The Economic and Organised Crime Office (EOCO) has been advised by the Office...

BIR FORM.docx

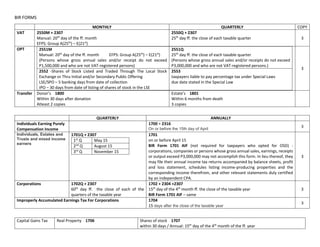

1. BIR FORMS

MONTHLY QUARTERLY COPY

VAT 2550M + 2307

Manual: 20th

day of the ff. month

EFPS: Group A(25th

) – E(21st

)

2550Q + 2307

25th

day ff. the close of each taxable quarter 3

OPT 2551M

Manual: 20th

day of the ff. month EFPS: Group A(25th

) – E(21st

)

(Persons whose gross annual sales and/or receipt do not exceed

P1,500,000 and who are not VAT-registered persons)

2551Q

25th

day ff. the close of each taxable quarter

(Persons whose gross annual sales and/or receipts do not exceed

P3,000,000 and who are not VAT-registered persons.)

2552 -Shares of Stock Listed and Traded Through The Local Stock

Exchange or Thru Initial and/or Secondary Public Offering

LSE/SPO – 5 banking days from date of collection

IPO – 30 days from date of listing of shares of stock in the LSE

2553

taxpayers liable to pay percentage tax under Special Laws

due date stated in the Special Law

3

Transfer Donor’s 1800

Within 30 days after donation

Atleast 2 copies

Estate’s 1801

Within 6 months from death

3 copies

QUARTERLY ANNUALLY

Individuals Earning Purely

Compensation Income

1700 + 2316

On or before the 15th day of April

3

Individuals, Estates and

Trusts and mixed income

earners

1701Q + 2307

1st

Q May 15

2nd

Q August 15

3rd

Q November 15

1701

on or before April 15

BIR Form 1701 AIF (not required for taxpayers who opted for OSD) -

corporations, companies or persons whose gross annual sales, earnings, receipts

or output exceed P3,000,000 may not accomplish this form. In lieu thereof, they

may file their annual income tax returns accompanied by balance sheets, profit

and loss statement, schedules listing income-producing properties and the

corresponding income therefrom, and other relevant statements duly certified

by an independent CPA.

3

Corporations 1702Q + 2307

60th

day ff. the close of each of the

quarters of the taxable year

1702 + 2304 +2307

15th

day of the 4th

month ff. the close of the taxable year

BIR Form 1701 AIF – same

3

Improperly Accumulated Earnings Tax For Corporations 1704

15 days after the close of the taxable year

3

Capital Gains Tax Real Property 1706 Shares of stock 1707

within 30 days / Annual: 15th

day of the 4th

month of the ff. year

2. Certificates issued by the withholding agent

2304 Certificate of Income Payment Not Subject to

Withholding Tax (Excluding Compensation Income)

on or before January 31 of the year following the year in which the income payment was

made

2305 Certificate of Update of Exemption and of Employer's

and Employee's Information

within ten (10) days after such change or event. (This form is given to the main employer,

copy furnished the secondary employer)

2306 Certificate of Final Income Tax Withheld on or before January 31 of the year following the year in which income payment was made.

However upon request of the payee the payor must furnish such statement to the payee

simultaneously with the income payment

2307 Certificate of Creditable Tax Withheld at Source

EWT Attached to 1701/Q @ 1702/Q 20th day of the month following the close of the taxable quarter.

% tax on Gov’t money

payment

2551M/Q on or before the 10th day of the month following the month in which withholding

was made

VAT withholding 2550M/Q on or before the 10th day of the month following the month

2316 Certificate of Compensation Payment / Tax Withheld

For Compensation Payment With or Without Tax

Withheld

on or before January 31 of the succeeding year in which the compensation was paid, or in

cases where there is termination of employment, it is issued on the same day the last

payment of wages is made

2322 Certificate of Donation within thirty (30) days from receipt of donation

Submitted by Withholding Agents (SUBSTITUTED VAT RETURN/WITHHOLDING AGENT VAT RETURN)

1600 Value-Added Tax and Other Percentage Taxes Withheld 10th

day of the ff. month

1600WP Percentage Tax on Winnings and Prizes Withheld by

Race Track Operators

20th

day from the date the tax was deducted and withheld.

1601-C Monthly Remittance Return of Income Taxes Withheld

on Compensation

EFPS

January-November: 10th

day of the following month

December: On or before January 15 of the following year

EFPS: Jan-Nov: GroupA-E 15th

-11th

day of the following month

December: Group A-E 15th

-11th

day of the following month

1601-EQ Creditable Income Taxes Withheld (Expanded) last day of the month following the close of the quarter during which withholding was made

1601-FQ Final Income Taxes Withheld last day of the month following the close of the quarter during which withholding was made

1602-Q Final Withheld On Interest Paid on Deposits and

Deposit Substitutes/Trusts/Etc.

1603-Q Final Income Taxes Withheld (On Fringe Benefits Paid to Employees Other

than Rank and File)

1604-E Creditable Income Taxes Withheld (Expanded)/ Income

Payments Exempt from Withholding Taxes

On or before March 1 of the year following the calendar year in which the income payments

subject to expanded withholding taxes or exempt from withholding tax were paid or

accrued.

1606 Withholding Tax Remittance Return (For Transactions

Involving Real Property other than Capital Asset

including Taxable and Exempt)

10th

day following the end of the month in which the transaction occurred.