1. Charles R. Blyth Fund

20 Jan 2010

Technology | Gaming

Activision Blizzard: Buy Erin Parker | ecparker@stanford.edu

Ryan Rosztoczy | ryanr2@stanford.edu

Joanna Xu | joannaxu@stanford.edu

Lionel Vital | lgvital@stanford.edu

Megan Kanne | mkanne@stanford.edu

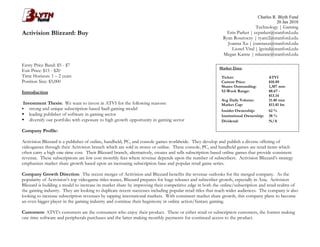

Entry Price Band: $5 - $7

Market Data:

Exit Price: $15 - $20

Time Horizon: 1 – 2 years Ticker: ATVI

Position Size: $5,000 Current Price: $10.89

Shares Outstanding: 1,307 mm

Introduction 52-Week Range: $8.67 -

$13.14

Avg Daily Volume: 11.40 mm

Investment Thesis: We want to invest in ATVI for the following reasons: Market Cap: $13.81 bn

strong and unique subscription-based SaaS gaming model Insider Ownership: 62 %

leading publisher of software in gaming sector Institutional Ownership: 38 %

diversify our portfolio with exposure to high growth opportunity in gaming sector Dividend: N/A

Company Profile:

Activision Blizzard is a publisher of online, handheld, PC, and console games worldwide. They develop and publish a diverse offering of

videogames through their Activision branch which are sold in stores or online. These console, PC, and handheld games are retail items which

often carry a high one-time cost. Their Blizzard branch, alternatively, creates and sells subscription-based online games that provide consistent

revenue. These subscriptions are low cost monthly fees where revenue depends upon the number of subscribers. Activision Blizzard’s strategy

emphasizes market share growth based upon an increasing subscription base and popular retail game series.

Company Growth Direction: The recent merger of Activision and Blizzard benefits the revenue outlooks for the merged company. As the

popularity of Activision’s top videogame titles wanes, Blizzard prepares for huge releases and subscriber growth, especially in Asia. Activision

Blizzard is building a model to increase its market share by improving their competitive edge in both the online/subscription and retail realms of

the gaming industry. They are looking to duplicate recent successes including popular retail titles that reach wider audiences. The company is also

looking to increase subscription revenues by tapping international markets. With consistent market share growth, this company plans to become

an even bigger player in the gaming industry and continue their hegemony in online action/fantasy gaming.

Customers: ATVI’s customers are the consumers who enjoy their product. These or either retail or subscription customers, the former making

one time software and peripherals purchases and the latter making monthly payments for continued access to the product.

2. Charles R. Blyth Fund

20 Jan 2010

Competition: Other companies that publish video games either in retail or online. Examples of such companies include: Electronic Arts Inc.,

Sony Corporation, and Take-Two Interactive Software Inc.

Risks: Volatility created by game console wars. Revenue depends upon relatively small number of franchises as largest source of revenue.

Successful integration of Activision and Blizzard dependent upon management because Vivendi holds over 50% of commonshares implying that

ATVI is a controlled company. Thus, marketing, cost management, preserving development/distribution relationships, and overall coordination

of marketing/publishing/distribution are all key factors in how well ATVI performs. Industry and company will respond to drops in

discretionary income/rises in unemployment in 2010 based upon the discretionary nature of the product and the high number of casual gamers

that bolstered their most popular series. Recent insider trading may cast a negative light upon the company’s prospects.

Available Products: Activision: Call of Duty, Guitar Hero/Band Hero/DJ Hero, Tony Hawk, games based upon licensed properties from

LucasArts, Marvel, and DreamWorks Animation. Blizzard: World of Warcraft, Starcraft, Diablo.

Recent News

Call of Duty Modern Warfare 2 Surpasses $1bn in Retail Sales Worldwide: MW2 continues to set sell-through records since its launch in

November, in the first five days alone the game sold $550 mm worldwide, there are only a handful of entertainment properties that breach

the $1bn mark

Video Game Industry Prospects Poor: Console cycle is aging and demand for high-end systems has been satiated. Consumers continue

cutbacks in discretionary spending resulting in 13% drop in overall industry sales during November 2009.

Strong holiday season for Call of Duty: Modern Warfare 2: Sold six million units in December and made $310M on first day alone,

breaking videogame records.

Subscriptions Strong; Console Games Weak: Many of Activision’s aging console game series are seeing a drop in revenue and popularity

which is being balanced by increased subscriptions. Trend expected to continue in 2010 with three large upcoming Blizzard releases.

New ZBoard Keyset Based on StarCraft II: SteelSeries peripheral manufacturer created a customized keyboard in preparation for the

upcoming release of Starcraft II.

Guitar Hero Kicks Off 2010 With Great Downloadable Tracks: To jumpstart revenue from the Guitar Hero series, Activision released

downloadable singles on its website.

S&P Ups Rating To Strong Buy: Standard & Poor’s equity analyst Jim Yin raised ATVI to Strong Buy from Hold while noting its recent

fall with the industry. He quoted strong Call of Duty sales, subscription revenue, and expansion in China as optimistic signs for stock.

Financials and Valuation

3. Charles R. Blyth Fund

20 Jan 2010

Balance Sheet Trends

Cash has been steadily increasing from $354mm in 2006 to $2.9bn in 2008

There has been a similar trend in accounts receivable

More than half of the company’s assets are in Goodwill and Intangibles

While accounts payable and expenses have been rising accordingly the company has no long term debt

Revenue vs. Cost Growth

2006 2007 2008

Revenue 1468 1337.88 3026

% Growth -8.86% 126.18%

Cost of Revenue 940.36 382.02 1839

% Growth -59.38% 381.39%

SG&A 379.76 330.3 735

% Growth -13.02% 122.52%

R&D 132.65 384.81 592

% Growth 190.09% 53.84%

Income Statement Trends

Company made net loss of $107mm in 2008 because SG&A and R&D expenses surpassed revenue

As a result, retained earnings were negative

Cost of revenue grew faster than revenue in 2008

Cash Flow Statement Trends

Deferred tax liability account (as a result of differences in tax and GAAP accounting standards) means ATVI will have to pay more in taxes in

the future

Cash from operating activities is positive and has been steadily increasing from $86mm in 2006 to $379mm in 2008

Company has been making steady capital expenditures

Company has received most funding from stock issuances