Public Startup Company "Re-Repo" Startup Capital Formation Model

•Download as ODP, PDF•

0 likes•1,040 views

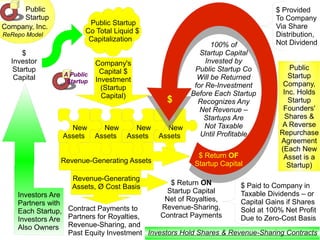

Reverse Repurchase Agreements might become the standard of practice in startup capital formation and startup tax accounting. This concept properly balances the competing interests of all stakeholders, including tax authorities, to solve a core problem with startup finance. Without Reverse Repurchase Agreements between startups and seed capital investors cash payments to investors are usually mistakenly accounted for as taxable dividends long before the investor has realized any actual return on investment. With Re-Repos, startups will be able to make cash distributions to early investors and account properly for this return OF capital until such payments become a return ON capital.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (9)

Similar to Public Startup Company "Re-Repo" Startup Capital Formation Model

Similar to Public Startup Company "Re-Repo" Startup Capital Formation Model (20)

More from Jason Coombs

More from Jason Coombs (20)

Recently uploaded

Recently uploaded (20)

Public Startup Company "Re-Repo" Startup Capital Formation Model

- 1. New Assets Company's Capital $ Investment (Startup Capital) Revenue-Generating Assets $ Investor Startup Capital Public Startup Co Total Liquid $ Capitalization New Assets New Assets New Assets $ 100% of Startup Capital Invested by Public Startup Co Will be Returned for Re-Investment Before Each Startup Recognizes Any Net Revenue – Startups Are Not Taxable Until Profitable $ Return OF Startup Capital $ Return ON Startup Capital Net of Royalties, Revenue-Sharing, Contract Payments Revenue-Generating Assets, Ø Cost Basis Contract Payments to Partners for Royalties, Revenue-Sharing, and Past Equity Investment $ Provided To Company Via Share Distribution, Not Dividend Public Startup Company, Inc. Holds Startup Founders' Shares & A Reverse Repurchase Agreement (Each New Asset is a Startup) $ Paid to Company in Taxable Dividends – or Capital Gains if Shares Sold at 100% Net Profit Due to Zero-Cost Basis Investors Hold Shares & Revenue-Sharing Contracts Public Startup Company, Inc. ReRepo Model Investors Are Partners with Each Startup, Investors Are Also Owners AA PPuubblliicc SSttaarrttuupp