Flash comment: Estonia - September 7, 2012

•

0 likes•300 views

Flash comment: Estonia - September 7, 2012: Economic growth in 2Q founded on domestic demand

Recommended

Recommended

More Related Content

What's hot

What's hot (16)

Viewers also liked

Viewers also liked (19)

Similar to Flash comment: Estonia - September 7, 2012

Similar to Flash comment: Estonia - September 7, 2012 (20)

More from Swedbank

More from Swedbank (20)

Recently uploaded

Recently uploaded (20)

Flash comment: Estonia - September 7, 2012

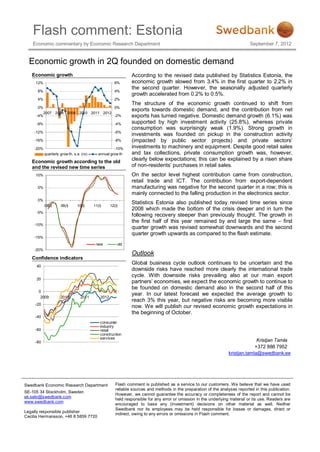

- 1. Flash comment: Estonia Economic commentary by Economic Research Department September 7, 2012 Economic growth in 2Q founded on domestic demand Economic growth According to the revised data published by Statistics Estonia, the 12% 6% economic growth slowed from 3.4% in the first quarter to 2.2% in the second quarter. However, the seasonally adjusted quarterly 8% 4% growth accelerated from 0.2% to 0.5%. 4% 2% The structure of the economic growth continued to shift from 0% 0% exports towards domestic demand, and the contribution from net 2007 2008 2009 2010 2011 2012 -4% -2% exports has turned negative. Domestic demand growth (6.1%) was -8% -4% supported by high investment activity (25.8%), whereas private consumption was surprisingly weak (1.9%). Strong growth in -12% -6% investments was founded on pickup in the construction activity -16% -8% (impacted by public sector projects) and private sectors’ -20% -10% investments to machinery and equipment. Despite good retail sales quarterly grow th, s.a. (rs) annual grow th and tax collections, private consumption growth was, however, Economic growth according to the old clearly below expectations; this can be explained by a risen share and the revised new time series of non-residents’ purchases in retail sales. 10% On the sector level highest contribution came from construction, retail trade and ICT. The contribution from export-dependent 5% manufacturing was negative for the second quarter in a row; this is mainly connected to the falling production in the electronics sector. 0% Statistics Estonia also published today revised time series since 08(I) 09(I) 10(I) 11(I) 12(I) 2008 which made the bottom of the crisis deeper and in turn the -5% following recovery steeper than previously thought. The growth in the first half of this year remained by and large the same – first -10% quarter growth was revised somewhat downwards and the second quarter growth upwards as compared to the flash estimate. -15% new old -20% Outlook Confidence indicators Global business cycle outlook continues to be uncertain and the 40 downside risks have reached more clearly the international trade cycle. With downside risks prevailing also at our main export 20 partners’ economies, we expect the economic growth to continue to be founded on domestic demand also in the second half of this 0 year. In our latest forecast we expected the average growth to 2009 2010 2011 2012 reach 3% this year, but negative risks are becoming more visible -20 now. We will publish our revised economic growth expectations in the beginning of October. -40 consumer industry -60 retail construction services -80 Kristjan Tamla +372 888 7952 kristjan.tamla@swedbank.ee Swedbank Economic Research Department Flash comment is published as a service to our customers. We believe that we have used reliable sources and methods in the preparation of the analyses reported in this publication. SE-105 34 Stockholm, Sweden However, we cannot guarantee the accuracy or completeness of the report and cannot be ek.sekr@swedbank.com held responsible for any error or omission in the underlying material or its use. Readers are www.swedbank.com encouraged to base any (investment) decisions on other material as well. Neither Swedbank nor its employees may be held responsible for losses or damages, direct or Legally responsible publisher indirect, owing to any errors or omissions in Flash comment. Cecilia Hermansson, +46 8 5859 7720