1. President’s Message

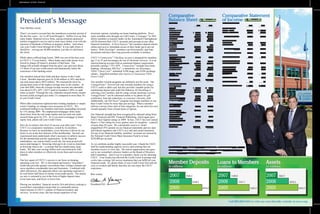

Comparative Statement

of Income (In Thousands)

Call 800-288-6423 or visit our user-friendly website at uecu.org.

$446.4

$530.9

$678.6 $220.3

$169.8

$191.7

$563.7

$679.2

$835.9

Best wishes,

President/CEO

INTEREST INCOME

Interest on Loans $ 13,258 $ 12,846

Interest on Investments 26,754 20,403

Total Interest Income 40,012 33,249

INTEREST EXPENSE

Dividends Paid 15,906 16,632

Borrowed Funds 1,648 1,102

Total Interest Expense 17,553 17,734

NET INTEREST INCOME 22,459 15,515

Provision for Loan Losses 1,145 1,052

Net Interest Income After

Provision for Loan Losses 21,314 14,463

Non-Interest Income 1,657 1,420

Operating Expenses 10,676 8,950

Non-Operating Income

(Expense), Net (2,767) (266)

Net Income Before Taxes 9,528 6,667

Federal Income Taxes (25) 18

NET INCOME AFTER TAXES $ 9,553 $ 6,649

2009 2008

ASSETS:

Loans to Members:

Secured Vehicle $ 42,421 $ 42,756

Other Personal 14,094 13,548

Real Estate Secured 146,572 120,126

Credit Card 17,165 15,269

Total Portfolio Loans 220,252 191,699

Loan Participations

Purchased - 686

Total Loans 220,252 192,385

Allowance for Losses (1,580) (1,271)

Net Loans 218,672 191,114

Investments:

Overnight Investments 17,482 7,222

U.S. Government

Agency Securities 9,239 31,736

Mortgage-Backed Securities 538,114 412,653

Mutual Funds 10,138 -

Other Investments 9,504 10,362

Total Investments 584,477 461,973

Deposit - NCUSIF 6,064 4,658

Other Assets 26,717 21,418

TOTAL ASSETS $ 835,931 $ 679,162

LIABILITIES AND EQUITY

Member Deposits:

Checking $ 12,106 $ 6,208

Money Market Savings 352,528 226,109

Share/Special Savings 209,892 215,101

Individual Retirement

Accounts 55,849 40,211

Certificates of Deposit 48,181 43,238

Total Member Deposits 678,557 530,867

Notes Payable and

Other Liabilities 39,992 50,067

Members' Equity 108,067 98,513

Unrealized Gain(Loss) on

Available-for-Sale

Securities, Net 11,743 2,469

Accumulated Other

Comprehensive Income (2,428) (2,755)

TOTAL LIABILITIES

AND EQUITY $ 835,931 $ 679,162

Comparative

Balance Sheet (In Thousands)

2009 2008

2007 2007 2007

December 31 Year Ended December 31

Dear Member-owner,

There’s no need to recount here the tumultuous economic period of

the last few years – we’ve all lived through it. Suffice it to say that

many banks, financial service firms, and government-sponsored

entities struggled to survive and in some cases failed, even with the

injection of hundreds of billions in taxpayer dollars. And where

was your Credit Union through all of this? It was right where it

should be – serving our 40,000 members, just like we did before

the storm.

While others suffered huge losses, 2009 was one of the best years

in UECU’s 75-year history. Many banks and credit unions were

forced to charge off massive amounts of bad loans. Our

charge-offs actually dropped from the prior year and were about

1/3 those of our peer credit unions and dramatically below the

experience of the banking sector.

Our members placed their faith and their money in the Credit

Union. Member deposits grew by $148 million or 28% and drove

our total assets above $835 million. We returned the favor by

paying them some of the highest savings rates in the country. At

year-end 2009, when the average savings account rate nationally

was about 0.25% APY, UECU paid its members 2.00% or eight

times as much! Through the year, federally-insured money market

account yields averaged just under 1% compared to more than 3%

at your Credit Union.

When other institutions tightened their lending standards or simply

weren’t lending, no changes were necessary at UECU. We

continued lending to our members and loans outstanding increased

by 15% during 2009. We emphasized mortgages while many

shied away from the real estate market and our total real estate

secured loans grew by 22%. So if you need a mortgage or home

equity loan, please call your Credit Union.

How do we achieve this level of success year after year? First,

UECU is a cooperative institution, owned by its members.

Because we have no stockholders, every decision is driven by our

desire to act in the best interests of the membership. Second, our

experienced team understands what’s necessary to achieve success

for the membership and the organization. In the financial

marketplace, one cannot totally avoid risk, but must proactively

assess and manage it. Knowing what not to do is just as important

as knowing what to do – a concept that has eluded many large

banks. We take your savings dollars and conscientiously lend

them to other members or effectively invest them and everyone

benefits.

One key aspect of UECU’s success is our focus on keeping

operating costs low. We’ve developed and honed a “branchless”

model that provides greater convenience than visiting a branch and

saves members considerable time and frustration. Combined with

other efficiencies, this approach allows our operating expenses to

be well below half those of similar sized credit unions. The money

we save is returned to you in the form of higher deposit rates,

lower loan rates, and fewer or lower fees.

Placing our members’ financial security first and always seeking to

exceed their expectations means that we continually pursue

improvements in UECU’s palette of financial products and

services. In recent years, this has meant expansion of our

electronic options, including our home banking platform. Previ-

ously available only through our Call Center, e-Vantages™

by Web

allows members to transfer funds via the Automated Clearinghouse

(ACH) between their UECU accounts and accounts at any other

financial institution. E-Posit Express™

lets members deposit checks

online and receive immediate access to their funds (up to pre-set

limits). With DocuSign®

, members can electronically sign loan

documents and have their loan proceeds available in minutes.

UECU’s Connections™

Checking Account is designed for members

age 15 to 25 and encourages the use of electronic services. It is an

interest-bearing account with no minimum balance requirement,

presently earning 1.75% APY. Connections™

includes free home

banking, Advantages Bill Pay™

, e-statements, an Advantages

VISA®

Check Card™

, unlimited ATM usage, and ATM surcharge

rebates. Qualified members also receive a Connections VISA

Power Card™

.

Our member rewards programs are definitely not the norm. The

VantagePoints™

Network not only rewards members for using a

UECU credit or debit card, but also provides valuable points for

maintaining deposit and credit line balances, for becoming or

referring a new member, and for using various electronic services.

VantagePoints™

can be redeemed online or by phone for gift

certificates, loan rate reductions, or everyone’s favorite, cash.

Additionally, our MyChoice™

program encourages members to use

their Credit Union for more than just savings. When a member

utilizes a service from each of four categories, he can select his own

reward annually from a broad menu of options.

Our financial strength has been recognized by national rating firms

Bauer Financial and IDC Financial Publishing, which again gave

UECU their highest ratings in 2009. In fact, UECU has now earned

Bauer’s 5-Star rating for every quarter since its inception – a period

of more than 20 years. We consistently receive a “clean”

unqualified CPA opinion on our financial statements and our state

and federal regulators rate UECU as a safe and sound institution.

On top of our financial stability, members’ accounts are insured by

the National Credit Union Share Insurance Fund to at least

$250,000 per account.

As we celebrate another highly successful year, I thank the UECU

staff for understanding superior service and assuring that our

members receive it every day. My sincere appreciation also goes

out to our committed volunteer leaders on the Board of Directors

and Committees. And if you’re a member, thank you for choosing

UECU. Your loyalty has allowed the Credit Union to prosper and

evolve into a strong, full service institution that can fulfill all your

financial needs. So, please think of your Credit Union first and tell

your co-workers and family that they too can enjoy the UECU

experience.

2008

2009

2008

2009

2008

2009

Photo from left to right: Walter A. Boquist, II, Vice President - Administration & Legal Counsel,

Patricia A. Zyma, Sr. Vice President/ Chief Financial Officer, Glen A. Yeager, President/CEO,

Kenneth C. Coutumas, Sr. Vice President/Chief Operating Officer

39063 inside.pdf 3/17/2010 10:12:44 AM