1. Stimuli in China, Europe and the UK

Central banks in China, Europe and Great Britain have announced at the same time (July 5) measures to

stimulate domestic economies fueling speculation of coordinated action.

Concerned by the economic slowdown both China and the ECB lowered interest rates. At the same time GB’s

central Bank increased money supply by £50 billion.

Hence in Europe the interest rate stands at 0.75% the lowest level ever. Meanwhile China surprised financial

markets by lowering interest rates for the second time in less than one month by 0.31% to the 6% level. In

addition the British Central Bank hinted it was preparing an additional £150 billion worth of asset (bonds)

purchasing package. Details of the package were rumored to be revealed during the 9 to 14 July week.

The latest less-than-expected non-farm payrolls report confirms U.S. anemic pace of new jobs creation. The

latter increases the chances that the Fed (the Fed) will announce Q3 at the next FOMC meeting (Aug1st).

Most significant is the ECB decision to lower deposit rates to 0. Consequently European bank deposits with the

ECB no longer earn any returns. Ergo excess bank funds are being “encouraged” into interbank lending.

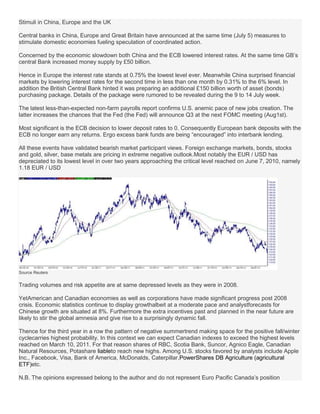

All these events have validated bearish market participant views. Foreign exchange markets, bonds, stocks

and gold, silver, base metals are pricing in extreme negative outlook.Most notably the EUR / USD has

depreciated to its lowest level in over two years approaching the critical level reached on June 7, 2010, namely

1.18 EUR / USD

Source Reuters

Trading volumes and risk appetite are at same depressed levels as they were in 2008.

YetAmerican and Canadian economies as well as corporations have made significant progress post 2008

crisis. Economic statistics continue to display growthalbeit at a moderate pace and analystforecasts for

Chinese growth are situated at 8%. Furthermore the extra incentives past and planned in the near future are

likely to stir the global amnesia and give rise to a surprisingly dynamic fall.

Thence for the third year in a row the pattern of negative summertrend making space for the positive fall/winter

cyclecarries highest probability. In this context we can expect Canadian indexes to exceed the highest levels

reached on March 10, 2011. For that reason shares of RBC, Scotia Bank, Suncor, Agnico Eagle, Canadian

Natural Resources, Potashare liableto reach new highs. Among U.S. stocks favored by analysts include Apple

Inc., Facebook, Visa, Bank of America, McDonalds, Caterpillar,PowerShares DB Agriculture (agricultural

ETF)etc.

N.B. The opinions expressed belong to the author and do not represent Euro Pacific Canada’s position