This corporate presentation was prepared by IDBI Bank for general information purposes regarding the bank and its subsidiaries. It provides an overview of IDBI Bank, including its establishment and evolution over time, current business segments and distribution reach, and key recent business highlights showing improved financial performance. The presentation also outlines IDBI Bank's role in developing the financial sector through its investments in subsidiaries. It notes the sustained capital support provided by major shareholders the Government of India and LIC.

![Page 12

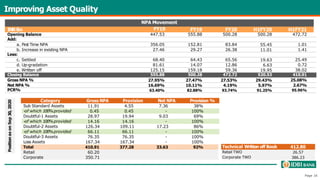

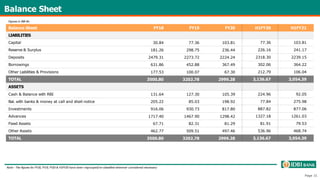

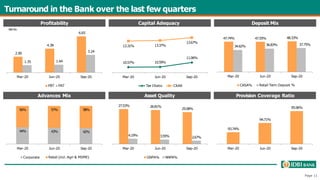

Improving Financial Position

Total Net Interest Income Profit After Tax

Operating Profit

Net Interest Margin[1] Cost-Income Ratio

56.40 59.06

69.78

30.89 34.69

FY18 FY19 FY20 H1FY20 H1FY21

79.09

40.52

51.12

19.60

25.72

FY18 FY19 FY20 H1FY20 H1FY21

(82.38)

(151.16)

(128.87)

(72.60)

4.69

FY18 FY19 FY20 H1FY20 H1FY21

37.51%

55.98% 55.35%

60.43%

53.60%

FY18 FY19 FY20 H1FY20 H1FY21

1.81%

2.03%

2.61%

2.23%

2.76%

FY18 FY19 FY20 H1FY20 H1FY21

Return Ratios

INR Bn

INR Bn

INR Bn

1. Net interest margin is the difference of interest earned and interest expended divided by average interest-earning assets

2. Return on Assets is profit after tax / average assets

3. Return on Equity is profit after tax / networth (excluding revaluation reserve & intangible assets)

-2.46%

-4.68% -4.26% -4.75%

0.32%

FY18 FY19 FY20 H1FY20 H1FY21

-58.30%

-155.20%

-128.25%

-163.39%

7.59%

FY18 FY19 FY20 H1FY20 H1FY21

RoA[2]

RoE[3]](https://image.slidesharecdn.com/bankingserviceandoperation-231214171010-6743fe84/85/Banking-service-and-operation-pptx-12-320.jpg)

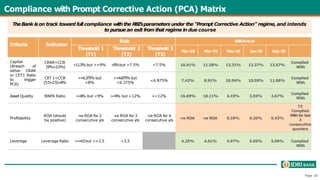

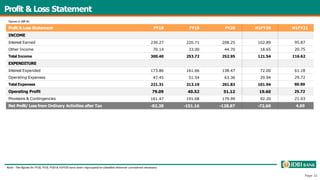

![Retail Focused Asset Book

Gross Advances Yield on Advances[1]

Gross Advances Mix

55.44%

44.56%

Corporate Retail

41.55%

58.45%

1,988.53

1,820.97 1,716.90 1,768.68

1,638.41

FY18 FY19 FY20 H1FY20 H1FY21

Structured Retail Advances

458.46

540.34

591.38 563.20 593.51

FY18 FY19 FY20 H1FY20 H1FY21

H1FY21

FY18

70.32%

23.46%

0.88% 3.44%

1.90%

HL LAP EL PL AL

72.39%

21.61%

1.02% 3.15%

1.83%

Structured Retail Advances Mix

H1FY21

FY18

Shift towards retail assets along with reduced corporate

exposure

INR Bn

INR Bn • The Bank intends to capture an even larger

share of the retail banking space by

expanding its portfolio of retail banking

• Focus on Government initiated schemes such

as Guaranteed Emergency Credit Line, PM

SVANidhi), Agriculture Infra Fund, Credit

Guarantee Scheme for Sub-ordinated Debt

etc. for ramping up the portfolio.

• Tie-up with LICHFL-FSL as Corporate DSA for

sourcing under identified MSME/Agri product

1. Yield is Interest income on advances/average advances. Previous period ratios have been re-calculated considering re-grouping/re-classification impacts.

8.34%

8.81%

9.55%

9.14%

9.56%

FY18 FY19 FY20 H1FY20 H1FY21

Increasing Retail share leading to increasing Yield on

Page 13

Advances](https://image.slidesharecdn.com/bankingserviceandoperation-231214171010-6743fe84/85/Banking-service-and-operation-pptx-13-320.jpg)

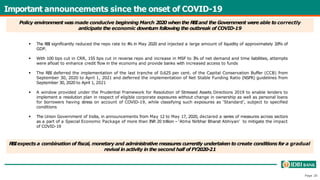

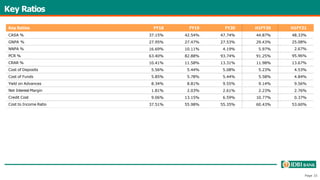

![Growing focus on low cost CASA Deposits

33.35% 25.39% 17.64% 21.84% 13.92%

66.65% 74.61% 82.36% 78.16% 86.08%

FY18 FY19

Bulk Deposits

FY20 H1FY20 H1FY21

Other Deposits

5.85% 5.78% 5.44% 5.58%

4.84%

5.56% 5.44% 5.08% 5.23%

4.53%

FY18 FY19 FY20

Cost of Funds

H1FY20 H1FY21

Cost of Deposits

Total Deposits & Borrowings

Cost of Deposits[1] & Cost of Funds[2]

Reduced dependence on Bulk Deposits

• The Bank aims to continue diversifying away

from its historic reliance on bulk deposits by

growing its low-cost CASA deposits

• Retail customer-specific orientation will

result in an increase in CASA deposits,

which will expand its pool of low-cost

funding

INR Bn

Increasing CASA focus

921.02 967.30 1,061.88 1,040.27 1,082.17

37.15%

42.54%

47.74%

44.87%

48.33%

FY18 FY20 H1FY20

CASA Ratio

H1FY21

FY19

CASA

INR Bn

631.86 452.88 367.49 302.06 364.22

2,479.31

2,273.72 2,224.24 2,318.30 2,239.15

FY18 FY19 FY20 H1FY20

Deposits

H1FY21

Borrowings

Customer Accounts

2.68 2.66 2.74 2.89

19.15 19.94

0.94 1.23

2.78

18.48 19.69

0.91 1.14

16.57

0.82

FY18 FY19

Current Accounts

FY20 H1FY20 H1FY21

Savings Account Term Deposit

Page 14

Mn

Consistent growth in Customer Accounts across types

1. Cost of deposits is Interest on deposits divided by average deposits

2. Cost of funds is interest expense divided by average interest-bearing liabilities (i.e. deposits & borrowings](https://image.slidesharecdn.com/bankingserviceandoperation-231214171010-6743fe84/85/Banking-service-and-operation-pptx-14-320.jpg)