Recommended

More Related Content

Similar to 4.pdf

Similar to 4.pdf (20)

Recently uploaded

Recently uploaded (20)

4.pdf

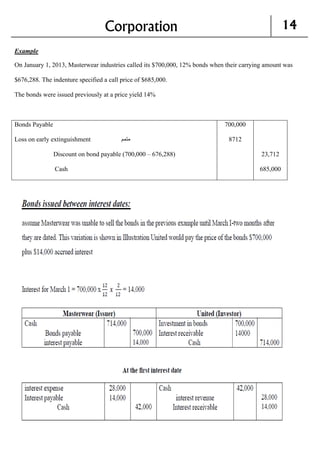

- 1. Corporation 14 Example On January 1, 2013, Masterwear industries called its $700,000, 12% bonds when their carrying amount was $676,288. The indenture specified a call price of $685,000. The bonds were issued previously at a price yield 14% Bonds Payable Loss on early extinguishment متمم Discount on bond payable (700,000 – 676,288) Cash 700,000 8712 23,712 685,000

- 2. Corporation 15 Problem (1): On January 1, 2011, Piper Co. issued ten-year bonds with a face value of $1,000,000 and a stated interest rate of 10%, payable semiannually on June 30 and December 31. The bonds were sold to yield 12%. Instructions (a) Calculate the issue price of the bonds. (b)Prepare the amortization table for 2011, assuming that amortization is recorded on interest payment dates (c) Prepare journal entry for piper co. for year 2011 Solution P= 1,000,000 stated rate = 10% 2 = 5% Market rate = 12% 2 = 6% N= 10 x 2 = 20 Maturity value of bonds payable 1,000,000 Present value of principle Principle x P.V. $1 (n=20 i=6%) 1,000,000 X 0.3118 Present value of interest payable Interest x P.V.O.A (n=20 i=6%) (1,000,000 x 5%) = 50,000 X 11.4699 311,800 573,495 proceeds from sale of bonds 885,295 = Discount on bonds payable 114705 Date Cash Paid Interest Expense (6%) Discount Amortized Carrying amount of Bonds 1/1/2011 885,295 30/6/2011 50000 53,117.7 3,117.7 888,412 31/12/2011 50000 53,304.7 3,304.7 891716 Piper Co. (Issuer) (Jan. 1) Cash Discount on bonds Bond payable 885,295 114705 1,000,000 July 1, interest expense Discount on bond Cash 53,117.7 3,117.7 50,000 Dec 1, interest expense Discount on bond Cash 53,304.7 3,304.7 50,000

- 3. Corporation 16 Problem (2): Grider Industries, Inc. issued $6,000,000 of 8% debentures on May 1, 2010 and received cash totaling $5,323,577. The bonds pay interest semiannually on May 1 and November 1. The maturity date on these bonds is November 1, 2018. The firm uses the effective-interest method of amortizing discounts and premiums. The bonds were sold to yield an effective-interest rate of 10%. Instructions Calculate the total dollar amount of discount or premium amortization during the first year (5/1/10 through 4/30/11) these bonds were outstanding. Solution P= 6,000,000 stated rate = 8% 2 = 4% Market rate = 10% 2 = 5% selling price = 5,323,577 Date Cash Paid (6,000,000 x 4%) Interest Expense (5%) Discount Amortized Carrying amount of Bonds 1/5/2010 $5,323,577 1/11/2010 240,000 266,178 26,178 5,359,755 1/5/2011 240,000 267,487 27,487 5,387,242 Piper Co. (Issuer) 1/5/2010 Cash Discount on bonds Bond payable 5,323,577 676,423 6,000,000 1/11/2011, interest expense Discount on bond Cash 266178 26,178 240,000 31/12/2010 interest expense 5,359,755 x 5% x 2 6 interest payable 89,329 89,329 1/5/2011 Interest payable Interest expense (267,487 – 89,329) Discount on bonds Cash 89,329 178,158 27,487 240,000