This letter informs Mrs. Amanda Jones about upcoming changes to her company's pension scheme that will take effect on January 1, 2016. She has two options: 1) remain in the defined benefit section with an increased contribution rate of 8% of salary, or 2) transfer to the defined contribution section and continue contributing 4% of salary. The letter provides estimates of Mrs. Jones' projected benefits and contributions under each option, as well as answers to frequently asked questions, to help her decide which option best suits her needs for retirement. She must return a form selecting her choice by December 31, 2015.

1. Mr JasonEber

MACS Actuarial LLP

25 Watt Street

Edingow

EH1 2HW

Mrs AmandaJones

3 Imaginary Street

Glasburgh

G12 3AB

5 November2015

Dear Mrs Jones,

I am writingtoinformyou of changesto the Template ManufacturingPensionScheme (“the

Scheme”) thatwill be implementedon1 January2016. Approachingthisdate youmustmake a

decision betweentwooptionsthatwill affectyourfuture contributionsandthe benefitpayments

that resultfromthem;

Option 1 - RemaininDefinedBenefit(DB) sectionof the Scheme withanincreased

contributionrate of 8% of pensionable salary(currentcontributionrate 4%);or

Option 2 - Transferto the DefinedContribution(DC) sectionof the Scheme, andcontinueto

pay contributionsof 4%of pensionablesalary.

It isimportantthat youunderstandthe changes tothe Scheme will onlyaffectyourfuture service

benefits,andanypast service benefitswillbe valuedastheyare currently.

We hope thatthe followinginformationisusefulandthatit will helpyouplanforyourfuture. This

letterandthe supportingdocumentshave beendesignedtogive youaninsightintoyourprojected

benefitsunderbothoptionsavailable,tohelpyoudecide whichwouldsuityoubest.If youare still

unsure aboutwhichto choose,please seekadvice fromanIndependentFinancial Advisor(IFA)for

unbiasedadvice.Youcanfindan IFA nearyou at: https://www.unbiased.co.uk/

Scheme Changes

The changesbeingmade are to improve the robustnessof the Scheme’sabilitytopaythe full value

of benefitsthathave beenaccruedbyall members,andprotectthe Scheme fromadverse market

conditions. The changeswill alsoensure thatthe Scheme will be able toprovidebenefitsforfuture

service.

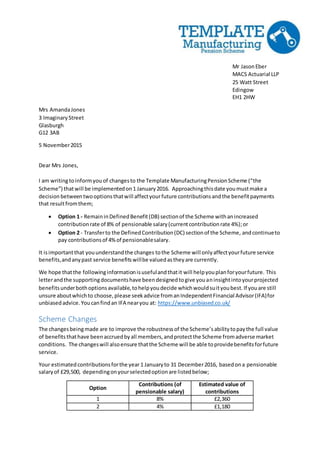

Your estimatedcontributionsforthe year1 Januaryto 31 December2016, basedona pensionable

salaryof £29,500, dependingonyourselectedoptionare listedbelow;

Option

Contributions (of

pensionable salary)

Estimated value of

contributions

1 8% £2,360

2 4% £1,180

2. Further Options

If you decide totransfertothe DC sectionyouwill be able toinfluence the balance betweensecurity

and investmentgrowth.Youwill be able tochoose froma selectionof premadeinvestment

strategieswithvaryinglevelsof investmentreturn.

Option Assetsinvestedin Expected

investmentreturn

Volatility

Growth Growth assets* High High

Balanced UK Gilts,Growth

Assets*

Medium Medium

Secure UK Gilts Low Low

* asset classes which areexpectedto return more than gilt yields over thelonger term.

You can alsoopt to investinthe Scheme’s‘Lifestyle’option,whichwill investinitiallyinthe ‘Growth’

optionandthen graduallylowerthe investmentriskof yourinvestmentsasyouapproachretirement

to ensure the value of yourcontributionsismaintained. Thisisthe Scheme’sdefaultoptionandwill

be the initial strategyyouwillbe enteredintoshouldyounotchoose another. Anillustrationof the

expectedinvestmentstrategyunderthe ‘Lifestyle’optionisgivenbelow;

You will findanattachedbenefitstatementthatwill outline yourannual contributionsand expected

benefitsunderbothoptions.

Alsoattachedisa form,detailingwhichoptionyouwouldlike toselect,whichmustbe returned to

the company by 31 December2015 (Please note thatthere will be nofurtheropportunitiesto

transferbetweensectionsof the Scheme afterthe deadline).

KindRegards,

Jason Eber

MACS Actuarial LLP

0%

20%

40%

60%

80%

100%

10 9 8 7 6 5 4 3 2 1

Years to retirement

Secure

Balanced

Growth

3. Benefit Statement

Option 1: Defined Benefit Section

If you choose to remaininthe DefinedBenefit Scheme,we have estimated yourbenefitsinline with

our salaryscale assumptionsanddefiningFinal Pensionable Salaryas the average of yourfinal three

yearsworking.Yourestimatedbenefitsforretiringatage 60 and 65 are includedbelow:

Retirementat 60:

1 January 2041

Retirementat 65:

1 January 2046

Past Service £15,484 £18,860

Future Service £27,650 £42,097

Total Income per annum £43,134 £60,957

Option 2: Defined Contribution Section

If you choose to move tothe DefinedContributionsectionof the Scheme,the benefitsthatyouhave

accrued inrelationto past service willbe paidasa DB pensionandyourfuture contributionswillbe

paidas a DC pension.We assume yourfuture DCcontributionsgaininvestmentreturnsof 5% each

yearto estimate yourpensionandaspart of a DC sectionyouwill be entitledtotake 25% of your DC

pot tax free.BelowIhave included;anestimate of the valuationof youraccruedbenefits if youtake

the full tax free lumpsum,andalternativelyif youdecide totake none of it:

Retirementat 60:

1 January 2041

Retirementat 65:

1 January 2046

Lump Sum (minimum) £0 £0

Past Service £15,484 £18,860

Future Service £10,856 £19,855

Total Income per annum £26,340 £38,715

OR

Lump Sum (maximumtax-free) £34,712 £54,852

Past Service £15,484 £18,860

Future Service £8,142 £14,891

Total Income per annum £23,626 £33,751

4. Leaving Service Benefit

If you decide toleave the Scheme atanygiventime,youare still entitledtothe pastservice benefits

youhave accrued, whenyouretire.Includedbeloware the valuesyoucouldreceiveatretirement,if

youwere to leave atage 40 or 45:

Date of Leaving Pensionreceivedat age 65

Age 40: 1 January2016 £10,841

Age 50: 1 January2021 £12,983

Death Benefit

Under bothsectionsof the Scheme youwill be entitledto5timesyoursalaryas a deathbenefit

before retirement.If youselect totransfertothe DC sectionandyourfundis worthmore than 5

timesyoursalary,youare entitledtothislargervalue instead.The value of the benefitsyoucouldbe

expectedtoreceive atages40 and 45:

Date of Death Death BenefitReceived

Age 40: 1 January2016 £147,500

Age 50: 1 January2021 £184,707

5. Frequently Asked Questions

What if I don’t like either of the options available, I want things to stay

as they are?

To remainin the Scheme youmust make a decisionbetweenthe twooptions. These changesare

beingmade toincrease the securityof The Scheme includingyourownpensionplan.

Will there be other opportunities to transfer between the new

sections?

After1 January 2016 youwill notbe able to transferbetweenthe twosectionsof the scheme.

Can I take my benefits now from the Defined Benefit section and

move to the Defined Contribution section for future service?

No,your pastservice will remaininthe scheme,aspart of the definedbenefitsection, until you

retire.

Can I transfer all of my benefit entitlements into the Defined

Contribution section?

No,your pastbenefitswill remainastheyare.If youwere to move tothe definedcontributions

sectionthenonlyyourfuture service benefitswouldbe calculatedonthisbasis.

Will the Company guarantee that the Defined Contribution section

will be better for me?

The company cannotguarantee thatthe Defined Contribution sectionwillbe betterforany

individual.The value of yourpensionatretirementisnotguaranteedinthe same mannerasthe

DefinedBenefitsectionandthe variationinthe investmentreturnsmayresultinahigheror lower

pensionentitlementonretirement.

Will this change affect my state pension entitlements?

No,your state pensionentitlementswill notbe affectedbythischange.The state pensionis

completelyseparate fromretirementbenefitsofferedbythe TemplateManufacturingPension

Scheme.

Who can I contact if I still have questions?

An IndependentFinancialAdvisor(IFA) wouldbe the mostuseful contactastheywill be able tooffer

youtailoredadvice andhelpyouconclude whichchoice wouldsuityoubest.Youmayfindan IFA

nearyou at the followingaddress: https://www.unbiased.co.uk/

6. Please complete and hand in thisform by the 31 December2015

Option 1

RemaininDefinedBenefitsectionof the

scheme,withincreased of 8%of

pensionable salary.

Option 2

Transferto the DefinedContribution

sectionof the scheme,and continue topay

contributions of 4%of pensionable salary.

If Option2 has beenselected,please selectaninvestmentstrategy:

Secure Balanced Growth Lifestyle

(Default)

Name: _______________________________________________________________________

Signature: ___________________________________________ Date: __________________