1. April 2015 Personal Income Data

Today we receivedApril2015 personal income data. We decidedtotake some time to share withreaderssome of

our takeaways.

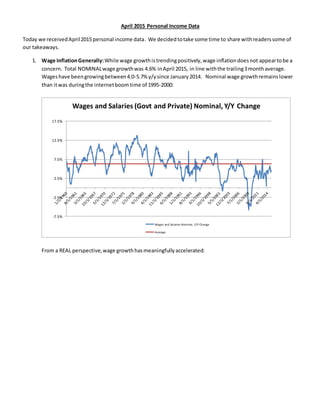

1. Wage InflationGenerally:While wage growthistrendingpositively,wage inflationdoesnot appeartobe a

concern. Total NOMINALwage growthwas 4.6% inApril 2015, in line withthe trailing3monthaverage.

Wageshave beengrowingbetween4.0-5.7% y/ysince January2014. Nominal wage growthremainslower

than itwas duringthe internetboom time of 1995-2000:

From a REAL perspective,wage growthhasmeaningfullyaccelerated:

-7.5%

-2.5%

2.5%

7.5%

12.5%

17.5%

Wages and Salaries (Govt and Private) Nominal, Y/Y Change

Wages and Salaries Nominal, Y/Y Change

Average

5. 4. Personal ConsumptionExpendituresas a Function of EmploymentGrowth: On botha NOMINALandREAL

basis,consumption remainsquite tepidrelativetothe jobgrowthwe are seeingandiswell below whatwe

saw duringthe internetboom. Infact,on a nominal basis,consumptionrelativetoemploymentisatlevels

lastseenin2008:

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Disposable PersonalIncome, Nominal, Y/Y

Disposable Personal Income, Total Average

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

PersonalConsumption Expenditures, Nominal

Deflated by Non-Farm Payrolls

Personal Consumption Expenditures, Nominal Deflated by Non-Farm Payrolls Average

7. Households,on average,are now saving over $6,000, equal to 12% of the average householdincome of

$50,000. As it is unlikelythat the average familyis able to save 12% of their income (the current savings

rate appliedto the average income is roughly$2,800), savings must be skewedto the highestearners:

Withthe average householdtheoreticallysavings$2,800 per year,one can understandwhycreditissovital

to a home purchase. The medianprice of an existinghome soldinthe USinApril 2015 was$265k. A 20%

downpaymentwouldrequire $53kequal to19 years of savingsusingthe currentsavingsrate.

We believe amore accurate portrayal of the savingsrate is encapsulatedbythe chartbelow. While the

overall savingsrate (blue line)is5.7%,if we exclude governmenttransfers(redline),the savingsrate is

roughly -15%. Similarly,if we exclude supplementstowages(greenline),2/3of whichconsistsof actual and

actuarial contributionstopensions,the savingsrate isroughly -7% (we donotknow how muchare actual and

howmuch are actuarial contributionsbutthisdistinctionisclearlyimportantasthe formerisa cash flow

itemwhile the latterisnot). Saidanotherway,if youdon’treceive apensionorgovernmenttransfer,you

likelyhave anegative savingsrate:

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1q65

4q66

3q68

2q70

1q72

4q73

3q75

2q77

1q79

4q80

3q82

2q84

1q86

4q87

3q89

2q91

1q93

4q94

3q96

2q98

1q00

4q01

3q03

2q05

1q07

4q08

3q10

2q12

1q14

Annual Savings/Household, Level Data (1965-

Present)

Annual Savings/Household,Level Data (1965-Present)