Downloaded 1,510 times

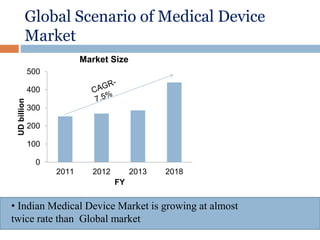

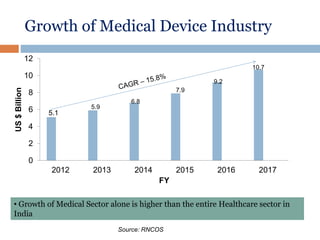

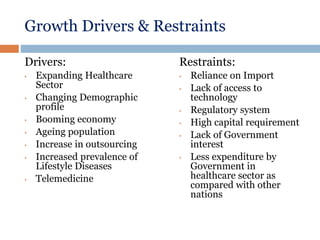

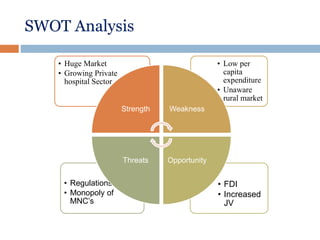

The document provides a comprehensive overview of the medical device sector in India, including its growth, market dynamics, regulatory environment, and comparison with the global market. It highlights that India's medical device market is expected to grow at a faster rate than the overall healthcare sector, driven by various factors such as technological advancements and increasing healthcare needs. The summary also outlines device classifications and discusses strengths, weaknesses, opportunities, and threats (SWOT) in the context of the Indian medical device industry.

![India Medical Devices Market: Industry Size and Growth Trends [2029] Analyzed...](https://cdn.slidesharecdn.com/ss_thumbnails/indiamedicaldevicesmarket-240528124717-7e7cbb30-thumbnail.jpg?width=640&height=640&fit=bounds)