Argie bond quant track record

•

0 likes•190 views

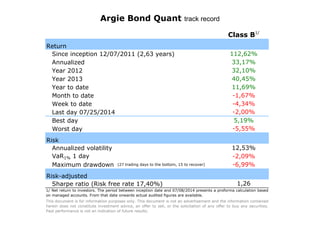

This document summarizes the performance of the Argie Bond Quant fund from inception in December 2011 through July 2014. Over this period, the annualized return was -2.09% and the annualized volatility was 33.17%. The maximum single-day loss was 11.69% and the maximum drawdown over a period of 27 trading days was 32.10%, recovering over the next 15 days. The Sharpe ratio, a measure of risk-adjusted return, was 0.519.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (19)

Similar to Argie bond quant track record

Similar to Argie bond quant track record (19)

Recently uploaded

Recently uploaded (20)

Argie bond quant track record

- 1. Return Since inception 12/07/2011 (2,63 years) Annualized Year 2012 Year 2013 Year to date Month to date Week to date Last day 07/25/2014 Best day Worst day Risk Annualized volatility VaR1% 1 day Maximum drawdown (27 trading days to the bottom, 15 to recover) Risk-adjusted Sharpe ratio (Risk free rate 17,40%) Argie Bond Quant track record -2,09% -6,99% -2,00% -1,67% -4,34% 1,26 40,45% 11,69% Class B1/ 112,62% 33,17% 32,10% 5,19% This document is for information purposes only. This document is not an advertisement and the information contained herein does not constitute investment advice, an offer to sell, or the solicitation of any offer to buy any securities. Past performance is not an indication of future results. 12,53% -5,55% 1/ Net return to investors. The period between inception date and 07/08/2014 presents a proforma calculation based on managed accounts. From that date onwards actual audited figures are available.

- 2. Daily data Inception date 12/07/2011 =0,4500 Argie Bond Quant track record The period between inception date and 07/08/2014 presents a proforma calculation based on managed accounts. From that date onwards actual audited figures are available. 0,40 0,50 0,60 0,70 0,80 0,90 1,00 1,10 D ____ E 2012 F M A M J J A S O N D E 2013 F M A M J J A S O N D E 2014 F M A M J J Maximum drawdown Recovery Argie Bond Quant

- 3. J F M A M J J* A S O N D Year 2011 2,60% 2,60% 2012 3,92% 3,05% 2,58% 0,50% -2,11% 4,23% 4,55% 0,94% 4,05% -1,45% 2,48% 5,75% 32,10% 2013 5,71% -3,57% 6,81% 6,16% -2,54% -0,68% 5,78% 2,26% 7,55% 8,06% -1,13% 1,01% 40,45% 2014 8,43% 1,41% 0,61% 0,90% 2,67% -0,90% -1,67% 11,69% * as of 07/25/2014 Argie Bond Quant track record