10 facts about taxation in Slovakia | Infographic

•

0 likes•55 views

Discover the top 10 facts about taxation in Slovakia, one of the many overviews to come about Slovak business environment.

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Similar to 10 facts about taxation in Slovakia | Infographic

Similar to 10 facts about taxation in Slovakia | Infographic (20)

Recently uploaded

Recently uploaded (20)

10 facts about taxation in Slovakia | Infographic

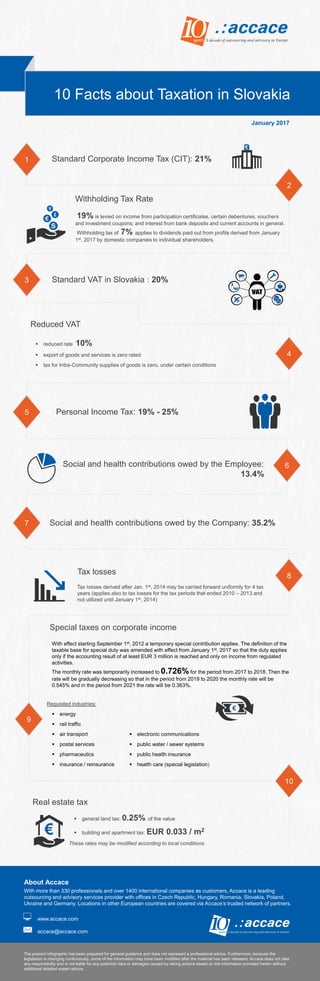

- 1. Standard Corporate Income Tax (CIT): 21% 19% is levied on income from participation certificates, certain debentures, vouchers and investment coupons; and interest from bank deposits and current accounts in general. Withholding tax of 7% applies to dividends paid out from profits derived from January 1st, 2017 by domestic companies to individual shareholders. Withholding Tax Rate Standard VAT in Slovakia : 20% 10 Facts about Taxation in Slovakia 1 2 8 9 10 Personal Income Tax: 19% - 25% Social and health contributions owed by the Employee: 13.4% Social and health contributions owed by the Company: 35.2% Tax losses Regulated industries: energy rail traffic air transport postal services pharmaceutics insurance / reinsurance Special taxes on corporate income About Accace With more than 330 professionals and over 1400 international companies as customers, Accace is a leading outsourcing and advisory services provider with offices in Czech Republic, Hungary, Romania, Slovakia, Poland, Ukraine and Germany. Locations in other European countries are covered via Accace’s trusted network of partners. www.accace.com accace@accace.com The present infographic has been prepared for general guidance and does not represent a professional advice. Furthermore, because the legislation is changing continuously, some of the information may have been modified after the material has been released. Accace does not take any responsibility and is not liable for any potential risks or damages caused by taking actions based on the information provided herein without additional detailed expert advice. 6 7 Reduced VAT reduced rate 10% export of goods and services is zero rated tax for Intra-Community supplies of goods is zero, under certain conditions 4 5 Tax losses derived after Jan. 1st, 2014 may be carried forward uniformly for 4 tax years (applies also to tax losses for the tax periods that ended 2010 – 2013 and not utilized until January 1st, 2014) Real estate tax general land tax: 0.25% of the value building and apartment tax: EUR 0.033 / m2 These rates may be modified according to local conditions. electronic communications public water / sewer systems public health insurance health care (special legislation) With effect starting September 1st, 2012 a temporary special contribution applies. The definition of the taxable base for special duty was amended with effect from January 1st, 2017 so that the duty applies only if the accounting result of at least EUR 3 million is reached and only on income from regulated activities. The monthly rate was temporarily increased to 0.726% for the period from 2017 to 2018. Then the rate will be gradually decreasing so that in the period from 2019 to 2020 the monthly rate will be 0.545% and in the period from 2021 the rate will be 0.363%. 3 January 2017