers should be eliminated, but not the portion paid to Business-type funds. 8. Expenditures for bond principal should be eliminated. �(Prepare the journal entries and enter them on the worksheet used to convert governmental funds to the accrual basis, but do not post the entries in the journals of the funds.) 1