Financial Leverage Definition, Advantages, and Disadvantages

Quarterly report on deposits september 2011 b

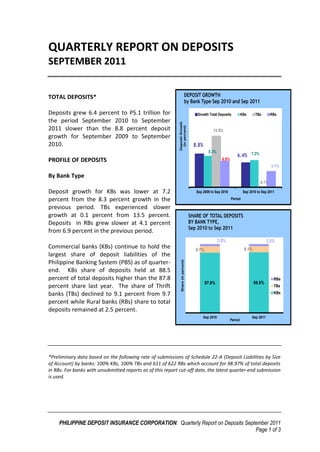

1. QUARTERLY REPORT ON DEPOSITS

SEPTEMBER 2011

TOTAL DEPOSITS* DEPOSIT GROWTH

by Bank Type Sep 2010 and Sep 2011

Deposits grew 6.4 percent to P5.1 trillion for Growth Total Deposits KBs TBs RBs

the period September 2010 to September

Deposit Growth

(in percent)

2011 slower than the 8.8 percent deposit 13.5%

growth for September 2009 to September

2010. 8.8%

8.3%

6.4% 7.2%

PROFILE OF DEPOSITS 6.9%

4.1%

By Bank Type

0.1%

Deposit growth for KBs was lower at 7.2 Sep 2009 to Sep 2010 Sep 2010 to Sep 2011

percent from the 8.3 percent growth in the Period

previous period. TBs experienced slower

growth at 0.1 percent from 13.5 percent. SHARE OF TOTAL DEPOSITS

Deposits in RBs grew slower at 4.1 percent BY BANK TYPE,

Sep 2010 to Sep 2011

from 6.9 percent in the previous period.

2.5% 2.5%

Commercial banks (KBs) continue to hold the 9.7% 9.1%

largest share of deposit liabilities of the

Philippine Banking System (PBS) as of quarter-

Share (in percent)

end. KBs share of deposits held at 88.5

percent of total deposits higher than the 87.8 RBs

87.8% 88.5%

percent share last year. The share of Thrift TBs

banks (TBs) declined to 9.1 percent from 9.7 KBs

percent while Rural banks (RBs) share to total

deposits remained at 2.5 percent.

Sep 2010 Sep 2011

Period

*Preliminary data based on the following rate of submissions of Schedule 22-A (Deposit Liabilities by Size

of Account) by banks: 100% KBs, 100% TBs and 611 of 622 RBs which account for 98.97% of total deposits

in RBs. For banks with unsubmitted reports as of this report cut-off date, the latest quarter-end submission

is used.

PHILIPPINE DEPOSIT INSURANCE CORPORATION: Quarterly Report on Deposits September 2011

Page 1 of 3

2. By Deposit Type

Savings deposits continue to dominate the type of deposit products and increasing its

share of deposits at 47.8 percent from 46.2 percent for the same period last year. The

share of Time and LTNCD deposits contracted to 32.6 percent from 35.2 percent while

the share of Demand & NOW deposits increased to 19.5 percent from 18.6 percent of

the total.

SHARE PER DEPOSIT TYPE DEPOSIT GROWTH by Deposit Type

TO TOTAL DEPOSITS, Sep 2010 to Sep 2011 Sep 2010 and Sep 2011

Demand & NOW Savings Time Total

Time/LTNCD Savings Demand & NOW

12.1%

Deposit Growth

10.1%

(in percent)

8.3%

9.9%

8.8%

8.7%

35.2% 32.6%

6.4%

Share (in percent)

46.2% 47.8%

-1.3%

Period

18.6% 19.5%

Sep 2010 Sep 2011 Sep 2009 to Sep 2010 Sep 2010 to Sep 2011

Period

Demand and NOW deposits grew most at 12.1 percent for the period followed by

Savings deposits at 10.1 percent. Time deposits dragged growth of total deposits with a

contraction of 1.3 percent from a growth of 8.3 percent last year.

By Bank Type and Deposit Type

DEPOSIT GROWTH by Bank Type and Deposit Type RBs posted the highest growth rate for

Sep 2010 and Sep 2011

Demand & NOW deposits with 14.6

Demand & NOW Savings Time percent, while growth rate for Time and

LTNCDs was at 14.4 percent. However,

15.6%

14.6%

there was a 1.0 percent contraction in

14.4%

13.5%

12.6%

12.0%

Savings for the period September 2010 to

10.1%

Deposit Growth

9.8%

(in percent)

8.3%

7.4%

September 2011.

6.9%

5.9%

4.4%

1.2%

0.9%

TBs experienced growth of 4.4 percent for

-2.8%

-1.0% Time and LTNCDs, Demand & NOW grew

by 1.2 percent while Savings deposits,

-7.2%

contracted by 7.2 percent.

KBs TBs RBs KBs TBs RBs

Sep 2009 to Sep 2010 Sep 2010 to Sep 2011

Period

PHILIPPINE DEPOSIT INSURANCE CORPORATION: Quarterly Report on Deposits September 2011

Page 2 of 3

3. On the other hand, KBs posted growth for

Demand & NOW deposits at 12.6 percent, SHARE PER DEPOSITOR TYPE

Savings at 12.0 percent and contraction of TO TOTAL DEPOSITS

Sep 2010 to Sep 2011

2.8 percent for Time deposits and LTNCDs.

Non- OBUs OBUs Trust Departments

Individuals Private Corporations Banks

Government

By Depositor Type 1.1%

1.1%

59.5% 54.8%

By September 2011, deposits of Individuals

Share (in percent)

account for 54.8 percent of total deposits,

lower than the 59.5 percent for the

preceding year. The share of Private

Corporations’ deposits increased to 30.2 27.2%

30.2%

percent from 27.2 percent while 10.2% 0.9% 11.4%

1.1%

Government deposits share was up at 11.4

Sep 2010 Sep 2011

percent from 10.2 percent of total deposits Period

for the comparative period.

INSURED DEPOSITS AND THE DEPOSIT INSURANCE FUND

As of end September 2011, deposits Domestic Deposit Liabilities - Philippine Banking System

that are P10,000 and below comprise (Am ounts in MIllion; Accounts in Thousand)

as of September 2011

74.4 percent of total deposits in

terms of number of accounts, but is

Grand Total

only 0.7 percent of total deposits in DEPOSIT SIZE

% to % to

terms of amount. On the other end Account Total Amount Total

of the deposit range, deposits over

P 5,000 & Below 28,588 68.2% 17,275 0.3%

P2.00 million are only 0.8 percent of

P 5,000.01 - P10,000 2,583 6.2% 18,046 0.4%

total deposits in terms of total P 10,000.01 - P15,000 1,556 3.7% 18,466 0.4%

accounts, but takes up 67.5 percent P 15,000.01 - P 40,000 2,815 6.7% 70,188 1.4%

of deposits in terms of amount. P 40,000.01 - P 60,000 1,344 3.2% 64,182 1.3%

P 60,000.01 - P 80,000 639 1.5% 44,071 0.9%

P 80,000.01 - P 100,000 494 1.2% 44,482 0.9%

With the Maximum Deposit P 100,000.01 - P 150,000 913 2.2% 108,964 2.1%

Insurance Cover (MDIC) at P500,000, P 150,000.01 - P 200,000 479 1.1% 82,835 1.6%

total insured deposits as of P 200,000.01 - P 250,000 407 1.0% 90,301 1.8%

P 250,000.01 - P 300,000 260 0.6% 71,295 1.4%

September 2011 stand at P1.47

P 300,000.01 - P 400,000 368 0.9% 125,022 2.5%

trillion, with 97.2 percent of total P 400,000.01 - P 500,000 301 0.7% 136,601 2.7%

accounts fully-insured and only 2.8 P 500,000.01 - P 750,000 363 0.9% 213,249 4.2%

percent of accounts partially insured. P 750,000.01 - P 1,000,000 173 0.4% 153,278 3.0%

P1,000,000.01 - P1,500,000 211 0.5% 245,963 4.8%

P1,500,000.01 - P2,000,000 83 0.2% 143,862 2.8%

The DIF stands at P67.0 billion as of Ov er P 2,000,000 337 0.8% 3,429,300 67.5%

September 2011, which is sufficient

Total 41,914 100.0% 5,077,378 100.0%

to cover 4.5 percent of the P1.47

trillion total insured deposits.

PHILIPPINE DEPOSIT INSURANCE CORPORATION: Quarterly Report on Deposits September 2011

Page 3 of 3