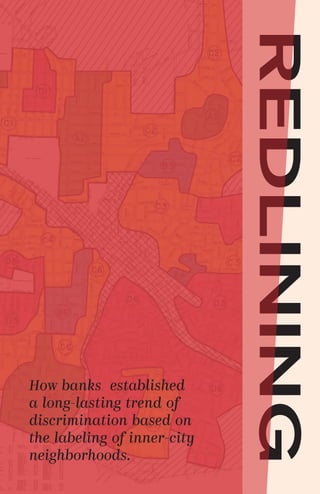

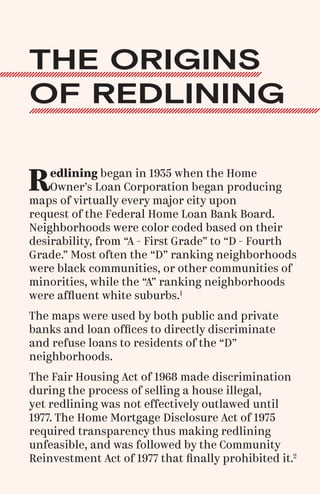

The document discusses the practice of redlining, a discriminatory method used by banks in the 1930s to deny loans to communities of color, resulting in long-lasting socioeconomic impacts. Despite the Fair Housing Act of 1968 and the Community Reinvestment Act of 1977 aiming to curb such discrimination, practices continue through insurance and retail redlining, negatively affecting urban minority communities. The combination of these factors contributes to increased poverty and criminalization in these areas, perpetuating inequities across generations.