Flash comment: Estonia - September 8, 2011

•

0 likes•150 views

Flash comment: Estonia - September 8, 2011: GDP growth driven by exports and investments

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Flash comment: Estonia - September 8, 2011

Similar to Flash comment: Estonia - September 8, 2011 (20)

More from Swedbank

More from Swedbank (20)

Recently uploaded

Recently uploaded (20)

Flash comment: Estonia - September 8, 2011

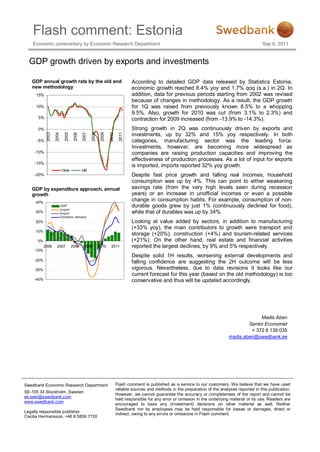

- 1. Flash comment: Estonia Economic commentary by Economic Research Department Sep 8, 2011 GDP growth driven by exports and investments GDP annual growth rate by the old and According to detailed GDP data released by Statistics Estonia, new methodology economic growth reached 8.4% yoy and 1.7% qoq (s.a.) in 2Q. In 15% addition, data for previous periods starting from 2002 was revised because of changes in methodology. As a result, the GDP growth 10% for 1Q was raised from previously known 8.5% to a whopping 9.5%. Also, growth for 2010 was cut (from 3.1% to 2.3%) and 5% contraction for 2009 increased (from -13.9% to -14.3%). 0% Strong growth in 2Q was continuously driven by exports and investments, up by 32% and 15% yoy respectively. In both 2003 2004 2005 2006 2007 2008 2009 2010 2011 -5% categories, manufacturing sector was the leading force. Investments, however, are becoming more widespread as -10% companies are raising production capacities and improving the effectiveness of production processes. As a lot of input for exports -15% is imported, imports reported 32% yoy growth. new old -20% Despite fast price growth and falling real incomes, household consumption was up by 4%. This can point to either weakening GDP by expenditure approach, annual savings rate (from the very high levels seen during recession growth years) or an increase in unofficial incomes or even a possible 40% change in consumption habits. For example, consumption of non- GDP durable goods grew by just 1% (continuously declined for food), Import 30% Export while that of durables was up by 34%. Domestic demand 20% Looking at value added by sectors, in addition to manufacturing (+33% yoy), the main contributors to growth were transport and 10% storage (+20%), construction (+4%) and tourism-related services 0% (+21%). On the other hand, real estate and financial activities 2006 2007 2008 2009 2010 2011 reported the largest declines, by 9% and 5% respectively. -10% Despite solid 1H results, worsening external developments and -20% falling confidence are suggesting the 2H outcome will be less -30% vigorous. Nevertheless, due to data revisions it looks like our current forecast for this year (based on the old methodology) is too -40% conservative and thus will be updated accordingly. Madis Aben Senior Economist + 372 6 139 035 madis.aben@swedbank.ee Swedbank Economic Research Department Flash comment is published as a service to our customers. We believe that we have used reliable sources and methods in the preparation of the analyses reported in this publication. SE-105 34 Stockholm, Sweden However, we cannot guarantee the accuracy or completeness of the report and cannot be ek.sekr@swedbank.com held responsible for any error or omission in the underlying material or its use. Readers are www.swedbank.com encouraged to base any (investment) decisions on other material as well. Neither Swedbank nor its employees may be held responsible for losses or damages, direct or Legally responsible publisher indirect, owing to any errors or omissions in Flash comment. Cecilia Hermansson, +46 8 5859 7720