Downloaded 166 times

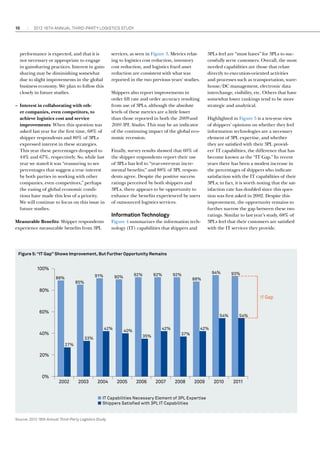

The 2012 Third-Party Logistics Study surveyed shippers and 3PLs to understand the current state of the logistics outsourcing market. Key findings include: 1) Shippers continue to outsource approximately 42% of their logistics expenditures on average, indicating continued confidence in 3PL services. 2) 64% of shippers are increasing their use of 3PLs, while 24% are bringing some services back in-house. 3) Total logistics expenditures average 12% of shippers' sales revenues, with transportation managed by 3PLs averaging 56% and warehousing 39%.